Voya Fixed Income Perspectives August 2014

Bond Market Outlook

Global Interest Rates: We are overweight duration in those parts of the world where rate hikes will be eclipsed by zero interest rates in the U.S. and Europe.

Global Currencies: Foreign central bank accommodation will continue to support the dollar, though the recent rally likely limits nearterm upside. We have lowered our EM currency exposure in light of heightened volatility.

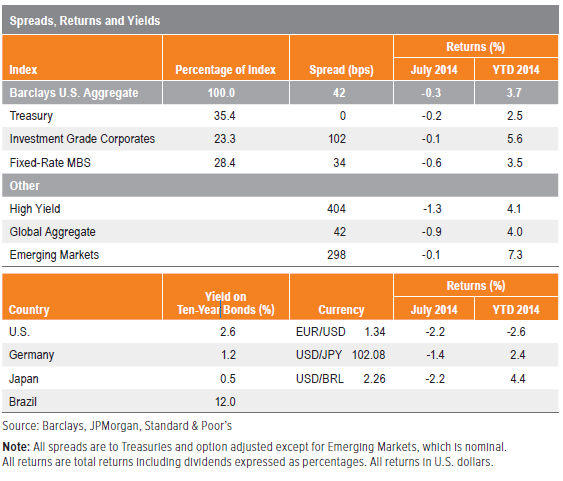

Corporates: Spreads are fairly valued, and we expect carry to be the primary driver of excess returns for the balance of the year.

High Yield: The recent selloff has provided an attractive entry point.

Mortgages: We favor CMBS and non-agency MBS, as we expect credit risk will continue to be well-bid.

Emerging Markets: While positive overall, we are cautious near term, as correlations appear unsustainable and fundamentals have not kept pace with the rally.

Macro Overview

- Like the buzz of the alarm clock on the first day of school, the July/early August market selloff awoke investors to the fact that the lazy, carefree days can’t last forever. Though a single catalyst for the latest shift in sentiment is tough to identify, there are a number of suspects: ample geopolitical uncertainty, the possibility that strong U.S. economic data may hasten fed funds rate normalization and Fed rhetoric about froth in certain markets. And while longer-term market trends have resumed, with credit spreads grinding tighter and the S&P 500 hitting all-time highs, the clear lesson going forward is that the volatility alarm can sound at any time.

- Our view is that despite signs of persistent U.S. growth — including strengthening consumer confidence, improved labor market conditions and budding inflation pressures — the Fed will withdraw its accommodation slowly. Meanwhile, interest rates have moved lower, not higher, as the economy continues to operate below potential; according to the Fed, “underutilization” of the labor supply is a key driver of this output gap and is one of the reasons the central bank remains dovish in the face of stronger economic data. Non-domestic factors also are contributing to the suppression of U.S. yields; with central banks in Europe, Japan and China all easing, money continues to seek a relative return, often in the form of U.S. Treasuries.

- Interest rates worldwide should remain contained thanks to the structural concerns overshadowing the U.S. economic recovery combined with the low global growth impulse and the robust liquidity dynamic outside U.S. borders. This should mitigate duration risk and keep spread sectors linked to the U.S. recovery story — like CMBS and high yield bonds — well-bid in the search for yield. While we have seen some deterioration in lending and credit standards, fundamentals remain solid and the U.S. growth outlook continues to improve.

- That the market has to deal with bouts of volatility is simply reality, and we believe these periodic wakeup calls represent buying opportunities. However, they also underscore the importance of protecting portfolios against tail risk now, before the alarm sounds again.

Sector Overviews

Global Interest Rates

- The flood of liquidity from central banks — particularly in light of Europe’s upcoming targeted longer-term refinancing operations (TLTROs) — continues to dominate fixed income and keep positive carry trades in favor. Should improved macro and jobs data inspire a change in the Fed stance at its September meeting, market volatility may follow. But given the central bank’s emphasis at the recent Jackson Hole summit on labor market “slack” and its impact on inflation, our expectation is that a change in Fed strategy is not imminent.

- We are overall neutral on duration risk in developed markets, with the exception of countries like the U.K. and New Zealand, where the expectation of interest rate hikes will be eclipsed by zero interest rates in Europe. We are tactically overweight in emerging markets like Mexico and South Africa for similar reasons.

Global Currencies

- The overwhelming level of accommodation from foreign central banks is likely to persist for the near term and will continue to support the dollar; note the recent depreciation of the euro on the heels of increased QE rhetoric by the European Central Bank. As such, we are overweight the dollar, though the scope of the recent rally will likely limit near-term upside. Given European tail risks and significant dispersion within emerging markets, we have lowered our overall exposure to EM currencies and continue to play the space on a tactical basis.

Investment Grade Corporates

- Investment grade spreads were relatively unscathed in the recent selloff, with inflows remaining steady. Second quarter earnings have rebounded after a dismal first quarter, with EBITDA and capex growth looking solid. Net leverage appears to have ticked up despite stronger profit growth, though a gradual trend higher in net leverage historically has not been an impediment to spread tightening when economic growth is improving.

- From a seasonal perspective, the third quarter is generally the weakest in terms of excess returns, and this year that weakness could be amplified by European tail risks. However, we still believe that the technical backdrop, with new-issue supply easing, is constructive for spreads and that they will ultimately end the year tighter. Spreads are fairly valued, and we expect carry to be the primary driver of excess returns.

High Yield Bonds

- High yield suffered sharp losses in July and early August. The selloff was consistent across rating categories, driven by large outflows — notably by ETFs — rather than underlying credit concerns. Outflows have since abated, and spread tightening has resumed with strong second quarter issuer results, as both revenue and EBITDA showed a pickup. We have seen modest increase in leveraging transactions, but leverage actually has declined of late due to the improvement in earnings.

- With equities rallying, the technical picture improving, credit fundamentals still solid and U.S. economic growth stronger, the recent selloff has provided an attractive entry point for high yield. Excess returns are still expected to be positive at this stage of the credit cycle, and the relative carry offered by high yield versus other fixed alternatives is attractive given the low risk of defaults.

Mortgages

- Agency RMBS suffered losses in the recent selloff given tight valuations and a pickup in prepayment speeds, though spreads have recently stabilized. The continuation of the Fed’s reinvestment purchase program — recent Fed minutes reaffirmed that reinvestments will likely continue until after the first fed funds rate hike — should provide support for mortgages over the longer term. However, as economic improvement continues and Fed support fades, the potential for interest rate volatility remains, which could pressure spreads in the nearer term. We have trimmed our exposure to agency RMBS as a result.

- Within securitized products, we continue to favor CMBS and non agency MBS, as we expect credit risk to continue to be well-bid. CMBS, for instance, is attractively valued given the potential for spread compression. The sector has not snapped back after the July selloff due to low supply and thin trading volumes, but tone is positive and fundamentals remain intact, with delinquencies on the decline and lending standards continuing to ease. We expect the market to pick up after the holiday.

Emerging Markets

- Despite escalated tensions between Russia and Ukraine and increased volatility, contagion across emerging markets has been limited. The rally in emerging corporates and sovereigns continues to be broad based and supported by favorable global liquidity conditions. While valuations are still attractive in a low-rate environment, fundamentals have not kept pace with the rally, and correlations have begun to look untenable (for example, emerging markets have strengthened even as commodity prices weaken). We still maintain a positive view overall but are expressing a note of caution in the near term.

This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or olicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that

are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance does not guarantee future results.

CID# 10401

©2014 Voya Investments Distributor, LLC • 230 Park Ave, New York, NY 10169