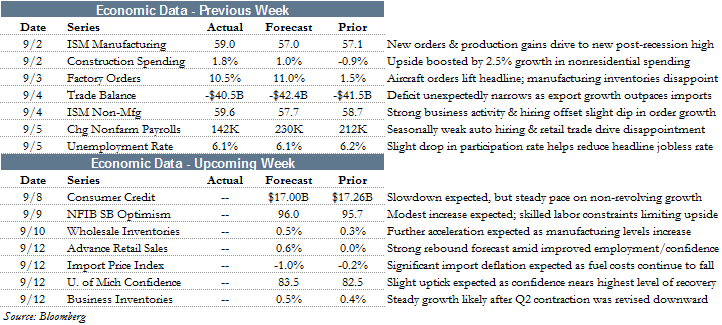

Hiring Flounders in August and Extreme Seasonal Distortions

Stocks Churn near highs as The ECB Comes to the Rescue

Equity markets edged higher last week in a holiday-shortened period. Risk assets see-sawed through the period, sinking Wednesday and Thursday before rallying Friday in spite of a disappointing government jobs report. For the week, the S&P 500 and Dow Jones Industrial Average gained 0.2%.

The most notable development last week was a surprise accommodation by the European Central Bank. Although murmurings of an interest rate cut or an asset purchasing program had made its way into the headlines, most dismissed such action as unlikely. ECB officials sought a bold move to combat disinflation and slowing growth across the monetary union. The group cuts its primary financing rate by 10 bps to 0.05% and indicated they would embark upon an asset purchasing program of up to €500 billion. The latter move is an extraordinary development as it crosses a line the bank adamantly opposed previously.

Outside of Friday’s labor market report, which we discuss further in the topical section, economic data was generally strong last week in the US.

Twin reports released by the Institute for Supply Management (ISM) indicated the US economy is robust. The ISM Manufacturing Index, released on Tuesday, came in above expectations at 59.0 for August. This was the best reading since 2011. The diffusion index’s most important components were quite strong, with new orders and production hitting 66.7 and 64.5, respectively. Employment also remains at strong levels (58.1) despite slipping a tenth over the month.

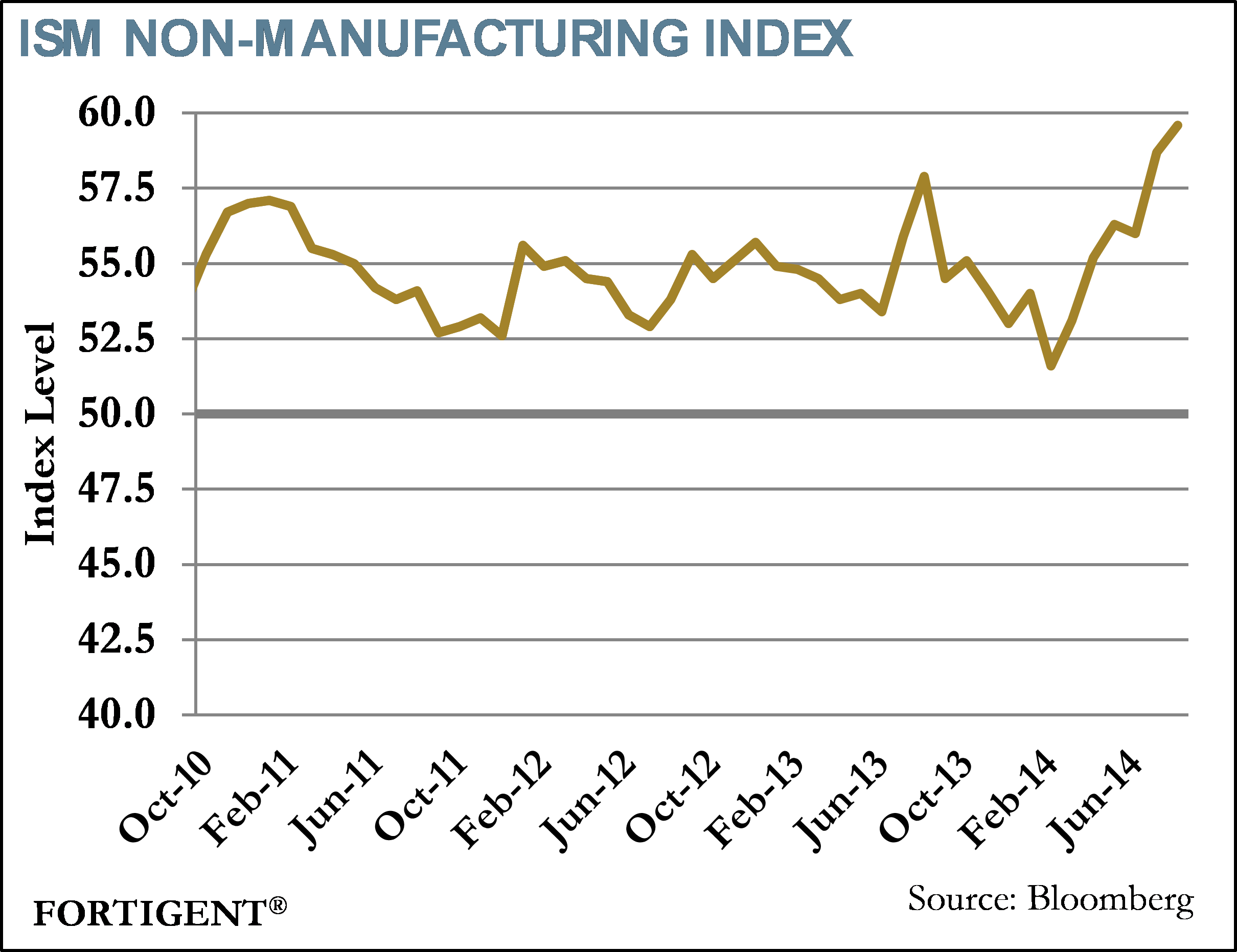

The ISM Non-Manufacturing Index, which measures the strength of the domestic service sector, climbed to 59.6 in August. The uptick from an already-robust July was unexpected, and led by business activity and employment. Despite the improvement, just four components increased in August, with the all-important new orders index slipping 1.1 points. Still, at 63.8, the overall level of new orders remains quite healthy.

The positive picture painted by the ISM reports was echoed by the Fed’s Beige Book, a synopsis of economic conditions across the country. Market participants look closely to this report as it helps guide the Fed’s overall perception of the economy.

The most recent edition of the Beige Book suggested that economic activity improved during the summer months following a slow start to the year. As noted by the Wall Street Journal, this was the third straight Beige Book that reported modest, moderate, or improving growth across all of the Fed districts. There was also evidence that housing markets were stabilizing following a period of weakness.

Hiring Flounders in August amid extreme seasonal distortions

With expectations high, the August labor report landed with a reasonably loud thud. Economists expected recent improvements in labor markets to continue aplenty, but that proved not to be the case during the oftentimes-volatile month of August. It is never wise to read too much into a singular month, and the details of this report support that notion.

Recapping the numbers, headline employment grew by 142,000 in August, far below expectations for growth in excess of 230,000. Also problematic were negative revisions of 28,000 to previously released figures for June and July. The unemployment rate declined from 6.2% to 6.1%.

Despite negative revisions for June and July, there is optimism that August will buck that trend. During the previous four years, August payroll employment was revised higher by an average 55,000. This is reflective of unusual circumstances during the month, such as auto plants moving offline to retool, and other seasonal adjustment issues.

Within the labor report were a couple notable trends. Specifically, top-gaining sectors included professional and business services (+47,000), education & healthcare (+37,000), and construction (+20,000). Weakness was concentrated in retail (-8,000) and information (-3,000). Manufacturing was flat in the month, contrasting strength from various manufacturing surveys released earlier in September.

On a slightly more positive note, earnings growth remains steady. Average hourly earnings rose 0.2% in August, after a 0.1% increase in July. For the past year, earnings are up 2.1%.

Source: Haver Analytics

As noted earlier, the unemployment rate dropped by 0.1%, due in part to fewer people in the workforce, along with a modest rise in household employment. Longer-term, the percent of the population that is employed continues to hover at multi-decade lows. A combination of demographic trends and spillover from the financial crisis are combining to keep that level depressed.

Source: Center on Budget and Policy Priorities

The August labor report was not one that will impress many people, but as we mentioned, August has a historical tendency of being volatile and subject to upward revisions. Given the likelihood of those revisions, the trend of broad based improvement in labor markets is unlikely to be stunted by a single month.

The Week Ahead

Economic data slows down this week, though a few worthwhile reports are due for release. This includes the NFIB Small Business Optimism Survey on Tuesday and retail sales on Friday.

Central bank activity is mostly limited to a handful of emerging markets this week, with Chile, Russia, Peru, South Korea, Indonesia, and New Zealand offering up new policy guidance.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value