- We continue to expect the Fed to again cut its bond purchase program and remain on pace to exit QE by year end.

- However, odds have increased that the Fed could change “something” at this week’s FOMC meeting, including omitting its promise to keep rates low for a “considerable time” or providing the public with an update to its exit strategy.

- We are continuing to watch our Yellen indicators, including the unemployment rate, the job quit rate, and the output gap, to gain insight into whether the Fed will raise rates sooner than expected.

On Tuesday, September 16 and Wednesday, September 17, 2014, the Federal Reserve (Fed) will hold the sixth of its eight Federal Open Market Committee (FOMC) meetings of the year. This meeting will include a press conference by Fed Chair Janet Yellen and FOMC members’ forecasts for the economy, the timing of the first fed funds rate hike, and the level of the fed funds rate at the end of 2014, 2015, 2016, 2017, and in the long run. In recent years, markets have been conditioned to expect a greater possibility of policy changes at meetings accompanied by press conferences and new forecasts and, as a result, market participants have increased their odds that the Fed will change “something” at this meeting.

Although we continue to expect the Fed will again cut the pace of its bond purchase program (quantitative easing or QE) and remain on pace to exit QE by the fourth quarter of 2014, the odds have increased in recent weeks that the Fed will take some additional action. Arranged from most likely to least likely (in our view), at this week’s meeting the Fed could:

Move to a more “data-dependent” rather than a “time-dependent” promise to keep rates low. Yellen and most other Fed officials have gone out of their way to remind the public that the Fed’s QE program and the extraordinarily low rates are “data dependent,” and yet the FOMC statement continues to hinge on that “considerable time,” or time-based guidance. A subtle shift away from time-based to data-based rate guidance could be one outcome of this week’s meeting.

Change the bar and “dot plot.” At one of her press conferences earlier this year, Fed Chair Yellen referred to the FOMC members’ forecasts of the first rate hike and fed funds rate levels at year end 2014, 2015, 2016, and in the long term as the “dot plots.” To be clear, the timing of the first rate hike appears on a bar chart, while the forecasts for the level of the fed funds rate at year end are found in the dot plots. At the June 2014 meeting, 12 FOMC members said 2015 was the first hike, while one said 2014, and three said 2016. The bar and dot charts are likely to include 2017 this time. The June 2014 dot plots placed the fed funds rate at current levels at the end of 2014, 1.13% at the end of 2015, and 2.50% at the end of 2016. After identifying them as such, Yellen immediately told the public to not pay any attention to them, but of course financial markets and the financial media can’t seem to resist. Given the recent data -- and public pronouncements of FOMC officials on when they thought the first rate hike should occur -- there is likely to be some movement toward a rate hike sooner rather than later and a higher end point for fed funds in both the bar and dot plots this time around.

Drop the “significant underutilization of labor resources” language from the FOMC statement. This language was inserted into the statement released after the July 29 - 30, 2014, FOMC meeting and was likely designed to focus the market’s attention away from the headline labor market indicators -- such as the unemployment rate and the nonfarm payroll job count -- and on the broader set of labor market indicators often cited by Fed Chair Yellen and Fed staffers. Although several of the Yellen indicators have indeed improved since the July 2014 FOMC meeting, the majority of the Yellen indicators still suggest that the broad labor market is not back to normal. Our view is that although this description is unlikely to be dropped altogether, it could be softened a bit to reflect the ongoing -- albeit slow -- improvement in the labor market.

Omit from the FOMC statement the promise to keep rates low for a “considerable time” after QE ends. This is a close call. The recent run of better-than-expected economic data for the second and third quarters of 2014, along with recent comments from Fed officials (both hawks and doves*), support this view, but the sudden shift in policy implied in omitting these words seems out of line with the Fed’s recent gradualist approach.

Provide the public with an update to its “exit strategy,” first outlined in 2011. In our view, the sooner the Fed does this the better it will be in the long run. However, our read of recent comments from Fed officials, the June and July 2014 FOMC statements, and the minutes of the July 29 - 30 FOMC meeting suggest the FOMC subcommittee that was set up to review the exit strategy most likely has not had enough time to complete its task. With the next FOMC meeting (October 28 - 29, 2014) not scheduled to have a Yellen press conference or a new forecast, the final FOMC meeting of 2014 (December 16 - 17) is the likely date for the Fed to announce the long-awaited update to its exit strategy. If the Fed were to announce that a press conference would accompany the October FOMC, that would likely signal to the markets that the Fed was preparing to announce its exit strategy in October.

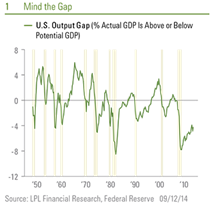

The one common thread to the potential changes from the Fed is how the economy is tracking to the Fed’s forecast, and when all of the slack in the economy -- as measured by the output gap [Figure 1] -- will be taken up. If the economy (as measured by growth in inflation-adjusted gross domestic product [GDP]) continues to grow at around 4% as it has, on average, in the second and third quarters of 2014, the output gap is likely to close much more quickly than the Fed now assumes, and the Fed will likely be raising rates in the early part of 2015. If GDP decelerates in 2015 and 2016 to the 3% pace forecast by the FOMC, the Fed is likely to begin hiking rates later in 2015 -- perhaps in Q3 or Q4. If, however, the economy returns to the below-average 2% pace of growth seen in 2011 - 2013, the Fed could be on hold until late 2015 or early 2016. We are continuing to watch our Yellen indicators, including the unemployment rate, the job quit rate, and the output gap, to gain insight in whether the Fed will raise rates sooner than expected.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

The Federal Open Market Committee (FOMC), a committee within the Federal Reserve System, is charged under the United States law with overseeing the nation’s open market operations (i.e., the Fed’s buying and selling of U.S. Treasury securities).

*Hawks: Fed officials who favor the low inflation side of the Fed’s dual mandate of low inflation and full employment; Doves: Those favoring the full employment side.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1-308011 (Exp. 09/15)