A Choppy Path Stretches Ahead, but It Could Favor Equities

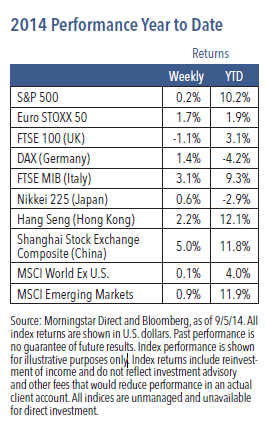

U.S. equities continued their winning ways, with the S&P 500 Index advancing 0.2% last week.1 Although the August employment data were somewhat disappointing, investors were cheered by strong manufacturing trends. Events outside of the U.S. also contributed to the positive tone. The European Central Bank (ECB) announced a surprise rate cut, and a cease fire agreement in Ukraine eased tensions in that region. Defensive sectors generally did better than cyclical sectors, with utilities and consumer staples performing particularly well. On the cyclical side, consumer discretionary stocks outperformed, but the energy sector suffered noticeably as a result of falling oil prices.1

Weekly Top Themes

1. Jobs growth slowed in August. Nonfarm payrolls increased by a much-lessthan-expected 142,000 last month, with the largest slowdowns coming from manufacturing and retail trade.2 On the bright side, unemployment ticked down another notch to 6.1%, and average hourly earnings advanced slightly.2 The silver lining is that the poor showing takes some pressure off of the Federal Reserve to be more aggressive about raising interest rates.

2. Two Institute of Supply Management surveys reached new post-recession highs.3 Both the ISM manufacturing and non-manufacturing surveys trended up last month, a sign the economy is continuing to move in the right direction.3

3. ECB easing is supporting global growth. The ECB’s unexpected announcement that it will cut interest rates by 0.1% and increase its bond-purchase programs should help both European and world growth. In the immediate aftermath of the announcement, European stocks advanced while the euro declined versus the dollar and yen.1

4. Russia/Ukraine turmoil represents a growing risk. Notwithstanding last week’s cease fire, the conflict is hurting European growth, and the threat of additional sanctions could further undermine the region. More broadly, we see a potential risk that the turmoil could begin to affect the rest of the world economy. In particular, we are concerned about the possible negative effect on U.S. multinational earnings and U.S. exports.

5. The United States appears set to become energy independent by the end of this decade. The U.S. is already the world’s largest producer of natural gas and is on pace to become the largest producer of crude oil within the next couple of years.4 At present, the U.S. is still importing oil, but the pace is diminishing, and more is coming from Canada and Mexico than from OPEC countries.4

Expectations for Stocks Look Better Than for Bonds

Equities and government bonds have both performed well this year. This is due in part to accommodative monetary policy and economic growth that has been fast enough to provide support, but not so fast that fears of Fed tightening have taken hold. Government bond markets have also been supported by risk aversion due to rising geopolitical tensions and pockets of disinflation fears around the globe.

But how much longer can this Goldilocks scenario continue for both asset classes? Global economic growth is clearly improving, and we believe that we will soon be at a point where growth will still be a tailwind for equities, but will also put stronger upward pressure on interest rates. We are not expecting the Fed to move rapidly or dramatically, but we do believe the central bank will begin increasing the fed funds rate next year, which should put further pressure on government bonds.

We expect the path ahead for both equities and bonds to be more choppy than what we have seen so far this year, and we also anticipate these asset classes will show more divergence. Specifically, we believe U.S. Treasuries will come under increasing pressure in the face of stronger growth and tighter policy, which may lead to underperformance. The outlook for equities varies a bit more. Should economic growth slow significantly (a scenario we believe is unlikely), stock prices could fall. Should growth continue to improve, we would expect stock prices to rise. Our current view at this point is that equities could experience returns in the high single digits in the coming years.

1 Source: Morningstar Direct, as of 9/5/14. 2 Source: Bureau of Labor Statistics. 3 Source: Institute of Supply Management and Cornerstone Macro. 4 Source: Cornerstone Macro.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment- grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2014 Nuveen Investments, Inc. All rights reserved.

GPE-BDCOMM2-0914P 3056-INV-W09/15