Back to School With the Three Rs: Revenues, Reinvestment, and Renaissance

Summer vacation is over and children are going back to school. As kids return to the classroom to learn the fundamentals of the “three Rs” (reading, ‘riting, and ‘rithmetic -- but clearly not spellin’), in this commentary we return to the basic fundamentals of investing and look at some of the basic drivers of stock prices. To do that, we discuss our own version of the three Rs that underpin our positive stock market outlook for the balance of 2014: revenues, reinvestment, and renaissance.

- Revenues -- as in corporate revenues. Revenues drive corporate profits, and profits are the key fundamental driver of stock prices. Our 2014 earnings outlook remains positive based on several factors discussed below.

- Reinvestment -- as in reinvestment of capital. We believe companies are poised to increasingly reinvest in their businesses and drive future growth.

- Renaissance -- as in manufacturing renaissance. The U.S. manufacturing sector has staged an impressive rebound from the depths of the financial crisis and is experiencing what many have called a renaissance, or rebirth.

We believe these three Rs are all key components in evaluating the opportunity for further stock market gains.

Revenues

If earnings or profits started with R, we would have gone that route here. But as we move to the latter stage of the business cycle, and with margins at record highs, opportunities for companies to further expand their profit margins will likely be limited. Therefore, revenue and profit growth will likely continue to converge as they have done in recent years.

When you make a corporate equity investment, what you’re really buying is a piece of a company’s future earnings. Those earnings are ultimately what justify the price you pay for a stock. Accordingly, we believe the best way to assess fundamentals of the stock market as a whole is to try to predict earnings for the broad market -- certainly no easy task. While we look at many factors when forecasting earnings, our favorite is the Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index (PMI).

What Is the ISM?

The Institute for Supply Management is an association of purchasing and supply management professionals. The ISM surveys its members each month and publishes the results in the form of an index. A reading above 50 indicates expansion in manufacturing activity; a reading below 50 indicates contraction. Purchasing managers are at the front of the line when it comes to activity in manufacturing, because orders for the supplies used to create products at manufacturing companies are a leading indicator of increased manufacturing, just as trimmed orders are indicative of slowing demand. Although manufacturing makes up only about 40% of S&P 500 company earnings, demand for manufactured goods has proven to be a timely barometer of economic activity of all types.

What Is the ISM Telling Us About Revenues (and Therefore Profits)?

The ISM has been an excellent indicator of the future direction of earnings, with a solid track record forecasting earnings growth in coming quarters [Figure 1]. Earnings are the most fundamental driver of the stock market and the most important product of economic growth for investors, which is why the ISM is so useful (and why it is one of the Five Forecasters we highlighted in our Mid-Year Outlook 2014). The recent rise in the ISM Index from 57.1 in July to 59.0 in August (reported on September 2, 2014) suggests improving earnings growth in the second half of 2014 and into 2015. It also tells us that the current business cycle is closer to its middle than its end, and that another R -- recession -- is unlikely in the near term. Expected continued economic growth, combined with corporate America’s strong financial condition, reinforces our positive outlook for corporate revenues and profits. We forecast a 5 - 10% growth rate in S&P 500 earnings in the second half of 2014 and for the full year, which supports our stock market forecast for a 10 - 15% return for the S&P 500 in 2014.*

Reinvestment

The next R is reinvestment -- as in companies reinvesting in their businesses through new capital expenditures. We believe companies are poised to increase their level of capital spending over the balance of this year and beyond. This reinvestment can drive future growth and slow the pace of gains in capital returned to shareholders through share buybacks and, to a lesser extent, dividends.

Capital spending is not depressed; in fact, far from it. After a weather-impacted slowdown in capital spending during the first quarter of 2014 based on gross domestic product (GDP) data (+1.6% annualized), spending on real private nonresidential fixed investment (equipment) rose 8.4% annualized during the second quarter. That pace of spending in the first half of 2014 (5.0%) could be better in the second half, and spending during the current economic expansion has trailed prior economic recoveries since World War II. Among factors contributing to the slower pace of spending: uncertainty around the durability of the economic expansion (and related memories of the financial crisis), lack of monetary and fiscal policy clarity, uncertainty surrounding government policy (health care and fiscal), and crowding out by share buybacks and dividends (see our Weekly Economic Commentary: Capital Spending Check-up, dated May 27, 2014).

A number of factors underpin our expectation that capital expenditures from corporate America are poised to accelerate:

- Companies are flush with cash and balance sheets are healthy -- a record $1.3 trillion in cash is held by nonfinancial S&P 500 companies.

- CEO confidence is on the upswing (less political uncertainty).

- Share buybacks are less compelling at higher stock price levels.

- Manufacturing equipment is aging.

- Credit markets are healthy and interest rates are low.

- Construction is improving and land development is growing.

Capital spending is key to the outlook for the U.S. economy and corporate profits. Figure 2 is an easy way to see why. Capital spending is a big driver of earnings, and earnings drive stock prices. Our expectations for stronger capital spending support our positive view of both the industrials and technology sectors, the destination for the overwhelming majority of these investment dollars.

Renaissance

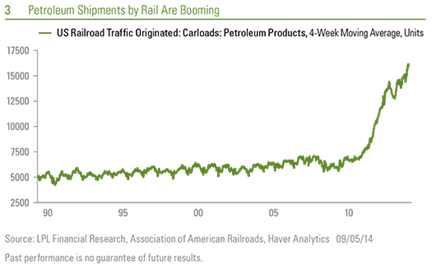

Our third R is renaissance -- as in manufacturing renaissance. The U.S. manufacturing sector has rebounded nicely from the depths of the financial crisis and is experiencing what many have called a renaissance, or rebirth. Another renaissance, the U.S. energy renaissance, is a big part of the manufacturing renaissance. The discovery of shale gas and technological innovation around extracting it has driven the oil and gas industry’s demand for transportation and production-related infrastructure and is starting to drive infrastructure spending to export natural gas. The impact on transportation is evident in Figure 3, which shows booming transportation of petroleum by rail.

Aside from infrastructure demand, the U.S. energy boom has another important benefit for domestic manufacturing -- it provides an abundant source of fuel and raw materials at low prices for manufacturers. U.S. manufacturers get a significant cost advantage over their overseas competitors from cheap gas, which has led several large U.S. companies to build plants here that might have previously been built overseas, including Dow Chemical, GE, and Caterpillar. Foreign companies are also increasingly looking to U.S. shores to build new plants. This ongoing trend of booming U.S. energy production, which we believe is sustainable, along with a number of other economic indicators (including the ISM Manufacturing Index), gives us confidence that the rebound in U.S. manufacturing still has legs.

Look for more from us on capital spending and the manufacturing renaissance in future commentaries.

Conclusion

As our kids go back to school to study their three Rs, we will continue to do our homework on our three Rs, which we believe are keys to the outlook for the stock market: revenues, reinvestment, and the renaissance in manufacturing. Our stock market outlook for the rest of the year remains positive. We expect stocks to garner support from these three Rs in the form of continued growth in revenues and profits, more corporate reinvestment, and continued steady gains for the U.S. manufacturing sector.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

*As noted in our Outlook 2014: The Investor’s Almanac, the stock market may produce a total return in the low double digits (10 - 15%). This gain is derived from earnings per share (EPS) for S&P 500 companies growing 5 - 10% and a rise in the price-to-earnings ratio (PE) of about half a point from just under 16 to 16.5, leaving more room to grow. The PE gain is due to increased confidence in improved growth, allowing the ratio to slowly move toward the higher levels that marked the end of every bull market since World War II (WWII).

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

Because of their narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Tracking # 1-305569 (Exp. 09/15)