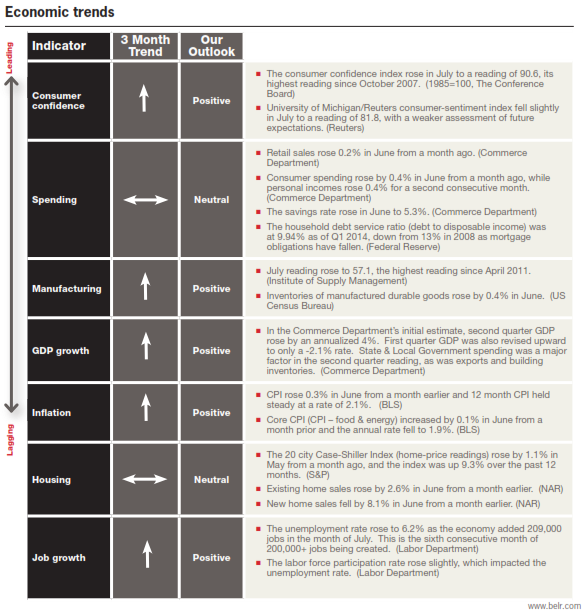

Confidence high with mixed forward expectations

The U.S. economy experienced a robust summer for economic expansion and job growth, however recent consumer data is casting doubt as to whether the current level of activity can be sustained. GDP grew at a 4.2% annualized rate during the second quarter, according to the Commerce Department’s second of three estimates. Job growth was also strong, adding more than 200,000 jobs per month until this most recent reading in August. Businesses continue to cite difficulties in finding qualified workers, which could lead to slowing job growth going forward. Wage growth is an area of continued concern as annual increases hover around the 2% level, barely keeping pace with inflation. For now, we believe the summer momentum will likely continue with strong corporate earnings and a slow moving Federal Reserve acting as tailwinds.

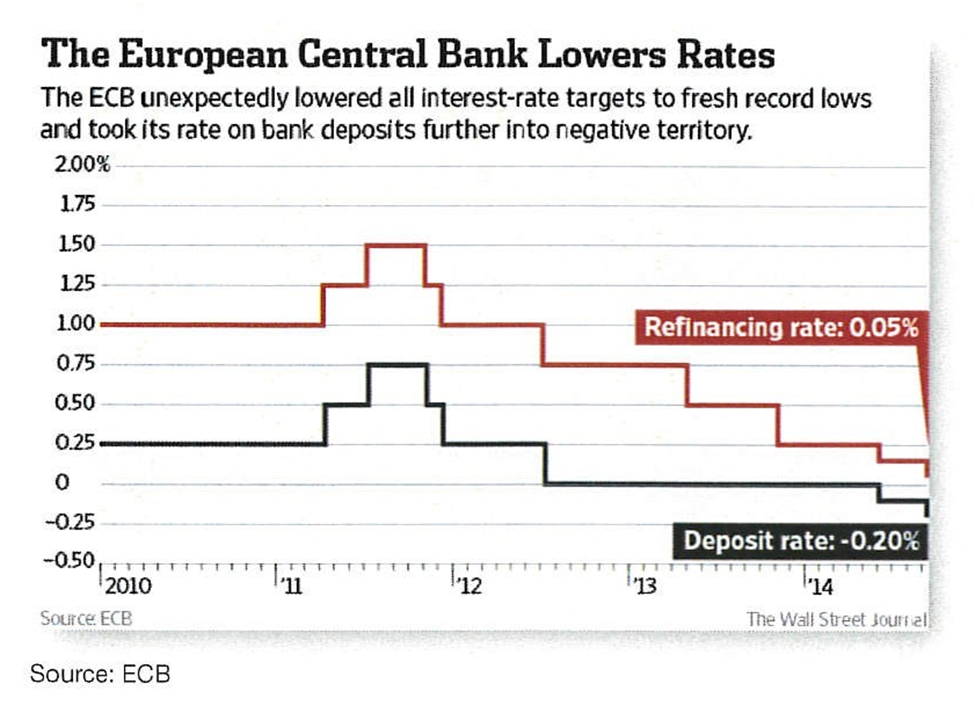

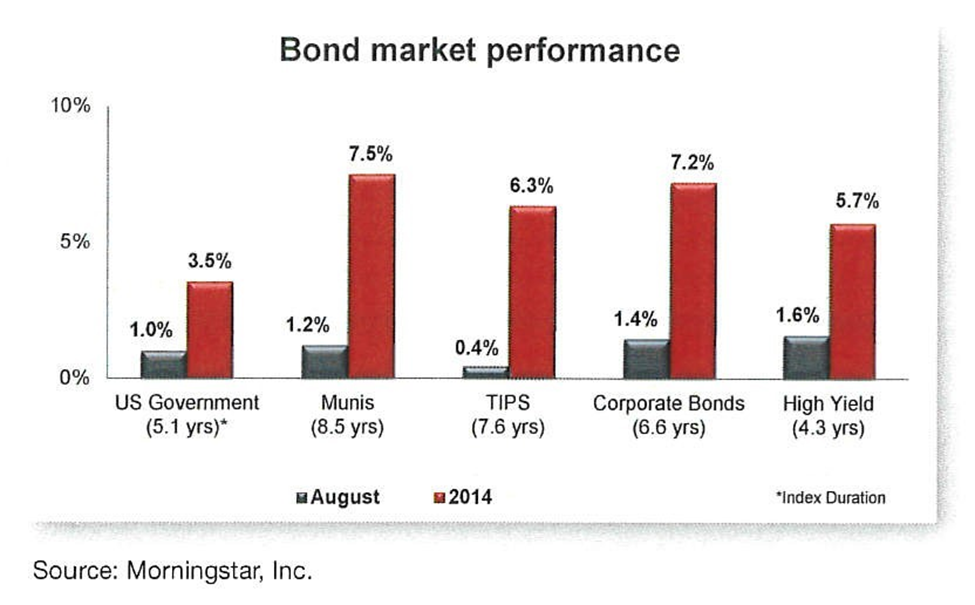

Quantitative easing/ECB policy affect bond yields

The first week of September, European Central Bank President Mario Draghi announced a quantitative easing program and interest rate cut. The ECB is preparing to buy asset-backed securities in an effort to revive lending to small and medium-sized businesses similar to what the United States, Britain and

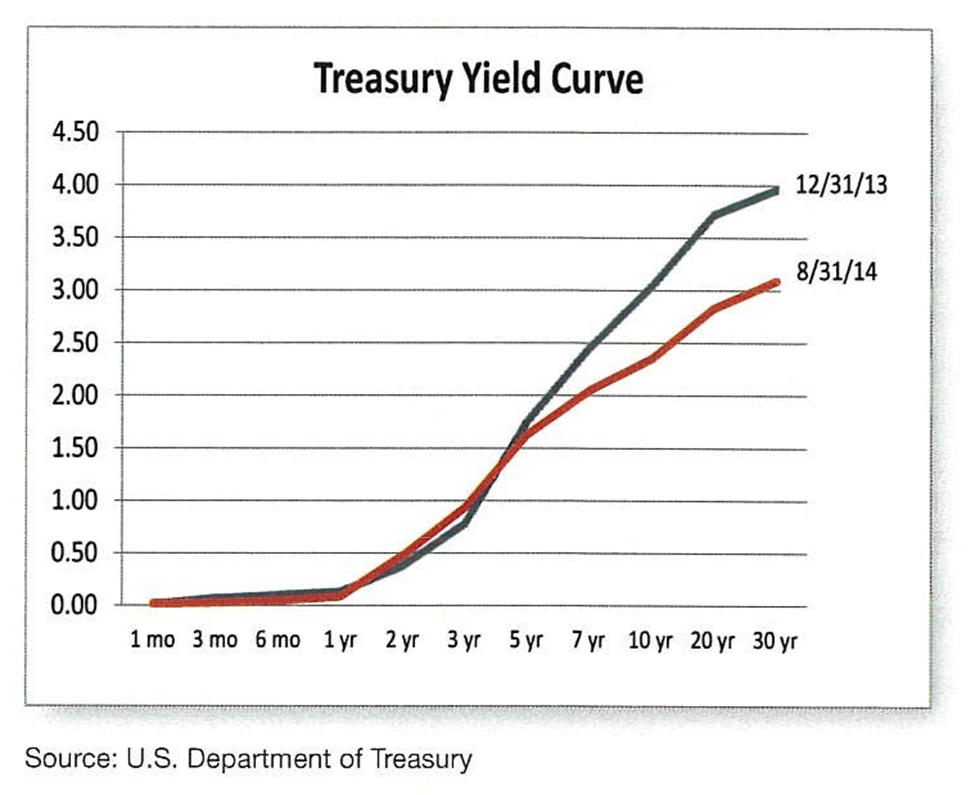

Japan have previously attempted. The amount of the buy- back is expected to be forty billion euros, or $53.3 billion U.S. dollars. This program has pushed already low interest rates even lower on sovereign debt in Europe and Asia. And, with lower bond rates in Europe, investors have continued their migration into U.S. bonds for their perceived security and risk- adjusted yield. In general, the yield curve continues to flatten as the long end of the curve moves downward, signaling a potentially deflationary economy. Our position is to maintain an emphasis on higher-quality bonds and be prepared for short-term rate increase(s) in the months to come.

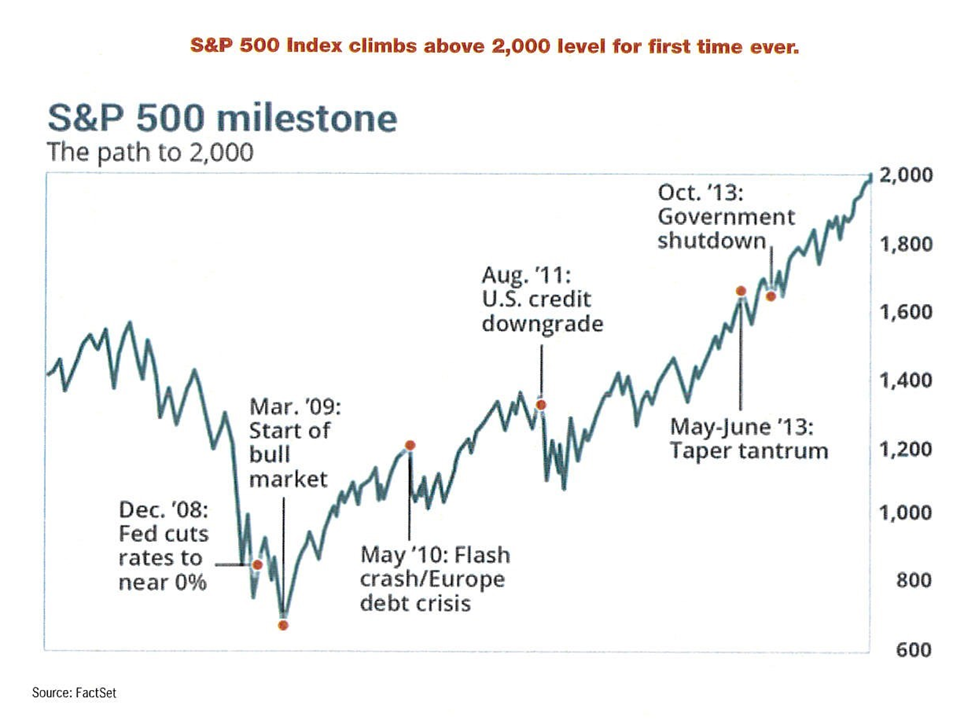

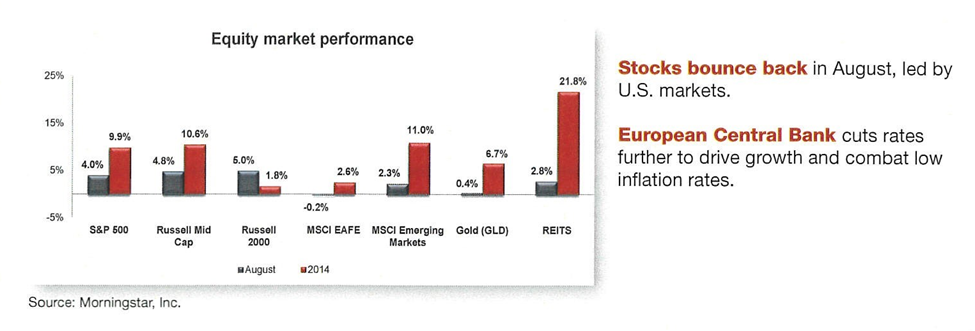

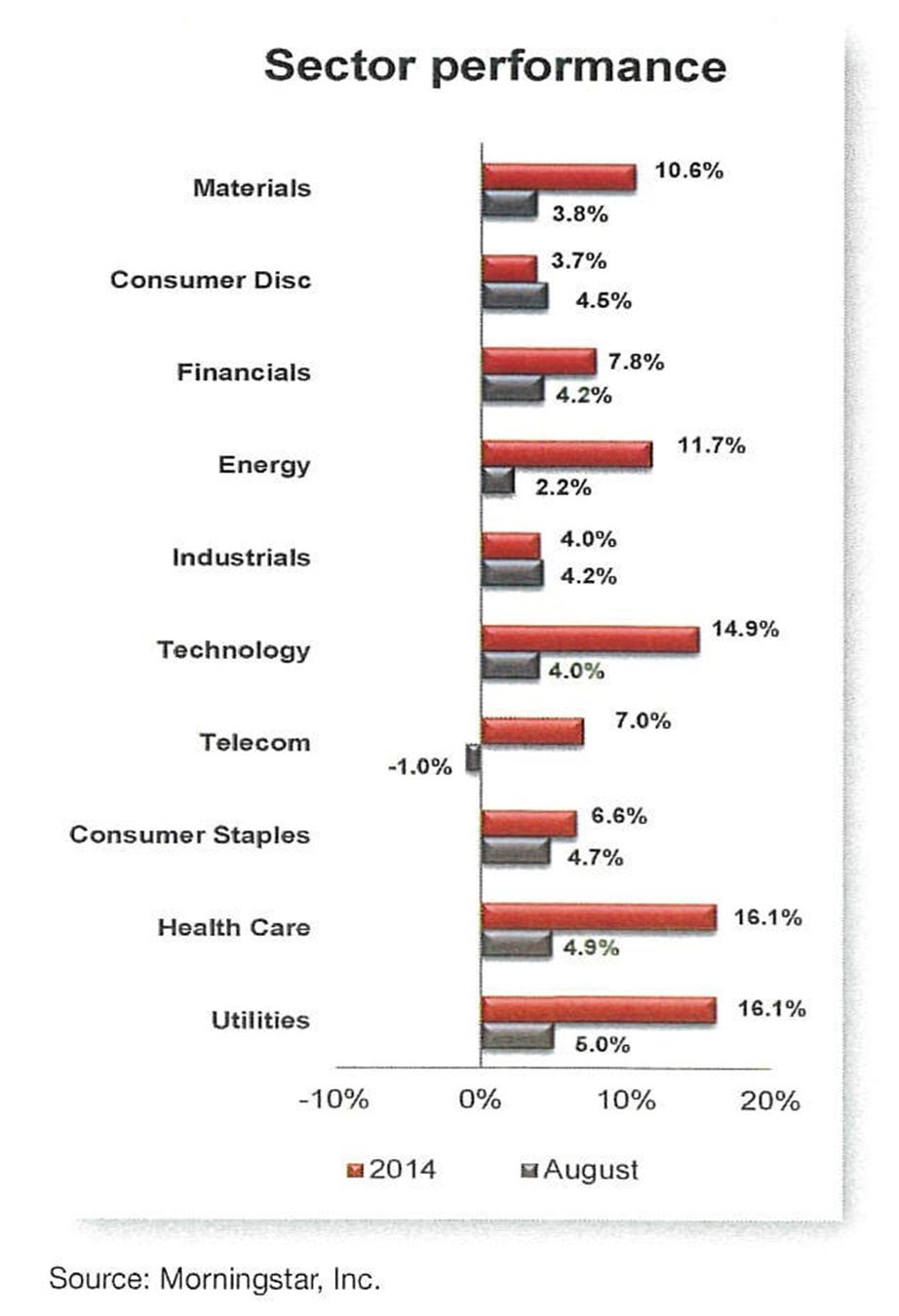

Stocks bounce back in August, attain record highs

The S&P 500 Index closed over 2,000 for the first time ever, while the Dow Jones Industrial Average climbed back over the 17,000 level. Stocks saw a major push to finish the month of August as the European Central Bank hinted at additional stimulus measures. A string of strong economic data also helped, as investors reacted strongly to the positive news. This in contrast to the month of July, when good economic news was viewed as a signal of accelerating monetary tightening by the Federal Reserve, which caused investors to pull back from stocks. While some areas of the market are arguably overvalued, the broad S&P 500 Index has a forward P/E ratio that is consistent with its 25-year average of 15.6x. The road ahead for stocks continues to look positive, but it would be prudent to keep in mind the inevitable speed bumps that will likely present themselves down the road, as we have not had a meaningful pullback since 2011.

|

Indexes |

YTD |

Treasury Yields |

||||

|

Stock Indexes |

Prime Rate |

3.25% |

6-month |

0.05% |

||

|

Dow Jones |

17,098 |

4.84% |

LIBOR Rate (3 mos.) |

0.24% |

1-year |

0.09% |

|

S&P 500 |

2,003 |

9.89% |

Unemployment rate |

6.1% |

2-year |

0.48% |

|

NASDAQ |

4,580 |

10.57% |

15-year mortgage rate |

3.29% |

5-year |

1.63% |

|

Bond indexes |

30-year mortgage rate |

4.18% |

10-year |

2.35% |

||

|

Broad Market Barclays Agg |

4.81% |

CPI (12-mo. ending 7/31/2014) |

2.0% |

30-year |

3.09% |

|

|

US Corporate Barclays Capital |

7.18% |

GDP (second-quarter 2014) |

4.2% |

|||

|

US Government Barclays |

3.54% |

Oil price (price/barrel) |

$95.96 |

|||

|

Mortgage-Backed Barclays |

3.90% |

Gold (oz.) |

$1,286 |

Data as of August 31, 2014 Source: The Wall Street Journal, US Department of Treasury www.belr.com

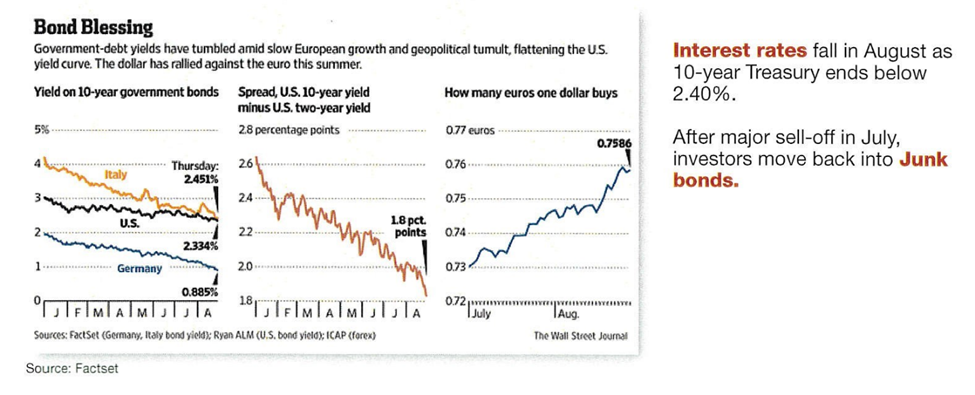

Interest rates fall in August as 10-year Treasury ends below 2.40%. After major sell-off in July, investors move back into Junk bonds.

Bronfman E.L. Rothschild, LP is a registered investment advisor. Securities, when offered, are offered through Baker Tilly Capital, LLC, member of FINRA and SIPC; Office of Supervisory Jurisdiction located at 10 Terrace Court, Madison, WI 53718, phone 800.362.7301. Bronfman E.L. Rothschild, LP and Baker Tilly Capital, LLC are not affiliated.

This publication should not be viewed as a recommendation, an offer to sell, or a solicitation of an offer to buy a particular security or service. The commentary provided is for informational purposes only and should not be relied on for accounting, legal, tax, or investment advice. Financial information is from third-party sources. While such information is believed to be reliable, it is not verified or guaranteed. Performance of any indexes is provided for reference and competitive purposes only without factoring any fees, commissions, and other charges. Individual results achieved by investors will be different from those of the indexes. Indexes are unmanaged; one cannot invest directly into an index. The views and opinions expressed are those of Bronfman E.L. Rothschild, LP, and they are subject to change at any time. Past performance does not imply or guarantee future results. Investing in securities involves risks, including possible loss of principal. Diversification cannot assure a profit or guarantee against a loss. Investing involves other forms of risk that are not described here. For that reason, you should contact an investment professional before acting on any information in this publication.

© 2014 Bronfman E.L. Rothschild, LP