Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

Â

One of our favorite measures to monitor in relation to the gold market has been the relationship between the gold price expressed in US dollars and the US 10 year real yield with the real yield being the nominal yield on a government bond adjusted for inflation expectations. Over the long term studies have shown that gold has a much stronger relationship with real interest rates versus nominal interest rates. The period most commonly used as evidence of this is during the 1970s which were a period of rising nominal interest rates but high inflation and hence low real rates that were accompanied a rising gold price. The implication being that rising nominal rates need not necessarily lead to falling gold prices with the level and trend of real rates being of greater importance in influencing gold prices. More specifically, there is historical evidence to show that gold has tended to perform best in an environment of falling and low real interest rates and perform poorly in an environment of rising and high real interest rates. Arguably ‘falling and low real interest rates’ accurately describes the current environment here in the US and other major economies such as the European Union, the UK and Japan and as such in the charts below we examine the recent relationship between real yields in each of these countries and the price of gold expressed in the local currency to see if there are any discernible patterns.

Â

Fortunately in economies with developed financial markets we are usually able to observe real yields directly as there are actively traded inflation-linked government bond markets. In this discussion we use the yield on the 10 year inflation-linked bond as the measure of real yields. Intuitively we can rationalize why there might be a relationship between the gold price and interest rates. A factor typically ascribed to driving the relationship is simply that with gold essentially having zero yield, the opportunity cost of holding gold versus a yield generating asset is (by definition) lower in a low real interest rate environment. Lower interest rates therefore make owning gold less expensive and more attractive for an investor. A second more important factor in our view however relates to our view of gold as a currency. As previous readers of our blog will know, rather than an absolute measure of value, we view gold as a choice of currency, out of the many different currencies available, that an investor can choose to hold. When an investor buys gold priced in dollars they are in effect using gold as a dollar alternative; they are expressing the view that they expect the value of gold to increase relative to the value of the dollar. Hence it is consistent that when the dollar falls in value on currency markets, the price of gold expressed in dollars tends to rise. Similarly when the value of the dollar rises, the price of gold in dollars tends to fall. This can then be tied back to gold’s relationship with interest rates with falling rates tending to be associated with weakness in the dollar and weakness in the dollar tending to be associated with a rising gold price.

Â

We should stress however that we do not wish to imply simplistically that real interest rates are the only factor determining the relative value of gold to other currencies (the price of gold) although we believe that they are a key factor. We recognize that just as there is typically a relationship between two currencies (the FX rate) and the interest rate differential between those two countries, the strength of that relationship fluctuates over time. And the same is likely to be no different for gold - the strength of the relationship between real rates and the gold price is likely to vary, moving between strength and weakness, over different periods of time with other factors such as geopolitics intermittently having greater influence.

Â

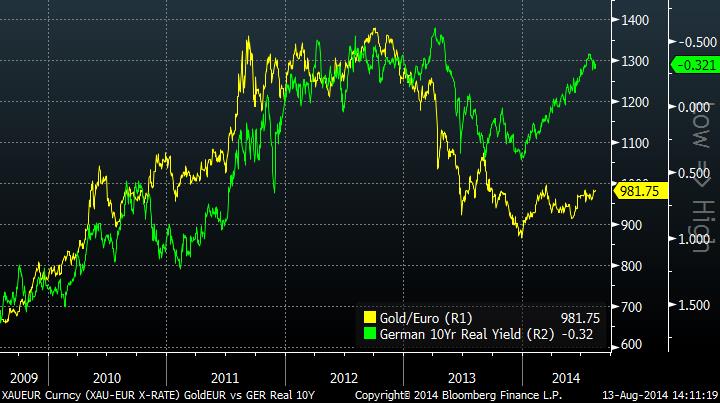

Below we show charts of the price of gold in dollars, euro, yen and pounds overlaid on real interest rates in the US, Germany, Japan and UK respectively. We should note firstly that the vertical, real yield axis has been inverted with values reading from high to low moving upwards on the axis. This is to make the direction of the two data series consistent on the chart with lower real yields being associated with high gold prices. The Gold/Dollar, Gold/Euro and Gold/Pound charts all show similar patterns of a close relationship between the price of gold in local currency terms and the local real interest rate but with varying degrees of divergence since the start of the year.

Â

Â

Â

Â

The greatest divergence has perhaps occurred with German real yields and Gold/Euro with the real yield falling from +0.40% to -0.32% since December 2013. Assuming there has been no structural breakdown in the relationship, in each case we would expect that either the real yield will bottom-out and start to rise or the price of gold in local currency will rise to close the gap. However, absent an economic trigger to push real yields higher, in particular in the Eurozone which is currently battling strong disinflationary forces, we would expect that the more likely outcome would be for gold prices to be supported at current levels or perhaps move higher over the next few months.

Â

Finally we note that in the Gold/yen chart real yield data is only shown from 2013 as prior to that date issuance had been suspended by the Japanese Ministry of Finance since 2008. We have nevertheless included the limited data as it does give some perspective on the significant fall in Japanese real yields (currently -0.70%) over the last year.

© AdvisorShares