The TCW Advantage: Constructing Proprietary RMBS Collateral Benchmarks

This TCW Advantage installment highlights ways in which our analysis is integrated across RMBS metrics through benchmark analysis. We review how TCW develops and maintains custom collateral benchmarks that help our portfolio management team spot risk and value that may be overlooked by others in the marketplace.

Regardless of asset class, investors seek to measure investment performance against benchmarks. For example, an IBM stock investor will want to know how the stock performs against the S&P 500. And a GM corporate bond investor will want to know how the bond performs against the Barclays U.S. Aggregate Index. An index provides context and information about outperformance and underperformance. With tens of thousands of distinct mortgage pools in the non-agency universe whose risk profiles change monthly, analyzing a single pool’s performance and fundamental risk characteristics begs for context. At TCW we create and maintain custom benchmarks that shed insight on a mortgage pool’s fundamental performance and risk profile. These benchmarks help us answer questions like: How does the delinquency percentage of this pool compare to other pools? Is the average mark-to-market LTV of this pool high or low versus other pools available? How do the average updated FICO scores of the loans collateralizing our bond holdings compare to the rest of the market? Benchmarks are essential to answering questions like these. Without them, investors are blind to the most basic tail risks inherent in mortgage pools and have difficulty identifying relative value opportunities.

We begin our benchmark creation by dividing up non-agency mortgage pools by sector: Prime, Alt-A, Option-Arm, and Subprime. Then we take the weighted average loan age (WALA) of each pool to identify the average month, quarter, and year in which the pool loans were originated. We then divide ALL the loans originated in the sector during the relevant quarter into fixed rate mortgage (FRM) and adjustable rate mortgage (ARM) subsets. These subsets form the foundation for our custom benchmarks or “cohorts.”

For example, if Subprime pool “A” currently has 727 ARM loans with a WALA of 98 months and a 60+ day delinquency rate of 26% then we would query our loan level database to find all Subprime ARM loans originated in Q2 2006. The result of this query yields 81,023 loans currently outstanding with a 60+ day delinquency rate of 39%. This group of 81,023 loans is our custom benchmark for this Subprime pool “A”. It provides context. It helps us understand that Subprime pool “A” originated in Q2 2006 is outperforming other similar loans in terms of serious delinquency by 13 percentage points. But it begs the question, “How significant is this outperformance?” We answer this question by cutting up the 81,023 loans into its component pools to create a distribution of serious delinquency deviations from the 39% benchmark performance. Using this distribution of deviations we find the standard deviation is 9%. Hence we can say that pool “A” is significantly outperforming similar loans (Subprime ARMs) originated during Q2 2006 when it comes to serious delinquencies.

It is common knowledge that ARM loans behave differently than FRM loans. And often non-agency mortgage pools contain a mix of ARM and FRM loans. When this occurs we weight the absolute performance and deviations by the percentage of ARM and FRM loans in the pool for any given month during the pool’s history. For example, pool “B” has 1,000 Subprime loans (33.9% FRMs and 66.1% ARMs) originated during Q2 2006. The seriously delinquent loans make up 45% of the overall balance this month. The percentage of all Subprime FRMs originated during Q2 2006 in 60+ delinquencies is 30% with a standard deviation of 7%. As seen above, the percentage of all Subprime ARMs originated during Q2 2006 is 39% with a 9% standard deviation. Hence the custom benchmark for pool “B” is:

% Bal in FRM loans * % FRM Cohort Delinquent

+

% Bal in ARM loans * % ARM Cohort Delinquent

OR

33.9% of Pool B * 30% DQ

+

66.1% of Pool B * 39% = 36%

If we weight the standard deviations the same way we find the benchmark standard deviation is:

% Bal in FRM loans * Standard DQ Deviation FRM

+

% Bal in ARM loans * Standard DQ Deviation ARM

OR

33.9% of Pool B * 7% Stdev

+

66.1% of Pool B * 9% Stdev = 8.3%

Hence, pool “B” with a 60+ delinquency of 45% is significantly underperforming the benchmark of 36% by more than one standard deviation of 8.3%.

The processing to create these metrics for all non-agency bonds and their cohorts occurs nightly so that our portfolio management team has daily refreshed data at their fingertips without delay. One of the many analytics screens available to our team contains the following metrics:

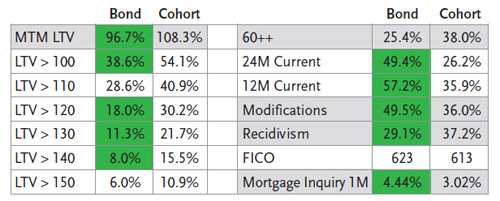

2007 Vintage Example Bond

Sources: Corelogic, Equifax, TCW

2005 Vintage Example Bond

Sources: Corelogic, Equifax, TCW

The green highlights indicate that the pool is outperforming the benchmark pool in that particular metric by more than one standard deviation. Conversely, a red highlight would indicate that a pool is underperforming in that metric. With this approach our team quickly gains a sense for which areas, if any, a mortgage pool deviates significantly from the average. For example, the 2007 vintage Subprime bond has a strong LTV, delinquency, servicing, and updated credit profile relative to its benchmark. And the 2005 vintage Subprime bond is underperforming its delinquency and updated credit benchmarks. While the servicer is modifying more loans than average, the recidivism rate belies the effectiveness of those modifications. Insights like these are difficult to come by unless there is a benchmarking framework embedded in the analytical process.

These benchmarks and their month-over-month changes are also used as the backbone for our portfolio surveillance process. Each month, as we receive new loan data for each non-agency mortgage pool, we compare the change in 60+ delinquencies on the non-agency bonds we hold to the change in the 60+ delinquencies of the relevant benchmark. If a bond’s delta is greater than the average delta plus a benchmark distribution derived deviation then that bond will be added to a “watch list.” The watch list is reviewed by our portfolio management team monthly to provide the highest level of service to our clients. In addition to the 60+ delinquency metric, we observe the changes in several other key risk metrics relative to their benchmarks to add bonds to the watch list. Observing the changes in these risk metrics helps us stay ahead of our competitors by identifying positive and negative trends as soon as the information becomes available.

At TCW we easily highlight underperformance and outperformance of non-agency mortgage pools across all of our risk metrics. This ability when coupled with the proprietary metrics we’ve covered in the “TCW Advantage” series allows TCW portfolio managers to spot risk and value quickly among the tens of thousands of non-agency mortgage bonds that trade in the market. Moreover, as we manage our holdings over time these custom benchmarks perform a pivotal role in the consistency with which our portfolios are managed via surveillance.

This material is for general information purposes only and does not constitute an offer to sell, or a solicitation of an offer to buy, any security. TCW, its officers, directors, employees or clients may have positions in securities or investments mentioned in this publication, which positions may change at any time, without notice. While the information and statistical data contained herein are based on sources believed to be reliable, we do not represent that it is accurate and should not be relied on as such or be the basis for an investment decision. The information contained herein may include preliminary information and/or "forward-looking statements." Due to numerous factors, actual events may differ substantially from those presented. TCW assumes no duty to update any forward-looking statements or opinions in this document. Any opinions expressed herein are current only as of the time made and are subject to change without notice. Past performance is no guarantee of future results.

© 2014 TCW