Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

Continuing on the theme of the impact that strength in the US dollar might have on the price of gold in dollars, in this week’s discussion we investigate the close historical relationship between the price of gold expressed in dollars and the value of the dollar.

Intuitively we can explain why we should expect there to be a strong relationship between the price of gold in dollars and the value of the US dollar. When we think about ways in which to define gold and its value, we find strong merit in the view of seeing gold as just one of any number of different currencies, albeit a commodity currency, that an investor might choose to hold. So rather than view gold as a physical asset with a given amount of intrinsic value we instead think of gold as a physical currency whose value can be determined, as with other currencies, relative to other currencies; for example how many dollars will an investor receive for an ounce of gold or similarly how many euro will an investor receive for an ounce of gold? In its essence when an investor buys gold in dollars they are expressing the view that they expect the price of gold to increase in terms of the number of dollars for which it can be exchanged at a future date. Similarly an investor that holds gold in euro terms is expressing the view that they expect the price of gold to increase in terms of the number of euros for which it can be exchanged at a future date.

When thought of in these terms we can see how a transaction to buy gold is exactly analogous to a foreign exchange (FX) transaction. In a FX transaction an investor exchanges one currency for another, at an agreed exchange rate and on an agreed date. In a gold transaction, an investor exchanges a currency (e.g. dollars) for gold at an agreed exchange rate, expressed in dollars per ounce. The exchange rate defines the rate at which the market values the two assets on a relative basis. An investor that buys gold in US dollars is therefore expressing a directional view on both gold and the dollar – in market speak they are long gold, short USD.

And it is this short position on the dollar that is creating a conundrum for investors that wish to hold gold for its diversification properties but are concerned about potential future strength in the dollar as the Federal Reserve draws near to ending its asset purchase program. When the price of gold increases in dollar terms, this indicates that the dollar is weak relative to gold. More generally we can say that when the dollar is weak on currency markets, all things being equal, the price of gold in dollars will tend to rise. Similarly when the dollar is strong on currency markets the price of gold in dollars will tend to be fall.

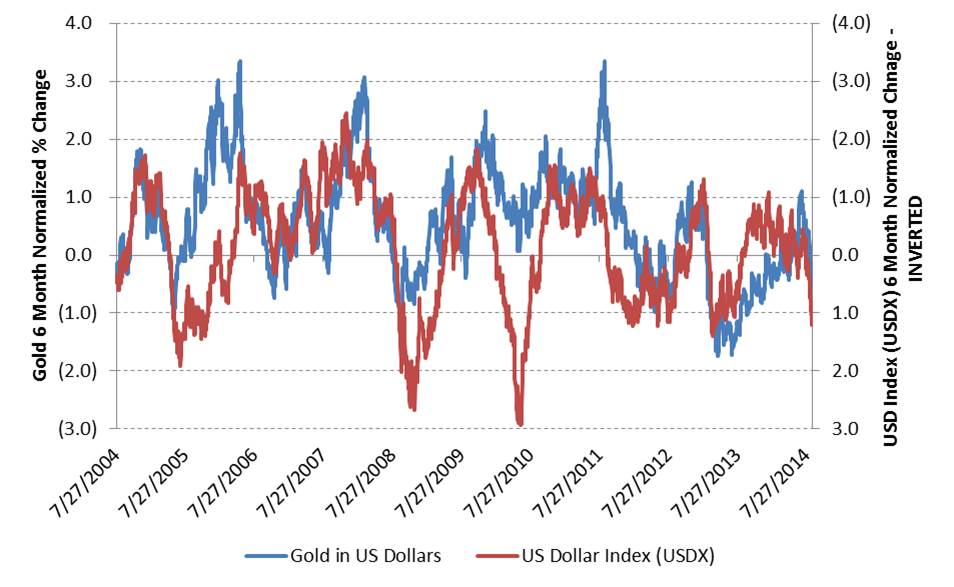

The strength of this relationship is shown clearly in the chart below which plots the 6 month percentage changes in the price of gold in dollars and the Intercontinental Exchange Trade Weighted US Dollar Index (USDX) which is a measure of the value of the dollar on currency markets. The values in the chart are normalized to reflect the fact that gold and FX rates have different standard deviations – here the 6 month percentage change is divided by the semi-annualized, standard deviation of daily returns. Finally the USDX axis has been inverted to make the direction of change of the two series consistent so that a weaker dollar is associated with stronger gold in dollar terms. The strength of the relationship is striking with weakness in the dollar very closely matching strength in the gold price in dollar terms. Of note however there were significant divergences between the two series during the heights of the global, credit crisis in 2008 and the Eurozone “periphery” credit crisis in 2010. These periods saw a sharp rise in the value of the dollar (red line) and weakness in the gold price but the fall in gold was not as sharp as would have been expected based on the prior historical relationship. This was most likely a result of investors’ buying both gold and the dollar as defensive assets as risk aversion spiked.

Source: Bloomberg LP; Treesdale Partners calculations; past performance is not indicative of future performance

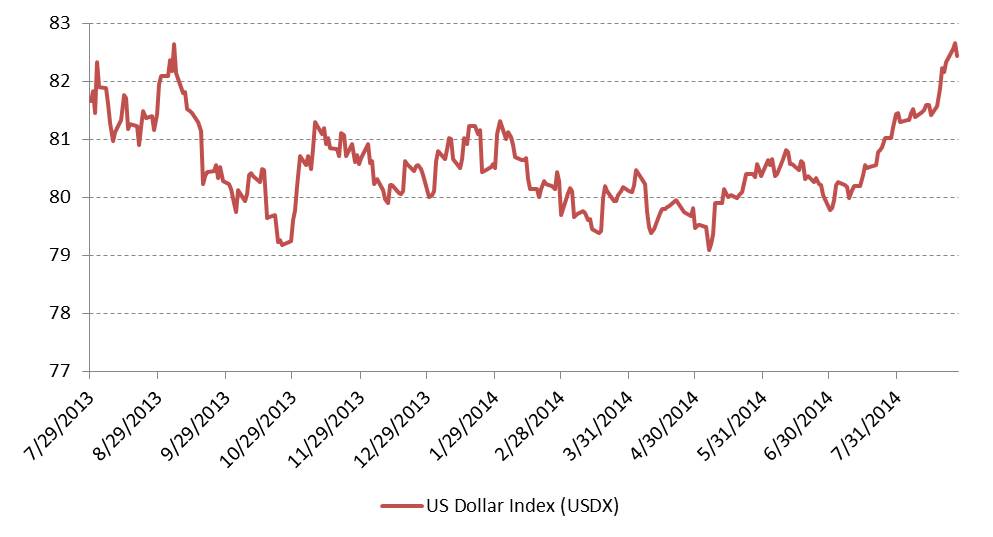

In the final chart below we show the recent performance of the US dollar as represented by the Intercontinental Exchange Trade Weighted Dollar index (USDX) and see that the dollar has strengthened by over 4% from its trough in April. With the Federal Reserve close to ending its quantitative easing program this year and job growth accelerating, the divergence between monetary policy in the US and many of its major trading partners is becoming stark and expectations have risen for the dollar to strengthen. For investors holding gold in dollars, the potential for significant strength in the dollar going forward is a cause for concern given the strong historical inverse relationship between gold priced in dollars and the dollar.

Source: Bloomberg LP; Treesdale Partners calculations; past performance is not indicative of future performance

For investors that wish to maintain an allocation to gold to benefit from its defensive qualities despite the current strong dollar environment we would therefore recommend financing gold purchases in currencies other than the dollar. Our preferred gold financing currencies would be from economies whose monetary policy for macroeconomic reasons, is most divergent from monetary policy here in the US such as in the Eurozone or Japan. And for investors that prefer not to express a strong directional view by using a single financing currency we would recommend taking a diversified currency.