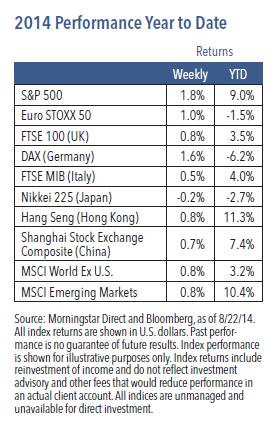

U.S. equities experienced a second week of strong gains, with the S&P 500 Index rising 1.8% and finishing the week near an all-time high.1 Cyclical sectors broadly outperformed, with the industrials, financials, technology and consumer discretionary sectors all posting gains of more than 2%.1 Investor attitudes have changed from where they were earlier in the month when we saw a broad sell-off of stocks driven by renewed concerns around Federal Reserve policy and rising geopolitical tensions. At this point, equities are now nearly 4.5% higher than their early-August lows.1

The Fed Appears to Acknowledge Stronger Growth

Last week’s Fed conference at Jackson Hole garnered some attention, as Fed Chair Janet Yellen focused on improving economic data. Overall, the tone of her speech was fairly balanced and we don’t believe any policy changes are immediately forthcoming. However, she did note the faster-than-expected improvement in the labor market and pointed out that the overall pace of economic growth is getting closer to the central bank’s objectives.

At the same conference, European Central Bank (ECB) President Mario Draghi suggested that the ECB would continue to adopt additional easing stances. He discussed the need for more growth-friendly fiscal and structural reforms for Europe and pointed out the growing divergence between U.S. and eurozone policies.

Weekly Top Themes

1. The labor market is strengthening. Unemployment claims fell last week,2 continuing a months-long trend of better jobs data. Employment indicators are perhaps the most important data sets for capital markets, so investors are rightfully viewing this trend as friendly for equity markets.

2. The housing market is also improving. July housing starts were reported at a much-better-than-expected 1.1 million units.3 Housing is a fundamental driver for the economy and ongoing growth in the labor force should continue to promote housing activity.

3. Manufacturing levels are increasing as well. The Manufacturing Purchasing Manager’s Index reached its highest level since April 20104 and the Philly Fed Survey reached its highest point since March 2011.5

4. The Fed is slowly adopting a more hawkish tone. The central bank is starting to focus on the improved pace of economic growth.

5. The odds of a Republican takeover of the Senate are rising. Given the combination of what looks to be a strong slate of Republican candidates and a difficult political environment for Democrats, we peg the odds of the GOP capturing the Senate at 60%. Should that occur, we believe it would have a limited effect on financial markets as a whole, but it could benefit some areas of the energy, health care and defense industries.

Expect a Low-Growth, Grind-Higher World

The global economy is expanding, but a couple of the key drivers from the past have been fading. Last decade, global growth was largely driven by U.S. consumption and Chinese investment, both of which have diminished as U.S. households are saving more and as the Chinese economy has slowed and become less reliant on investment spending. It appears to us that the world economy’s dominant problem is lower levels of demand compared to what we once saw, and this environment does not appear set to change any time soon.

Nevertheless, economic growth is accelerating (especially in the United States), and monetary policy remains accommodative. With this backdrop, we expect equities to continue to grind higher while experiencing occasional pullbacks. In such a lowgrowth, grind-higher world, investors may want to be cautious about taking on more risk to achieve higher returns. Instead, given that we believe correlations between different investments are falling, we suggest it makes sense to invest more, and to be more selective and more active.

1 Source: Morningstar Direct, as of 8/22/14. 2 Source: Department of Labor. 3 Source: U.S. Census Bureau. 4 Source: Institute for Supply Management 5 Source: Federal Reserve Bank of

Philadelphia.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2014 Nuveen Investments, Inc. All rights reserved.

GPE-BDCOMM4-0814P 2906-INV-W08/15