Housing Market Data Rebounds

Equity markets trended higher for most of the week with the Dow Jones Industrial Average gaining 2.0% and the S&P 500 gaining 1.7%. Tech and small cap stocks slightly lagged broader equity indices as the NASDAQ and the Russell 2000 each gained approximately 1.6%.

The week kicked off with positive news coming out of the housing market. The NAHB Housing Index jumped from 53 in July to 55 in August, exceeding consensus expectations. All components were up, led by future sales and present sales which were both up 2 points.

Housing starts also beat expectations as starts for July rose to an annualized pace of 1.093 million units. This was a 15.7% increase from June, led by the multifamily component, which was up 28.9%. Single-family unit starts were also strong, rebounding 8.3% after declining 4.4% in June. The report showed that momentum is building, driven largely by the multifamily component.

Existing home sales continued to paint a positive picture for the housing market as sales in July advanced 2.4% to an annualized pace of 5.15 million units. This topped consensus expectations of 5.00 million units. Single-family home sales gained 2.7% while condominium sales were unchanged.

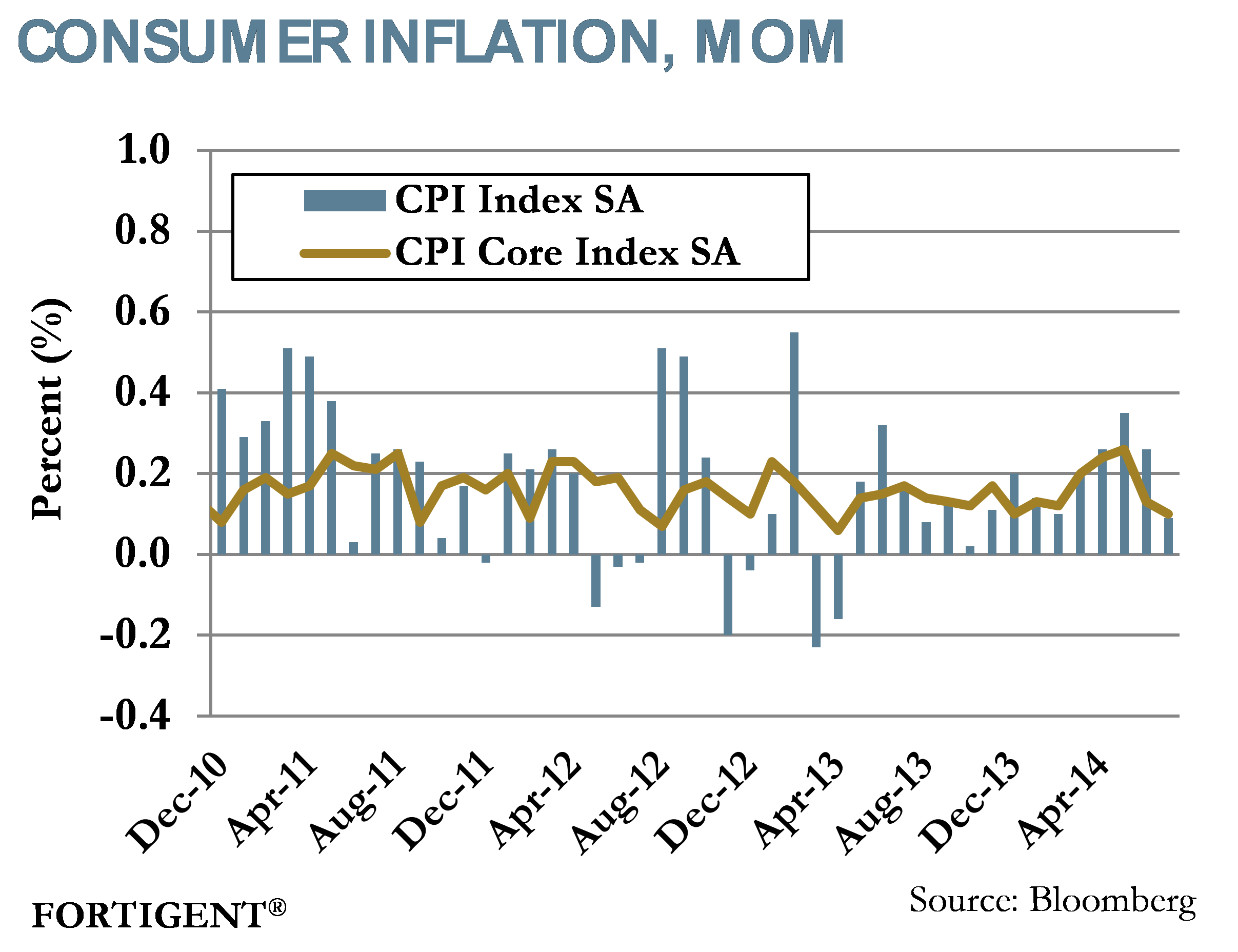

Consumer price inflation for July was meager, rising 0.1% after a solid 0.3% increase in June.

Monthly inflation growth was in line with expectations as energy’s 0.3% decline was offset by a 0.4% jump in food prices. Core CPI, which excludes food and energy, gained 0.1%. This came in slightly below consensus forecasts for a 0.2% gain.

On a year-over-year basis, headline CPI was up 2.0% in July, which is in line with the Federal Reserve’s inflation target. Core CPI is just under the Fed’s target at 1.9% on a seasonally adjusted basis.

FOMC minutes were also released during the week, which indicated that the economy is moving closer to Fed goals. Despite the unemployment rate continuing to fall, FOMC participants still see slack in the labor market with wage rates remaining sluggish. Given the improvement in economic indicators, however, the FOMC indicated that increases in policy rates could come sooner than anticipated. The group emphasized this decision is still dependent on data. Markets showed little reaction to the release.

Event Driven Managers Encounter a Short-Term Hiccup

After a period of very strong deal activity during the first half of 2014, traders and investors were hit with “arbageddon” in early August. “Arbageddon” struck after a series of large deals fell apart, sparking concern that the pickup in activity from earlier in the year was coming to an abrupt halt. Activity since that time would suggest otherwise, and it appears that the M&A train is back on course.

Despite the dog days of summer being in full effect, early August brought forth one of the most painful trading days for many hedge funds, mutual funds and institutional investors. During one 24-hour period, Sprint announced that it was dropping its bid to acquire T-Mobile, and 21st Century Fox nixed its $80 billion acquisition for Time Warner. Further complications arose as government officials announced that recently popular tax inversion deals were in their crosshair, leading to Walgreen’s unexpectedly dropping its pursuit of such a deal.

By way of background, tax inversion deals are when a company acquires or mergers with an overseas firm and reincorporates in the acquired firm’s country in order to take advantage of the lower tax rate in that country. Until recently, inversion deals were uncommon, and a massive pickup in activity during the past several years is causing politicians to take a closer look at the legality of such deals.

Source: Vox, Goldman Sachs

Resulting from tax inversions deals being called into question, and the breakup of several large deals was a dreadful multi-day period of performance for many of the largest investors. Some funds were estimated to be down in excess of 2% to 3% despite subdued conditions in the broader market.

At the time, several publications questioned whether this would represent the end of some of the most popular event driven trades for the last few years. Strategies such as merger arbitrage, special situations, and activist were heavily invested in the M&A renaissance, and fully taking advantage of the popularity in tax inversion trades. For the time being, it appears that those concerns were misplaced.

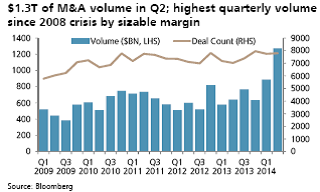

Through July, M&A activity was up 73% year-over-year, according to UBS, with $1.3 trillion of new deals announced during the second quarter alone. Even since the tumultuous period in early August, deal activity is not showing indications of slowing down. Companies such as Roche announced plans to buy InterMune for $8.3 billion, Dollar Tree and Dollar General are competing for an $8.5 billion+ acquisition of Family Dollar, and Coca-Cola purchased a 16.7% stake in Monster Beverage for $2.15 billion. Even tax inversion deals are resurfacing, as Burger King revealed plans to potentially merge with Canadian-based Tim Horton’s.

Source: UBS

There are other reasons to believe this trend will persist. Standard and Poor’s estimates that S&P 500 companies are carrying more than $1.2 trillion in cash on balance sheets, and management teams are anxiously looking for ways to grow revenue in an otherwise muted economic environment. With interest rates remaining low, the combined forces of high cash and cheap financing provide a strong tailwind to acquisition activity. The short-term blip that occurred in early August was likely nothing more than a confluence of bad timing and should not be viewed as the start of a breakdown in M&A activity.

The Week Ahead

The week ahead is full of data releases and kicks off with new home sales data. This is followed later in the week with the release of the Case-Shiller Home Price Index and pending home sales. Also on tap are durable goods orders, personal income, and consumer confidence and sentiment indicators.

The second revision to Q2 GDP is slated for release Thursday. It is expected to be revised down slightly, from 4.0% to 3.9%.

Central bank meetings this week include Israel, Turkey, Egypt, and Columbia. Minutes from the Central Bank of the Republic of Turkey has attracted interest from some observers as the central bank continues to clash with the government’s view on rate policy.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value