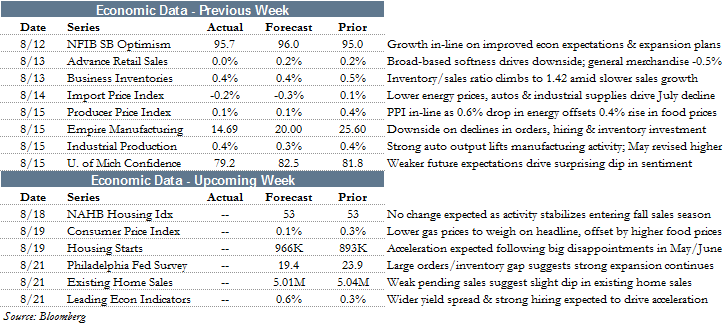

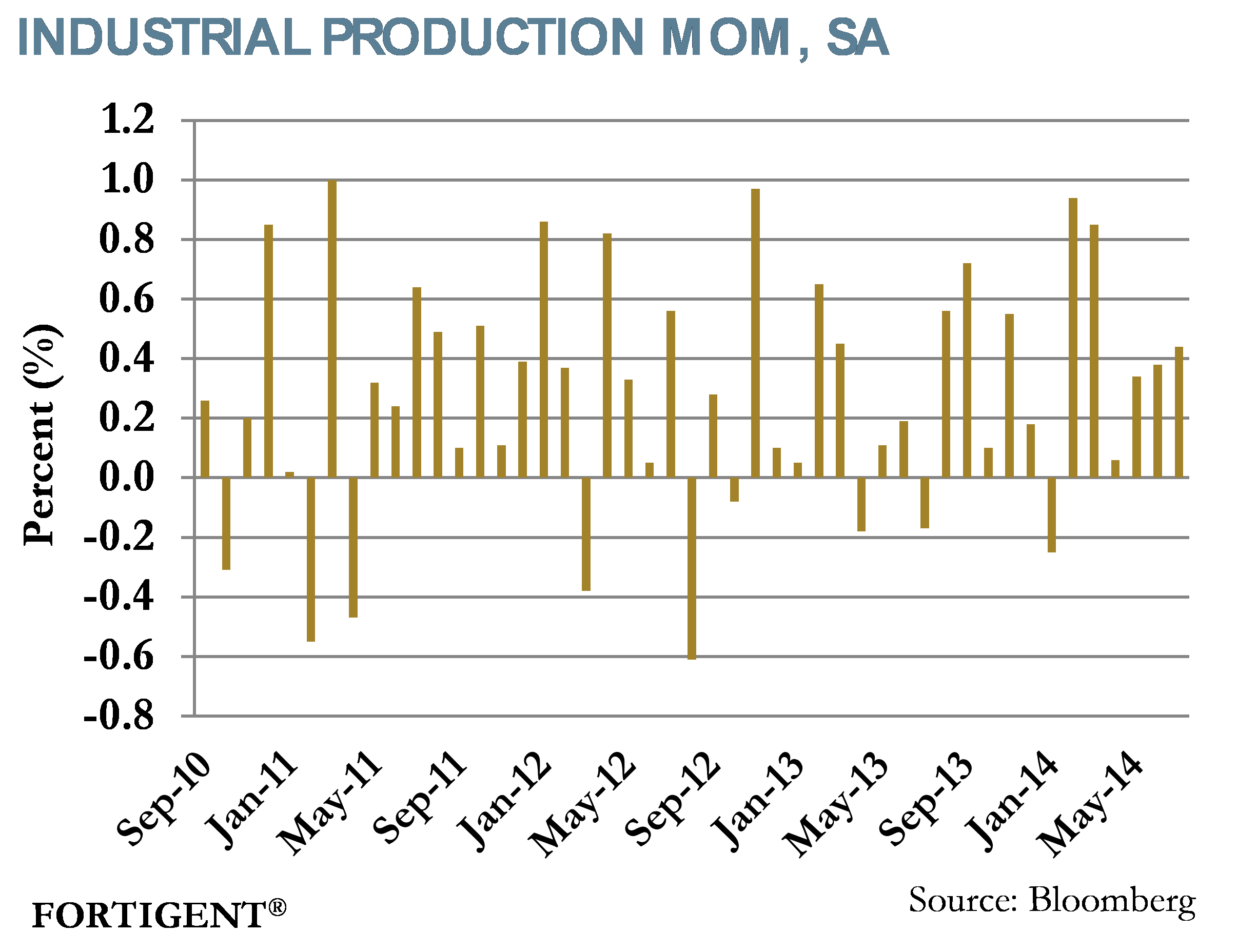

Industrial Production Remains Strong

Equity markets moved higher for most of the week before geopolitical caused a reversal on Friday. For the week, the Dow Jones Industrial Average gained 0.7% and the S&P 500 gained 1.2%.

It was a relatively quiet summer week, but a few important economic indicators were released. Manufacturing offered an encouraging picture, but consumer data was lighter than anticipated.

In the manufacturing space, industrial production rose 0.4% in July, matching similarly strong performance in June. Strength was attributable to a 1.0% bump in manufacturing, along with a 1.3% rise in business equipment production. Utilities detracted for the second consecutive month.

Retail sales continued to decelerate in July, finishing the month unchanged. That follows gains of 0.2% in June and 0.4% in May. Sales were mostly flat across the board, but disappointing auto sales weighed on the headline figure. Excluding auto sales, July retail sales were up a still sluggish 0.1%.

Consumer sentiment also disappointed for the month, falling 2.6 points in the early portion of August. Consumers are taking divergent views on the current state of the economy relative to future expectations. The survey found that current feelings about the economy continued to improve, but consumers became sharply less optimistic about the 6-month outlook for the economy.

Source: Econoday

The final indicator last week was the Producer Price Index, which posted a 0.1% increase. Inflationary pressure was evident in certain areas such as food, but energy prices fell 0.6% after a more than 2% gain in June. Food prices rose as a result of a 9.2% jump in beef and veal prices. Overall, inflation crept up in important areas like food, but the retracement of energy prices should aid consumer spending in the months ahead.

Europe Taking a Negative Turn

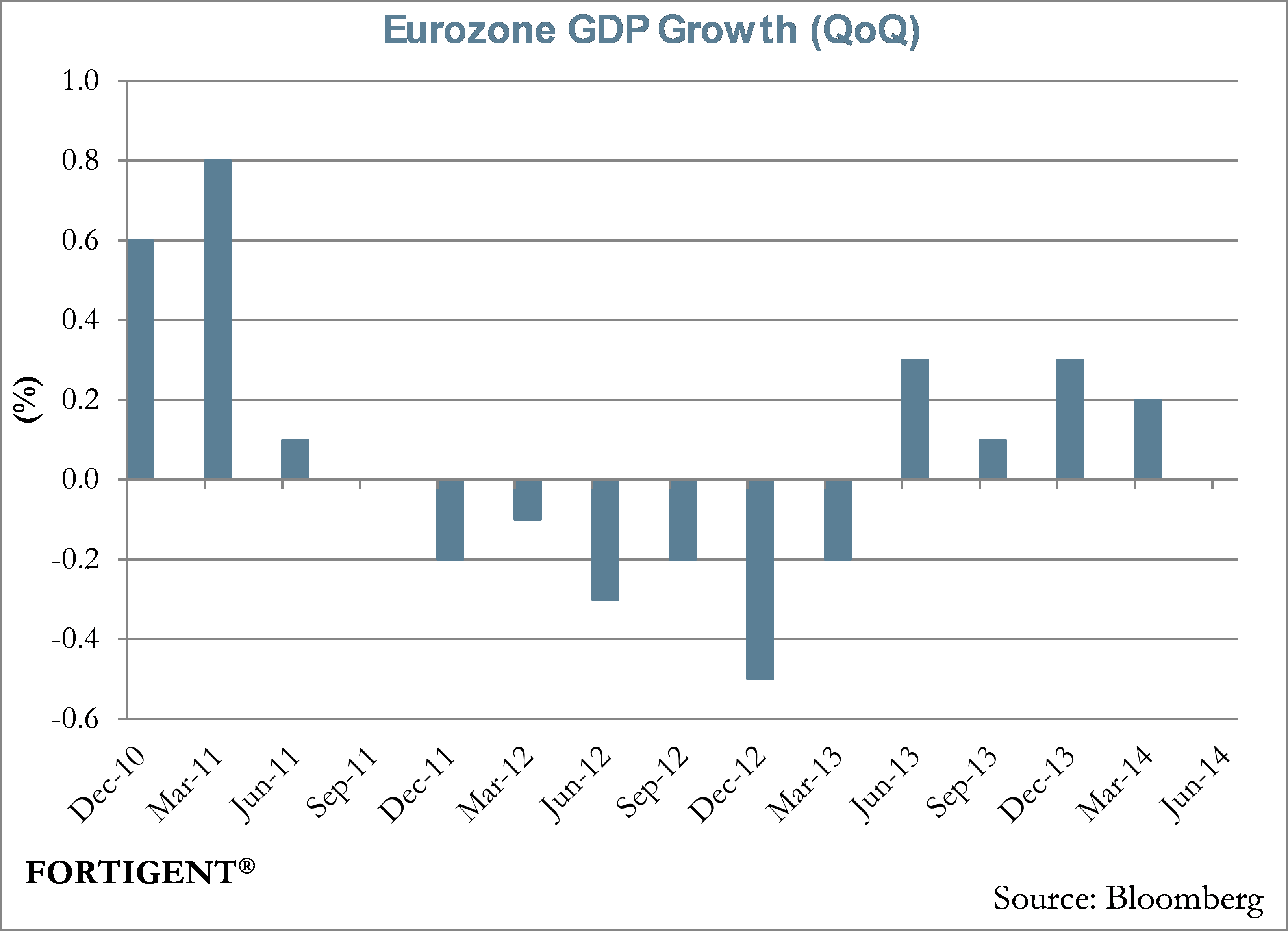

Among the highlights of a busy calendar of economic data last week was the flash estimate of second quarter Eurozone GDP. The region has come under greater scrutiny in recent months amid a disinflationary trend and slowing economic data. As we discussed a few weeks ago, the high profile failure of Portuguese bank Banco Espirito Santo has also inflamed worries that Europe’s financial system remains vulnerable to a systemic shock.

Last Thursday’s flash estimate of the monetary bloc’s second quarter GDP did nothing to relieve those concerns. The European Union posted a quarter-over-quarter figure of 0.0%, below an already meager consensus estimate of 0.2%. Even worse was the distribution of growth: the economy’s powerhouse, Germany, contracted 0.2%, while France was flat and Italy declined 0.2% in the quarter. If not for a rebound across several peripheral countries (Spain, Portugal) from very poor first quarters, the broad region would have sank into negative territory.

A litany of other data does little to lift optimism about second quarter GDP. The day before, manufacturing data showed unexpected weakness. June industrial production levels for the Eurozone fell 0.3%, far below a consensus 0.4% gain. Some rebound was anticipated following May’s 1.1% contraction.

Inflation data for July was more discouraging, with consumer prices sinking 0.5% over the month. Year-over-year, the measure of prices in the European Union matched its lowest level since 2009 at 0.6%. The lack of inflation in Europe has been a major left-tail risk factor bubbling to the headlines of late, and those concerns are only getting louder.

Amid a tepid lending environment in Europe and sluggish economic growth, inflation readings appear to be careening toward deflation. This has caused many to speculate that the ECB will need to step in and take bolder action, including potential quantitative easing. For its part, the ECB seems content to rely on its promise to do “whatever it takes,” in combination with its recent TLTRO program – a lending package designed to stimulate borrowing by banks and to prop up credit growth. The group has been under pressure to provide more tangible assistance to the region, but has been reluctant to do so thus far.

Unfortunately, things may get worse before they get better. Recent analysis by Fathom Consulting for Thomson Reuters suggests that the sanctions by the EU on Russia could meaningfully cut into growth. They note the significance of Russia as a trading partner with Europe, accounting for 4% of Euro exports and 8% of imports. According to Fathom’s estimates, economic growth could be reduced by as much as 1-1.5% in the first year of sanctions.

Source: Thomson Reuters

With the ECB paralyzed and lawmakers ill equipped to govern a patchwork of independent sovereigns, Europe may prove to be a more hazardous contributor to global financial markets than many realize. While the initial onset of the European sovereign crisis in 2010 and 2011 sent financial markets reeling, systemic risk in the region has been seemingly benign since Mario Draghi’s famous speech in July 2012. Yields on European peripherals rallied sharply over the past two years as that negative risk sentiment abated.

If the European economy continues on its current trajectory, however, market participants may be forced to grapple with the reality that little has structurally changed since that pre-crisis period. Debt levels remain high, regulatory changes are in flux, and underlying demand continues to be sluggish, especially across the peripherals. At some point, even if European officials are to step in, it may be too late to reverse the negative inertia currently taking hold.

The Week Ahead

The week kicks off with the NAHB Housing Index. Housing starts and existing home sales data follow later in the week. The Consumer Price Index, Philadelphia Fed Survey, and Leading Economic Indicators are also slated to be released.

Central bank meetings are light this week with just the Bank of Namibia and Central Bank of Iceland scheduled to meet.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value