Executive Summary

· A hawk in dove’s clothing, Yellen will likely be ahead of the curve when it comes to hiking rates.

· Driven by strength in manufacturing and a revitalized consumer, corporate America is thriving.

· The euro zone is an economic basket case, forcing Draghi to reach for another “bazooka” solution, to the likely benefit of risk assets.

· Broad, globally diversified portfolios can help protect investors against the volatility that policy normalization may bring.

The Fed Gets Schooled on Improving Economic Growth

With Labor Day behind us, the Federal Reserve may be well advised to open a history book for a refresher. It was only a few years ago that a long period of rock-bottom interest rates spawned the worst housing bubble in memory, which in turn led to conditions in September and October 2008 that then- Fed Chair Ben Bernanke categorized as “the worst financial crisis in global history, including the Great Depression”.

Current Chair Janet Yellen is no doubt well aware of the risks of extended accommodation and has spent 2014 tapering the central bank’s asset purchase program in preparation for an October cessation. But as the domestic economy continues to gain momentum and markets for risky assets rise ever-higher, more decisive action will be needed — and soon. In fact, we expect the Fed to accelerate its timetable for interest rate hikes, to March 2015 or even earlier; the current consensus is that the central bank will leave the fed funds target untouched until mid-2015. That’s right, Janet Yellen is really a hawk in dove’s clothing!

Rising Rates = Good

Rising interest rates typically correspond with economic growth; thus, it’s nonsensical to get a 4.2% GDP growth print for the second quarter while short rates remain pegged near zero. Of course, it’s the Fed that has kept rates low in an effort to foment inflation; while salutary in the short term, these artificial machinations can create longer-term mispricings (i.e., bubbles) as the hunt for yield leads investors toward more speculative, exotic, risky and highly levered securities. Ultimately, though, short- and long-term interest rates will rise, setting off a tug of war. On one side we have rising interest rates, which increase the discount to financial assets; on the other, improving economic fundamentals, driving the markets upward and onward. Expect volatility as this battle plays out.

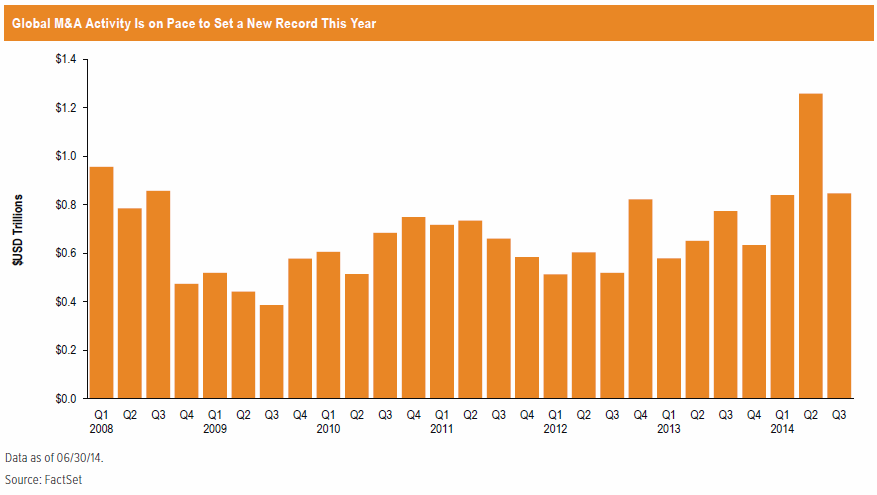

Meanwhile, an enormous amount of economic activity has been on hold in the aftermath of the financial crisis, with participants waiting for signs that it was safe to return to the normal ways of doing business. There’s certainly no shortage of all-clear signals of late. M&A deal activity, for example, is on pace to break the record set in 2007, both in the U.S. and internationally. And given the $1.5 trillion of cash on the balance sheets of S&P 500 companies, the markets could be in for a Hoover Dam-sized flood of spending once companies really open their wallets, not only in deal-making but also in capital expenditures. In fact, these floodwaters already are rising: cash levels dropped at a 19% annualized rate during first quarter 2014.

We also see all-clear signals from the traditional fear gauges of gold and oil, which after a brief surge at the open of 2014 have peaked and are dropping precipitously. Where is the fear? Ukraine, Iraq, Syria: mere blips in the rally. If there is fear out there, it is the fear of missing out on lucrative opportunities by being too meek. Is it all good? No, it never is; let’s look at Europe.

Europe: The Next Japan?

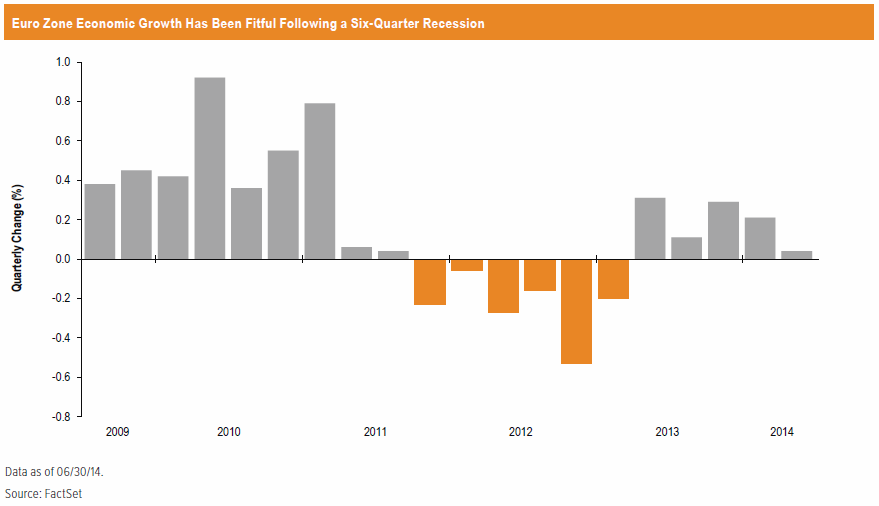

Deflation is a death spiral from which escape is a multiyear struggle — just ask Japan, which only now is showing signs that it may emerge from the deflation and muted economic growth that has plagued it for more than two decades. If recent data are any indication, Europe may be facing a similar fate:

· The euro zone posted an inflation rate of 0.3% in August, a far cry from the European Central Bank’s target around 2%.

· The region delivered second quarter GDP growth of zero, while the last manufacturing PMI showed factory activity at a 13-month low.

· Unemployment remains elevated, at 11.5% in July.

We believe these conditions will compel the ECB to again unleash its “bazooka” of stimulus — just as it did in late 2011 and early 2012 to spark a global market rally. In fact, as we go to press the ECB fired off several rounds of heavy artillery in the form of 10 basis point cuts to its main refinancing rate (to 0.05%), its marginal lending facility (to 0.30%) and its deposit rate (to -0.20%). In addition, ECB Chief Draghi announced the much-anticipated but little-expected launch of a quantitative easing program; the central bank in October will begin purchasing asset-backed securities and covered bonds issues by the region’s banks.

So despite the negative fundamental environment in the euro zone, history suggests that risk investors would benefit from waiting for Europe to act. That looks to be the case in the trading hours following the ECB’s announcement. And while interest rates appeared to have reached their lower boundary, the ECB has room to be more accommodative in the months ahead with its QE program.

Fundamentals in the U.S. Go to the Head of the Class

With rising short rates, deflation risk in Europe, flaring geopolitical risks and U.S. equities at all-time highs, where do we go from here? In terms of market fundamentals, corporate earnings are front and center after the latest blockbuster reporting season.

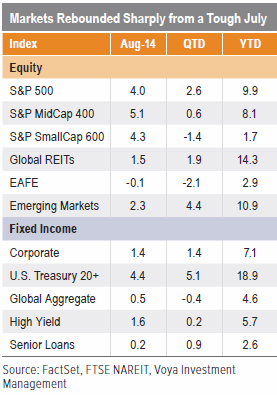

S&P 500 second quarter earnings eclipsed expectations, growing 7.5%.

S&P 500 revenues grew 4.4% in the second quarter, the best performance first quarter 2012.

Small- and mid-cap stocks fared even better than large caps, posting earnings growth of 12.5% and 10.9%, respectively, and revenue growth of 9.3% and 6.3%. In fact, investors may want to consider diverting a greater portion of their U.S. equity allocations to small-cap stocks, which have better growth prospects and are trailing large caps in year-to-date performance by more than 800 basis points.

Manufacturing and consumer strength are the wind in corporate America’s sails. The latest manufacturing PMI hit the highest level since March 2011, while the new orders component — which is suggestive of future activity — surged to its highest mark in ten years. Meanwhile, retail sales figures leaped 3.7% in July from the year prior to an all-time record, driven by strong auto sales. And we see signs that emboldened consumers will be a catalyst for stronger sequential retail growth in the all-important back-to-school shopping season.

· The job market is getting stronger. The four-week moving average of initial unemployment claims has dropped to levels not seen since 2006, and job openings are at 2001 highs.

· Home prices continue to rise. The S&P/ Case-Shiller 20-city composite grew 8.1% year over year through June. Homebuilder confidence rose to the highest level in seven months, while surging permits point to continuing

Applying History Lessons to Your Portfolio

History can be a useful guide, and the similarities between 2008 and today cannot be ignored despite the encouraging fundamental backdrop. We’ve seen market meltdowns during Septembers and Octobers past, the most prominent sparked by the 2008 collapse of Lehman Brothers that had the global financial system on the verge of failure.

If past is prologue, then Fed Chair Yellen should be more fearful of being behind the curve than in front of it; we expect she is and will act accordingly. This means higher rates, a stronger dollar and faster economic growth, resulting in adjustments — both positive and negative — to U.S. financial assets. Investors should ensure that they too are ahead of the curve, by globally diversifying their portfolios to protect against a bevy of risks and to enhance wealth.

This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities. The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. Past performance is no guarantee of future results.

CID# 10434

©2014 Voya Investments Distributor, LLC • 230 Park Ave, New York, NY 10169