Those responsible for collecting and disseminating economic data face the constant trade-off between timeliness of the data and its ultimate accuracy in capturing the economic phenomenon it is trying to measure. Many nations (both developed and emerging) worldwide have robust processes in place to gather and report economic data on a timely basis. Places like Canada, the European Union, and Japan in the developed world, and China, Brazil, and Mexico in the emerging markets have very robust and timely economic data. But generally speaking, the United States has the most reliable, comprehensive, timely, and conflict-free economic data collection and reporting system in the world. Despite our leading position on economic data collection and distribution, the economic data digested on an hourly, daily, weekly, monthly, and quarterly basis is still subject to a great deal of uncertainty and revision. A report due out later this week on the health of the nation’s economy helps to illustrate this point.

When Is it Final?

Later this week, on Thursday, August 28, 2014, the U.S. Department of Commerce Bureau of Economic Analysis (BEA) will release a revised estimate of gross domestic product (GDP) for the second quarter of 2014. The initial estimate of second quarter GDP was released on July 30, 2014, and showed the economy expanded at a 4.0% rate in the second quarter after the 2.1% weather-related decline in the first quarter of 2014. The data released since July 30, 2014 on retail sales, inventories, business capital spending, construction, employment, government spending (federal, state, and local), exports, and imports suggest second quarter GDP will be revised down slightly. In late September 2014, after another round of reports on retail sales, inventories, business spending, etc., the BEA will release another estimate of GDP for the second quarter. But even then, it’s not “final.” In fact, if history is any guide, we’ll still be getting a new read on last quarter’s GDP 12 years from now. How can the best economic data collection in the world produce this kind of uncertainty?

Judgmental Trend

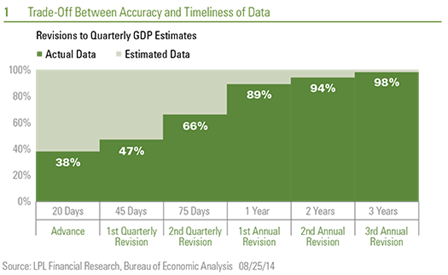

The Figure1 helps to explain the never-ending process of revisions. When the BEA releases the initial estimate (called the “advance estimate” by the BEA) roughly 20 business days after the end of the reference quarter, it has only collected 38% of the data that feeds into GDP categories on hand. Most of the rest of the data used to calculate GDP in that first, or “advance” estimate is filled in by the BEA using assumptions, or “judgmental trend,” or by using data from a similar data series. For example, data on imports and exports are not known for the final month of the reference quarter until a week after GDP is released, so the BEA makes an assumption about what that report will look like and plugs that into GDP. It does the same for inventories and several components of consumer and government spending, among many others.

By the time the second estimate of GDP is released -- about 45 days after the end of the reference quarter -- nearly 50% of the GDP report is based on actual data, with the rest left to judgment and indicator series. By the time the third estimate of GDP for a given quarter is released, roughly two-thirds of the data are known and only a third are unknown. The next time a quarterly GDP figure gets revised is at the next annual revision of GDP, which almost always happens at the end of July. At that point, the BEA has 90% of the actual data in hand it needs to calculate GDP for the quarter and estimates the rest. Every five years or so, the BEA does a “comprehensive revision” to GDP, and at that point, GDP for any specific quarter is just about as final as it will get, as the BEA has 98% of the data it needs to calculate GDP.

How, or more importantly, why do investors, the media, and the public at large obsess over each release of GDP? Mainly because revisions to GDP don’t often change the overall picture of the health, or lack thereof, of the economy. A recent study by the BEA on this topic found that, on average, the successive “vintages of GDP” (the advance estimate, the second estimate, the third estimate, etc.) successfully indicate:

- The direction of change in real GDP 97% of the time;

- The acceleration or deceleration of growth about 72% of the time;

- The relative magnitude of growth -- whether it was above, near, or below trend (near trend is less than one standard deviation from the mean) more than four-fifths of the time; and

- The cyclical peaks before five of the six recessions in 1969 – 2006 and the cyclical troughs of four of the six recessions between 1969 and 2006.

In other words, at two percentage points, the large revision to first quarter 2014 GDP -- initially reported as a 0.1% decline in April 2014, then revised to -1.0% in May, -2.9% in June, and then to -2.1% in July 2014 -- was an anomaly. From 1983 through 2009, the mean absolute difference between the first estimate of GDP for any quarter and the latest (most recent) estimate is one percentage point. The good news here is that prior to 1960, the revisions were closer to three percentage points, so despite cutbacks to congressional funding of data collection at the federal level in recent years, the GDP data are a lot more accurate than they used to be. The bad news is that each time GDP is released, market participants rely more on “judgmental trend” than actual data to help gauge the pace of economic activity.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1- 301764 (Exp. 08/15)