Executive Summary

The U. S. financial system is going through profound changes. In the early 1980s, interest rates began to fall and bond prices began to rise, causing financial services firms to shift behavior to capitalize on this trend. Balance sheets became more levered and complicated, and income streams were enhanced by new, untested loan products. In addition, regulatory control waned as belief grew that adaptive “market forces” were better than static regulation.

In 2007, the financial system began to unravel due to excessive leverage, credit risk and overall business complexity. This led to the “Great Recession,” as lending and liquidity quickly dried up around the globe. Bankruptcies and forced mergers ensued, lending was significantly curtailed and companies and consumers reigned in spending as their trust in the system plummeted. The subsequent response by Central Banks around the world was unprecedented.

We believe the financial sector has now stabilized. Regulatory controls have been modernized, while leverage, risk and complexity within the system have been significantly reduced. Companies are experiencing increased loan demand and better lending revenues and are showing a renewed attention to costs and operational efficiency.

As we look forward, we see a potentially more stable profit picture developing for these firms. And, a rising interest rates environment has historically translated to increased revenue for banks and financial institutions.

In short, we believe the financial sector is ripe with opportunity.

THE MASS DISLOCATION IN CREDIT MARKETS

To appreciate the banking environment today, a brief review of history is needed. In the years leading up to the most recent economic recession, the U.S. experienced a housing boom driven by low interest rates, easy credit and overly accommodative underwriting practices. Many large financial companies engaged in the complex packaging of debt instruments that leveraged the U.S. financial system to extreme levels.

One way to understand the extreme risk is to look at the balance sheet of the largest U.S. financial institutions as if they were one company. At the end of the third quarter of 2008, these institutions were leveraged almost 40-to-1, with $7 trillion in illiquid securities and loans financed to a large extent with short-term, variable-rate borrowings.1

When the housing bubble burst, vulnerabilities were exposed. Many financial companies faced capital shortfalls and, ultimately, failed or were forced to merge.

Lehman Brothers’ bankruptcy in September 2008 elevated the panic in the markets. In a series of articles on the effects of the financial crisis, The Economist described it in this manner:

“Suddenly, nobody trusted anybody, so nobody would lend. Non-financial companies, unable to rely on being able to borrow to pay suppliers or workers, froze spending in order to hoard cash, causing a seizure in the real economy.”2

This mass dislocation in the credit markets caused the U.S. to fall into a recession. Construction projects diminished, the real estate market collapsed, the stock market plunged and unemployment rose.

Tightened Lending Standards Emerge

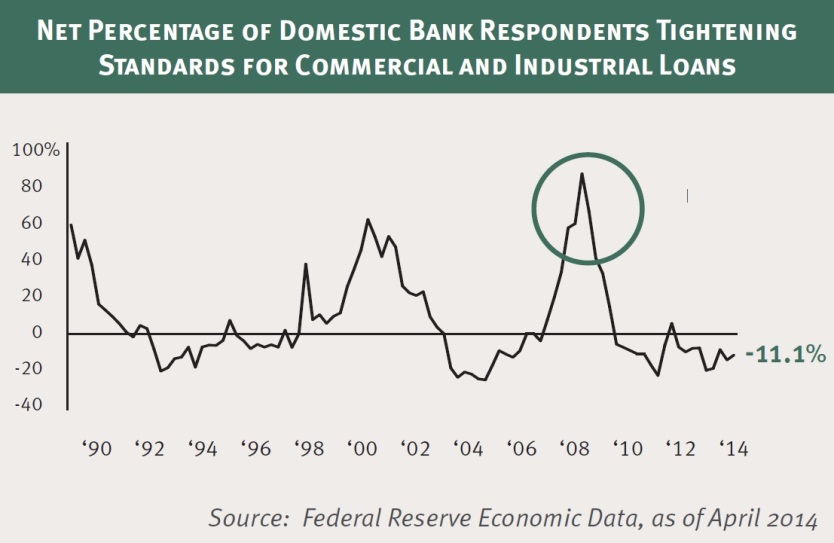

Once lending restarted, banks severely reversed their lenient ways. According to an October 2008 Federal Reserve Board’s Senior Loan Officer Opinion Survey on Bank Lending Practices, nearly 80% of domestic banks responded that they tightened their lending standards for commercial and industrial loans over the previous quarter. This was the highest percentage of banks indicating that they had tightened lending standards since 1990.3 Standards were also tightened for commercial real estate loans and consumer credit card loans during the same period.

For consumers and aspiring entrepreneurs to receive loan approval, banks required higher credit scores and larger down payments. Institutions and corporations faced higher interest costs. Banks tightened credit line availability and increased rates on secured and unsecured loans. Banks also tightened covenants on loans, lowered the maximum loan size and reduced the maximum maturities allowed.

As a result of this tightening of lending standards, banks currently have a higher quality loan portfolio. This development has also reduced bad credit costs and increased quality and long-term stability of earnings.

Competitive Advantages of Small-Cap Banks

Many small banks have relatively straightforward business models, where they earn money by taking short-term deposits and making long-term loans, carefully maintaining a balance between assets and liabilities. This function is essential to the local economy, with community banks providing nearly half of all small-business loans, 35% of commercial real estate loans and about 16% of residential mortgage lending as of 2010.4

While recognizing that there continued to be “considerable revenue pressure from low margins,” in May 2014, Federal Reserve Chair Janet Yellen said the following:

“Earnings for most community banks have rebounded since the financial crisis. Asset quality and capital ratios continue to improve, and the number of problem banks continues to decline. Notably, after several years of reduced lending following the recession, we are starting to see slow but steady loan growth at community banks.”5

» Loan Growth

For smaller banks, loan balances and growth are critical as a primary source of revenue generation. Interest and fees earned from loans comprise a majority of their revenues.

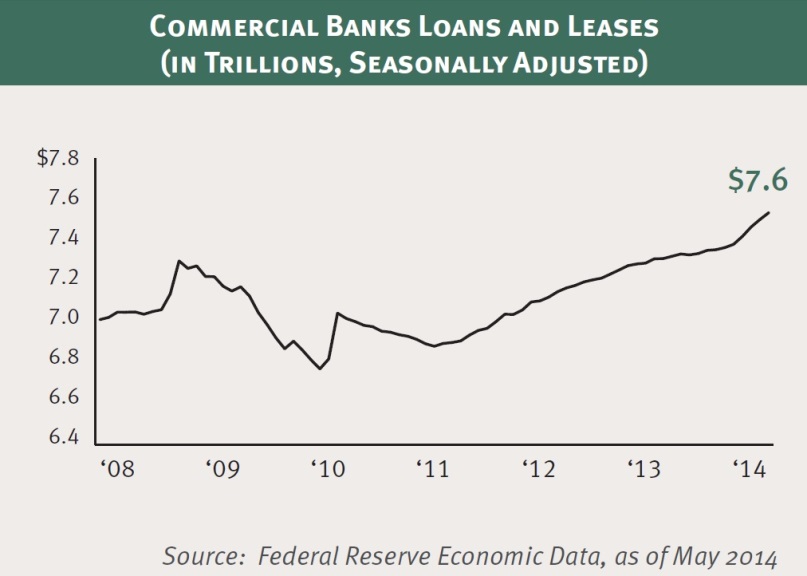

While loan growth has been difficult to cultivate in recent years, the industry has been witnessing signs of improvement. Following 2008, loans and leases held at commercial banks sunk from a high of about $7.3 trillion in the fall of 2008 to below $6.6 trillion at the beginning of 2010. By 2011, the figure began to slowly increase. In 2014, loan levels have risen to a record high.

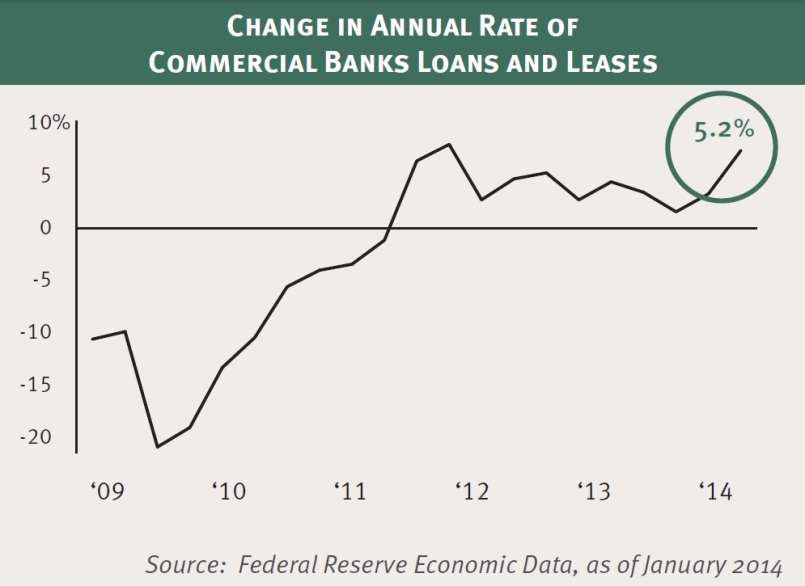

The pace of growth has been strengthening as well, as the annual rate of change of the loans and leases spiked in 2014. While the level has plateaued since 2011, a lift in recent data suggests an upward trajectory that we expect will continue due to rising consumer confidence and an improving economy.

» Potential for Rising Interest Rates

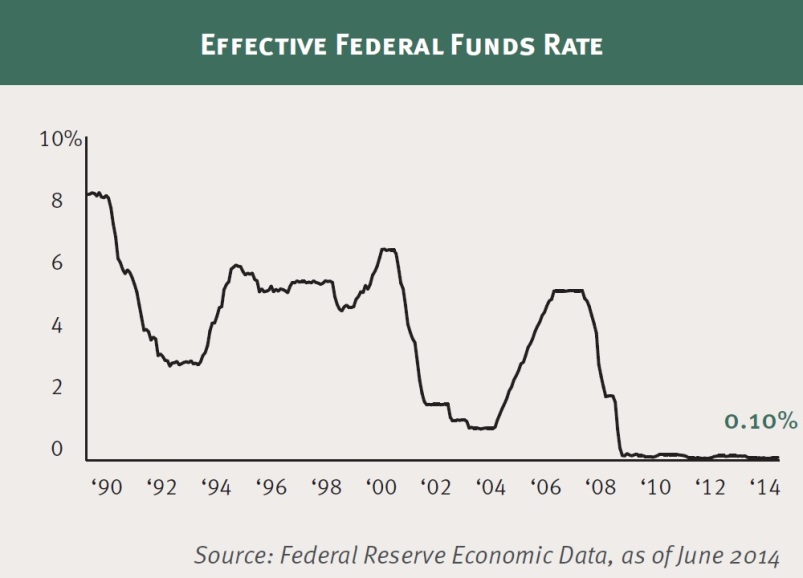

The U.S. has experienced more than a decade of low interest rates. The 10-year Treasury rate has been below 5% since 2002 and only since the summer of 2013 has the 10-year rate climbed above 3%. Likewise, the Federal Funds Rate, which is the interest rate at which depository institutions lend money to each other, has remained at low levels, with the Fed holding the rate just above 0% since the end of 2008.

As the economy continues to slowly improve, we expect the Fed will gradually increase interest rates, bringing an end to the era of record low rates. While rising rates may not be good news to business owners in need of a loan, rising rates offer positive leverage for banks, providing a top-line revenue boost. Even with a relatively small rate increase, smaller banks have historically experienced higher margins and higher profitability.

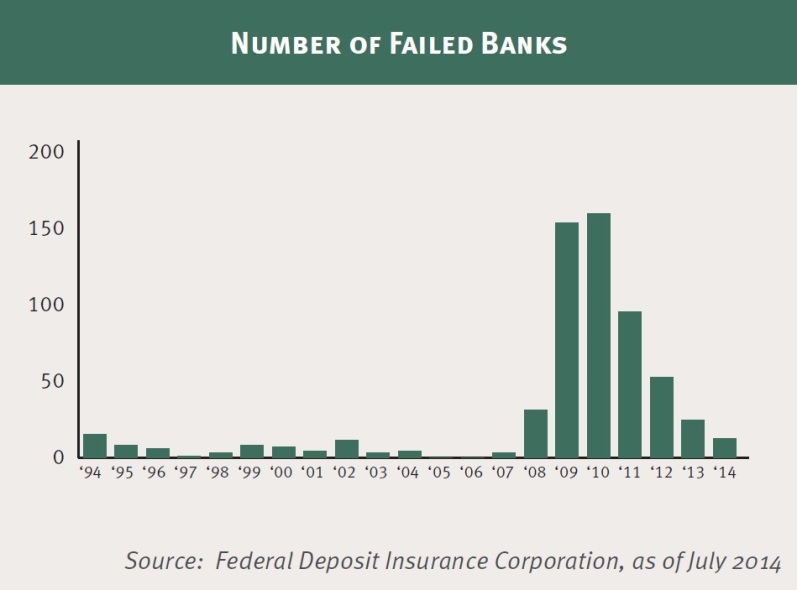

» Reduced Number of Bank Failures

Following the financial crisis, there was a wave of bank failures, with the number of failed banks rising to the highest level in 20 years. In 2009, over 140 banks were shuttered and in 2010, an additional 150 banks were closed by regulators. Many of these banks were burdened by balance sheets laden with failed commercial real estate loans for new housing developments, strip centers and office projects. With some of these sizable deals falling apart, lenders needed to raise capital and cover their losses.

In recent years, the number of failed banks has been falling and is moving toward the long-term norm.

As a potential alternative to shutting their doors, small banks are engaging in a rising number of mergers and acquisitions (M&A). With new regulations to meet—and hence, additional compliance costs—merging with or acquiring another bank can help spread those costs. According to the credit ratings and research company, Fitch Ratings, smaller banks in the U.S. with assets of less than $10 billion are “stepping up M&A activity at a time when weak organic growth prospects and rising regulatory costs are driving a need for increasing scale.”6

Competitive Advantages of Large Banks

Many large banks differ from smaller commercial banks in that they generate revenue via many different business lines, such as equity and fixed income securities trading, investment banking, wealth management and mortgage servicing. These institutions manage thousands of branch locations and employees, complex balance sheets, and numerous assets and liabilities.

Following the credit-driven cycle, many large banks have become more focused on improving the overall construction of their balance sheets. As opposed to overleveraging to enhance profitability, these large banks are focusing on operating their various business lines in the context of a new regulatory environment and a higher interest rate cycle. Therefore, many are restructuring and simplifying their businesses to develop a more stable balance sheet and income statement.

» Thriving in a Strict Regulatory Environment

Since the Great Recession, companies have had to navigate and reorganize around a new regulatory regime. The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 brought significant reforms to the financial industry with the intention of preventing bank collapses.

Filling over 800 pages, the Act has been criticized for its cumbersome, overbearing rules and regulations that are expensive to implement. Chairman and CEO of JPMorgan Chase Jamie Dimon has been one of the more outspoken voices in terms of its burden on the banking industry. In his 2012 letter to shareholders, he estimated that over the next few years, “tens of thousands” of JPMorgan Chase employees would “work on these changes, of whom 3,000 will be devoted full time to the effort, at a cost of close to $3 billion.”7

However, history indicates regulations are not necessarily detrimental to the banking industry. Following the thrift bailout cycle of 1987 to 1992—a period plagued with comparable liquidity and capital problems—a tremendous amount of regulations was implemented. After cleansing balance sheets and changing the mindset of the industry, financial stocks experienced one of their best periods of capital appreciation.

We believe regulation protects the integrity of the system. It adds clarity to banks’ operating condition and their potential. The quality and construction of balance sheets improve as banks reduce leverage, risk and complexity. High-quality management teams learn to thrive in and adapt to a strict regulatory environment. They seek to understand the rules, improve their business under the new regulations, and take business from competitors that are less nimble. The result is a reinvigorated lending infrastructure, which we believe drives a healthier banking system.

» Some Large Banks are Profitable with Sufficient Capital

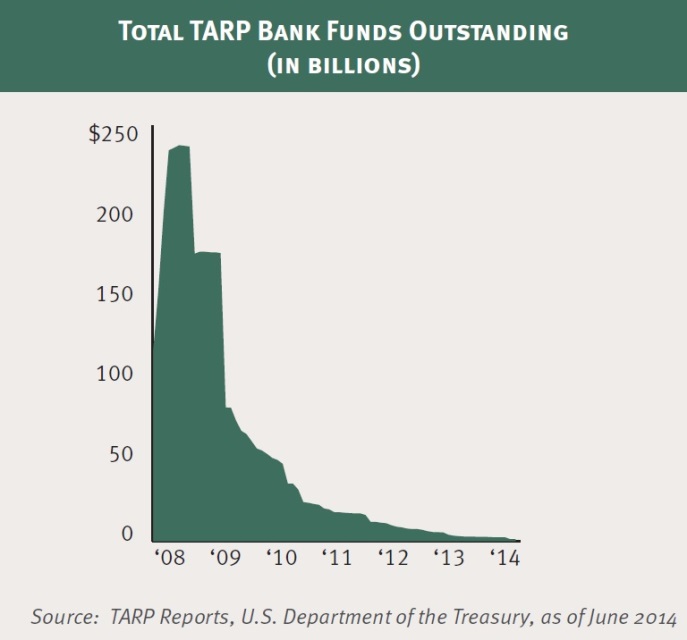

The government’s bailout program, the Trouble Asset Relief Program (TARP), was created to stabilize the banking system and get credit flowing again following the financial crisis. Approximately $245 billion was spent on bank investment programs, including one providing capital to financial institutions to bolster their capital positions.

As of June 2014, the total outstanding TARP amount shrunk from nearly $245 billion to $1.2 billion, as banks repaid their balance through principal and interest payments. The Treasury continued to wind down its remaining bank investments: Of the banks that still have TARP funds outstanding, only two banks have totals above $50 million.

Many banks were eager to repay the funds received by the government to prove to shareholders that their profits are solid and their businesses are well-capitalized.

» Increased Dividends and Share Buybacks

In 2008 and 2009, dividends at several banks were severely cut. In some cases, regulators pressured banks into cutting the dividend altogether after requiring a higher level of capital reserves to cushion against losses. As part of the Fed’s Comprehensive Capital Analysis and Review (CCAR, or the “stress test”), the central bank checks for “strong capital levels” to help “ensure that banking organizations have the ability to lend to households and businesses and to continue to meet their financial obligations, even in times of economic difficulty.”

It’s important to note that the CCAR for 2014 assumed banks should be able to continue to operate under a draconian scenario, where GDP falls to a negative run rate of -4.0%, unemployment rises to 11.3%, home prices drop by 26%, commercial real estate prices fall by 35%, the 10-year treasury yield falls to 1.0%, and the stock market falls by 50%.

Even under this extreme case, 29 of the 30 total bank holding companies, which represent 75% of the industry, met the minimum post-stress tier-1 common ratio of 5% in 2014. The tier-1 common equity ratio is a measure of a bank’s financial strength and compares its high-quality capital to riskier assets. According to the central bank, “U.S. firms have substantially increased their capital since the first set of government stress tests in 2009.” In fact, from the end of 2008 through 2012, the amount of high-quality capital held in the largest banks has more than doubled as a result of the annual stress tests and capital planning processes.8 The Fed expects this improvement to continue.

Following the Fed’s approval of its capital plan in 2014, several banks announced increases in dividend payments and stock buyback programs. In 2014, Wells Fargo increased its dividend rate by approximately 17% in the second quarter and plans to increase its repurchases of common stock.9 JPMorgan Chase increased its dividend payment by 5% in the first quarter of 2014 and the company also announced it would repurchase $6.5 billion of common equity over the next 12 months.10

Final Thoughts

The financial sector has changed dramatically, as it rebuilds following one of the most challenging periods in its history. While there were some notable firm failures and government-assisted mergers, most of the industry survived the worst of the crisis and appear to be well positioned to grow profits as the economy recovers. These companies have improved their balance sheet structure, raised standards for loan underwriting, reduced operating costs, and adjusted to heightened regulation.

We are enthused by the current banking environment and believe the industry, once again, holds compelling investment opportunities. However, not all companies hold the same potential, which we believe underscores the importance of active management when investing in the financial services sector.

Our goal has always been to build a portfolio of high-quality companies with geographic diversity, strong growth potential, well-structured balance sheets, high-quality management, and favorable relative valuation. Among our universe of approximately 700 banks and financial services companies, we believe there is an ample number that meet these criteria.

As the U.S. achieves stronger economic growth and enters a period of higher interest rates, the investment opportunity in the financial services sector appears promising. We believe a strong and well-constructed financial system is essential to a healthy economy and, by association, a healthy stock market.

About The Author

David Ellison

Portfolio Manager

Mr. David Ellison brings over three decades of investment management experience to Hennessy Funds and he has been recognized by Morningstar as the most tenured mutual fund portfolio manager in the Financial Services sector.

Prior to joining Hennessy Funds, Mr. Ellison served as President & CIO of the FBR Funds, where he launched and oversaw the line-up of ten FBR Funds. Mr. Ellison began his career at Fidelity, where he managed the Select Home Finance Fund, and he developed his investing discipline and strategy under the tutelage of famed value-investor, Peter Lynch.

Mr. Ellison received a BA in Economics from St. Lawrence University and an MBA from Rochester Institute of Technology.

Important Disclosure

1 Citigroup, Bank of America, JP Morgan, Wachovia, Wells Fargo, Morgan Stanley, Merrill Lynch, Goldman Sachs, Lehman Brothers, and GE Credit

2 “Crash course: The effects of the financial crisis are still being felt, five years on,” The Economist. September 7, 2013.

3 Senior Loan Officer Opinion Survey on Bank Lending Practices, Federal Reserve Board, April 2014.

4 Marsh, Tanya D., Norman, Joseph W. “The Impact of Dodd-Frank on Community Banks,” American Enterprise Institute, May 2013.

5 Yellen, Janet L., “Tailored Supervision of Community Banks,” Presented at the Independent Community Bankers of America 2014 Washington Policy Summit, Washington, D.C., May 1, 2014.

6 “US Community Banks Stepping Up M&A Activity,” Fitch Ratings, February 20, 2014.

7 Dimon, Jamie. JPMorgan Chase shareholder letter, March 30, 2012.

8 Board of Governors of the Federal Reserve System, October 24, 2013.

9 “Wells Fargo Receives No Objection to its 2014 Capital Plan,” Wells Fargo, March 26, 2014.

10 “JPMorgan Chase Plans Dividend Increase and $6.5 Billion Capital Repurchase Program,” JPMorgan Chase, March 26, 2014.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. This and other important information can be found in the Fund’s statutory and summary prospectuses. To obtain a free prospectus, please call 800-966-4354 or visit hennessyfunds.com. Please read the prospectus carefully before investing.

Mutual fund investing involves risk; Principal loss is possible. A non-diversified fund, one that may concentrate its assets in fewer holdings than a diversified fund, is more exposed to individual stock volatility than a diversified fund. Investments focused in the financial services industry may be adversely affected by regulatory or other market conditions such as rising interest rates. The Funds invest in small and medium capitalization companies, which involves additional risks such as limited liquidity and greater volatility. Because the Small Cap Financial Fund focuses on financial services companies that may invest in real estate, the Fund is subject to the risks associated with ownership of real estate and the real estate industry such as fluctuation of real estate values, changes in economic conditions, interest rates and government actions.

References to other mutual funds should not be viewed as an offer of those securities.

The Hennessy Funds are distributed by Quasar Distributors, LLC.