-

Despite the many products and services provided by GE, its business strategy is actually startlingly simple. In short, GE is betting on the continued flourishing of the human race.

-

The company is divesting consumer-facing assets and acquiring or boosting commercial-facing ones in what we term the PIT Strategy.

-

An analysis of the company’s valuation drivers suggests an upside potential of the 40% range for GE.

General Electric’s Business Strategy

You may think that GE is a phenomenally complex firm, but you are mistaken. At its core, GE is simply betting on and allocating resources to profit from the continued flourishing of human civilization in all corners of the world.

Thanks to the indelible imprint that Jack Welch[1] left on the firm’s corporate culture, and Jeff Immelt’s realization that consumer facing businesses were volatile and highly competitive, GE has settled on a strategy concentrated on two main areas:

1. Providing the aging, developed world the power and technologies to maintain its standard of living.

2. Providing the young, developing world the power and infrastructure to develop.

These two areas involve overlapping offerings in in power provision, infrastructure build-outs, and highly engineered high-tech solutions. Due to the emphasis on Power, Infrastructure and Technology, we will nickname GE’s present operating focus as the PIT strategy.

GE’s segments, and the classification we will use in this report to describe their foci, is as follows:

|

Segment |

Revenue Share FY13 (%) |

Op Profit Share FY13 (%) |

Classification |

|

Power & Water[2] |

17 |

20 |

Commercial Inputs |

|

Oil and Gas |

11 |

9 |

Commercial Inputs |

|

Energy Management |

5 |

0 |

Commercial High Tech |

|

Aviation |

15 |

18 |

Commercial High Tech |

|

Healthcare |

12 |

12 |

Commercial High Tech |

|

Transportation |

4 |

5 |

Commercial High Tech |

|

Appliances & Lighting |

6 |

2 |

Consumer Products |

|

GE Capital |

29 |

34 |

Consumer Services Commercial Services |

Each of the segments listed as Commercial are those that do not sell to individual consumers, but rather to an organization that provides products and services to end consumers. Any segment listed as “Inputs” are those mainly involved in the business of power provision or in the build-out of critical infrastructure (the “P” and “I” of the PIT strategy). “Services” include financial services and the entertainment services of former subsidiary NBC.

Note in the table above, the degree to which the company is tilted toward the provision of Commercial, rather than Consumer products and services. The only two remaining Consumer-focused business are Appliances & Lighting and Consumer Finance, the remains of both of which are on the auction block now. (Twenty percent of the Consumer Finance division was sold in an IPO earlier this month, and now trades under the name of Synchrony Financial SYF. Foreign Consumer Finance subsidiaries have already been wound down.)

With those two divisions gone, the entire business will be focused on providing products and services to organizations rather than individuals. The only part of the business that doesn’t directly fit into the PIT strategy is GE Capital, but that division fulfills a special role, which we discuss in our full report on GE.

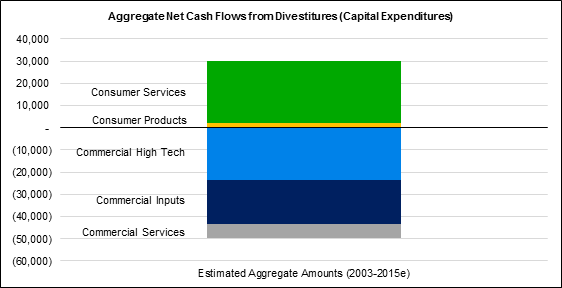

The following graph estimates the value of the 45 major acquisitions the company has made since 2004, split into the above classification structure.[3]

Figure 1. Source: Company Statements, YCharts Research Analysis

In this graph and the one below, a positive number means a net cash inflow from a divestment; a negative number shows a net cash outflow from an acquisition or acquisition-related capital expense.

Note that the aggregate divestments are all classified as “Consumer” and that the aggregate capital expenditures are all classified as “Commercial.”

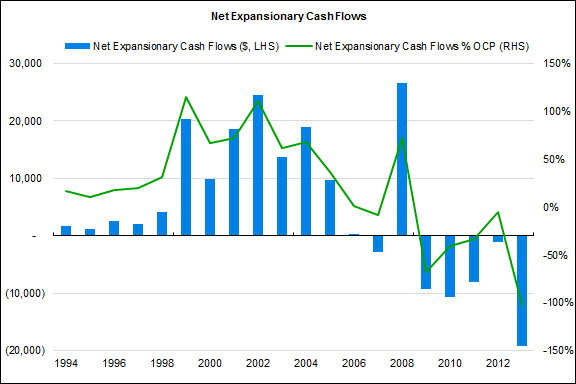

Even though Commercial High Tech shows the largest portion of the graph above, a look at these data disaggregated and spread over time gives a more accurate picture of the present PIT strategy.

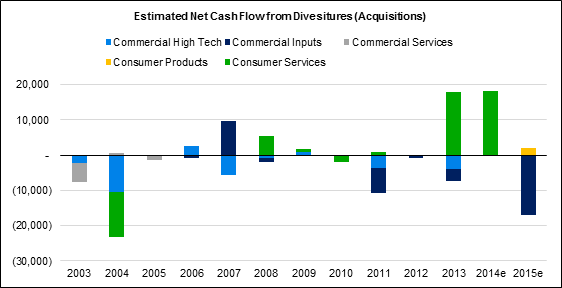

Figure 2. Source: Company Statements, YCharts Research Analysis

Note that pre-financial crisis, the firm was continuing to spend cash on Consumer Services (both financial services and entertainment assets). However, since the financial crisis, there was only one net capital expenditure for Consumer-related categories, and that was actually related to the eventual divestment of NBC.

Commercial Inputs seems smaller in the aggregation, but we can see this is because of a single divestment (of GE Plastics—Jack Welch’s springboard) in the pre-Financial Crisis days—before the PIT strategy was fully formed.

This view suggests that GE has been making strategic but smaller investments in the Tech part of the PIT strategy, but pouring more attention and capital into the Power and Infrastructure areas.

General Electric’s Valuation Drivers

YCharts valuation methodology hones in on three main drivers: Revenue Growth, Profitability, and Investment Level & Efficacy. (For more information, please see our valuation methodology document, available on the YCharts website, in the Resources section.)

We estimate a fair value for a firm by analyzing the company’s present business environment and historical performance in each of the valuation driver areas, and make data-driven, transparent projections for future performance.

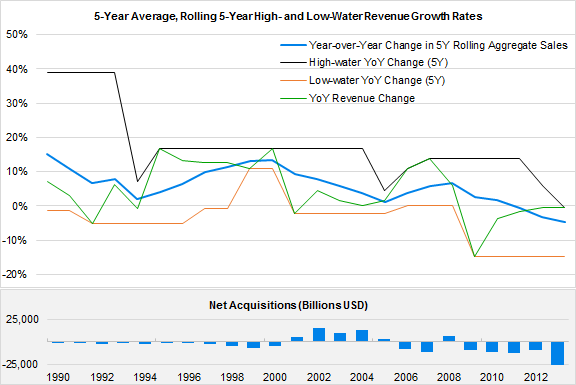

Revenue Growth

The pullback in GE’s revenue growth since 2011 (marked by the thick blue line in the chart above) is not due as much to softening demand, but rather to divestments of NBC (2013), overseas consumer and commercial lending subsidiaries, and currency effects (over half of GE’s revenues are generated outside of the U.S.).

Note the blue bars in the lower half of the graph showing acquisition and divestiture activity. Acquisitions are shown by a positive number, divestitures as a negative one; divestitures have dominated since 2008. Revenue headwinds from the sale of GE's Appliances business and its disposal of the U.S. Consumer Finance business this year will roughly offset the revenues it is purchasing from Alstom AOMFF.

Even after the shuffling of its business mix is complete, GE will likely to continue to acquire attractive assets aligned with its PIT Strategy, so will experience revenue growth through those acquisitions, as well as organic growth from its extant business.

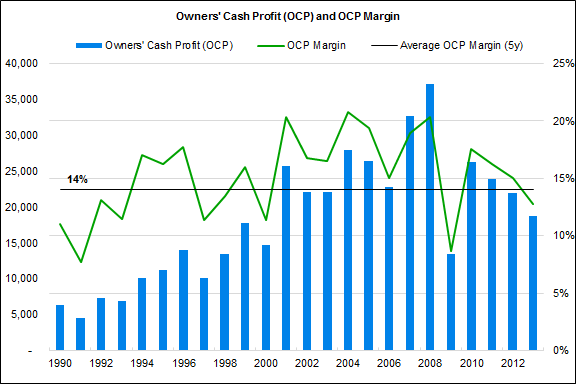

Profits

As you can see in the YCharts Competitor Snapshot on the Diversified Industrial industry, GE profitability is head and shoulders above its average peer. The GE Capital Corp. (GECC) deserves credit for this—not only because financial service margins tend to be higher than manufacturing ones, but mainly because of the complex leasing- and transfer pricing-related tax shelters made possible by GECC’s financial wizardry (these tax shelters and the associated uncertainty around them are discussed in detail in a longer report available on the YCharts website, in the Resources section). The media rails against tax inversions, but one of the marquee names of American industry has been perfecting a more subtle form of this art for 35 years.

The spinoff of the consumer finance business may have the effect of depressing GE margins somewhat. However, this effect will be partially offset by the divestiture of the lower-margin Appliances business.

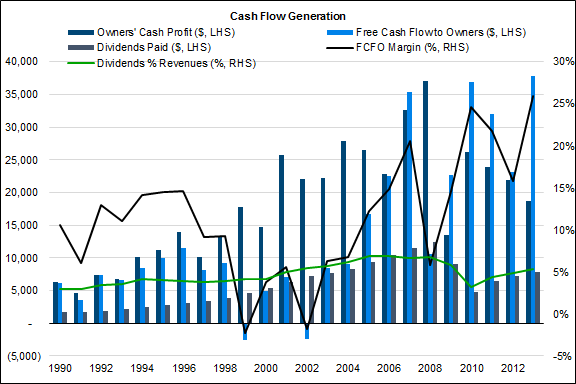

(Owners’ Cash Profits is YCharts’ preferred cash-based estimate of profitability available to owners. It equals Cash Flow from Operations less an allowance for maintenance capital expenditures.)

Investment Level

Recent investment levels have been affected by GE’s efforts to rid itself of customer-facing services businesses—NBC and GE Money in particular (divestments are shown as negative values in the above graph). However, GE will not continue to divest assets forever, and in fact, more overseas acquisitions may be in the works. Immelt has focused on overseas business and increased the revenue share from non-domestic sources by twenty five percentage points since assuming control of the firm. He has also placed renewed emphasis on a strong R&D pipeline, and to the extent that these expenditures can be capitalized, it will show up as an investment in the financial statements.

Note that GE’s most recently announced acquisition of Alstom represents about the equivalent of all of the company’s Owners’ Cash Profit for FY 2013.

Free Cash Flow and Dividends

Our preferred measure of free cash flow—Free Cash Flow to Owners (FCFO)—has fluctuated enormously as a percentage of revenues over the timeframe shown here, thanks to frequent acquisitions and dispositions. The average FCFO margin over the last 10 years has come it at 16%, but we figure that a reasonable expectation for future average FCFO margin is within the 10%-15% range.

Dividend Margin (dividends as a percentage of revenues) is climbing back to pre-Crisis levels and is in the 5% range.

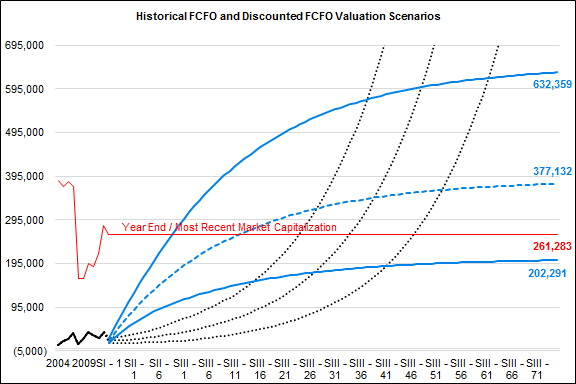

GE Valuation

YCharts uses best-, worst-, and most likely-case scenarios using a three-stage model to derive a valuation range for a company. In the diagram above, projected actual cash flows for each of the scenarios are represented by dotted black lines. Discounted values for each scenario is shown by the dark blue lines.

|

Valuation Assumptions & Scenarios |

|||

|

|

Likely |

Worst |

Best |

|

Revenue Growth |

3% |

1% |

5% |

|

OCP Margin |

16% |

14% |

18% |

|

Expansionary % OCP |

20% |

40% |

10% |

|

Medium-term Growth (years 5-10) |

6% |

3% |

8% |

|

Stage III Assumed Growth |

|

|

6% |

|

Discount Rate |

|

|

10% |

With the assumptions above, we calculated a fair value range for the firm of $20-$63 with a median case valuation of $37 / share. The median case valuation implies a rise of 43% from recent market prices with a fairly moderate downside risk scenario.

[1] Jack Welch did one thing phenomenally well: insisted upon only running businesses that were or plausibly could be #1 or #2 in their industries. Managers of Bronze Medal businesses would have to be content working for an acquirer, because Neutron Jack had no room for #3. Thanks to Welch’s long tenure, this focus on feeding the winners and killing the losers meant that the business that form GE’s core are impressive competitors with formidable moats. These moats differ from business line to business line, but generally rely upon intellectual property, network effects, and governmental access built over years of concerted effort. Don’t believe me? Imagine you are the purchasing manager at Boeing BA and need to buy some jet engines. How likely would you be to go with a state-sponsored Chinese jet engine maker that was offering you a 20% discount on your order compared to GE? Quod Erat Demonstrandum.

[2] Most of the “water” part of this segment should be read as “hydroelectric power”, though there is a bit of infrastructure water—desalinization, wastewater treatment, pumps, valves, etc.

[3] Not all of the sale or purchase amounts were made public, so these figures are estimates and will not agree with figures listed on the financial statements—especially in the early years. Directionally, however we believe them to be representative of the company’s investment activity and strategic focus.