S&P 500 Hits the 2,000 Mark

Equity markets moved modestly higher last week, with the S&P 500 closing above the 2,000 level for the first time. The S&P 500 added 80 bps on the week and now stands up 9.9% on the year following a 4% gain in August. Bonds also rallied last week, rising in tandem with European sovereigns. The rate on the 10-year Treasury fell to 2.33% by week’s end.

ECB President Mario Draghi’s recent acknowledgement of disinflationary trends in Europe has increased expectations for additional ECB policy action. Some believe Draghi’s comments, made at the Jackson Hole Economic Symposium, reveal a fundamental shift in the central bank’s policy approach – now one of greater accommodation following greater emphasis on austerity. The ECB was initially unwilling to engage in quantitative easing like several of its peers, but falling prices and economic growth across the region may force the group’s hand. The ECB meets this week in what will be a closely watched meeting.

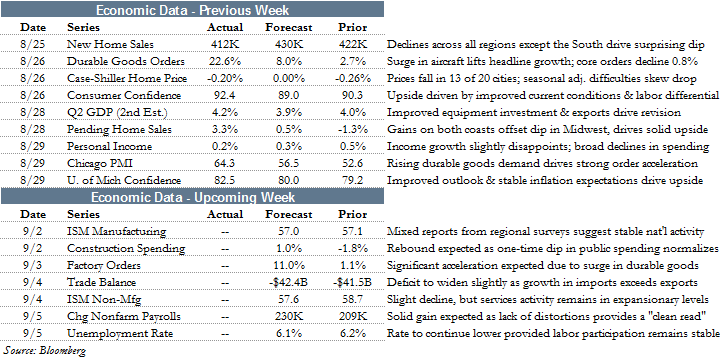

Last week marked a busy one for economic data in both the US and abroad. Domestic releases were generally positive, though not universal, led by an upward revision to second quarter GDP. The Bureau of Economic Analysis reported that annualized growth in the US advanced at a 4.2% rate in Q2, relative to an initial estimate of 4.0%. The revision was largely tied to better nonresidential fixed investment data.

Personal income and consumer spending softened somewhat in July following a robust May and June period. Income growth slowed to 0.2%, month-over-month, while spending contracted 0.1%. Both figures were below consensus expectations. Analysis by Econoday suggests the surprise drop in consumer spending occurred via the durables component, with volatility in vehicle sales serving as the main culprit.

A flurry of housing data also hit the newswires last week, encompassing sales and home prices. New home sales were encouraging, with the measure coming in at 412,000 annualized in July. Although this was below consensus, upward revisions to May and June pushed the previous estimates higher by 28,000. Also notable was an uptick in supply and a modest decline in home prices. Tight inventory and sharp home price increases have been viewed as a headwind for sales in recent months.

The decline in home prices was echoed by separate measures by Case-Shiller and the FHFA. Prices fell 0.2% in June, according to the S&P Case-Shiller 20-City Index – the second straight monthly contraction for a series that has otherwise been in positive territory since 2011. The FHFA Home Price Index, meanwhile, increased 0.4% in June, but year-over-year the measure slipped from 5.3% to 5.1%. The latter index has been on a consistent downtrend since peaking just above 8% in mid-2013.

Outside of the US, important data concerning Japan, Europe, and China made its way to investors.

Japanese data was mixed, with retail sales surprising to the upside while industrial production disappointed. An increase in the VAT tax on consumer purchases earlier this year has adversely affected consumption levels. In July, however, retail sales grew 0.5% year-over-year following three months of contraction.

Europe, meanwhile, saw mostly disappointing data last week. Economic sentiment for the monetary union fell to 100.6, down a point-and-a-half from last month and below expectations. The index’s components were broadly weak, with declines observed in consumer confidence, retail, construction, and consumer inflation expectations.

In what has become a closely watched indicator in the region, Eurozone inflation once again softened. August’s HICP edged down to 0.3% year-over-year, down a tenth from July and the lowest rate since 2009. The data only served to enhance expectations of ECB action, particularly in the wake of Draghi’s aforementioned comments.

Finally, China saw two competing manufacturing PMI indicators released over the weekend, with both suggesting a slight slowdown in August. Some may consider the recent data a mere blip, as it follows a period of accelerating momentum for Chinese manufacturing. Both the official government and private market statistics remain in expansionary territory, at 51.1 and 50.2, respectively.

The Week Ahead

September begins with a full slate of economic data, ranging from the ISM surveys to the government jobs report on Friday. The Federal Reserve’s Beige Book, a compendium of economic conditions across the country, is also due for release on Wednesday.

In Europe, the ECB’s policy announcement Thursday will take center stage. However, important releases concerning retail sales, manufacturing, and the first estimate of second quarter GDP are also on tap.

Economists expect EU growth to flat line quarter-over-quarter and to slip to 0.7% on a year-over-year basis.

Other global central banks with policy announcements this week include the Bank of England, Egypt, Canada, Mexico, Brazil, Australia, Poland, and Sweden.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value