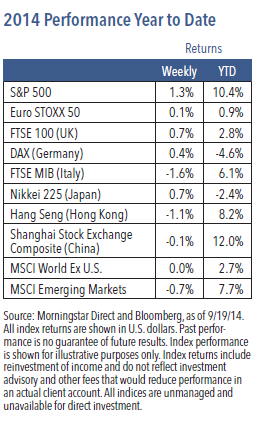

Equity markets rose again last week, with the S&P 500 Index climbing 1.3% and reaching another record high.1 Bond yields and the U.S. dollar drifted higher, while emerging market equities and commodities struggled.2 Two major events that resulted in a continuation of the status quo helped market sentiment. First, last week’s closely watched Federal Open Market Committee meeting produced no surprises and no real changes. And second, the vote for Scottish independence was defeated. Investors appeared to breathe a collective sigh of relief following both events.

The Fed Signals Rate Increases for Next Year

In its policy statement last week, the central bank essentially kept its view of the economy unchanged, pointing out that the labor market still has quite a bit of slack. The Fed also retained the phrase “considerable time” in its comments about how long it intends to keep rates anchored at near-zero.

In all, we view last week’s Fed news as benign for equities and modestly negative for bonds. We do think we are moving into a period of murkiness around Fed policy, which could result in additional volatility in both the equity and bond markets. We expect the Fed will begin raising rates in the first half of next year.

Weekly Top Themes

1. Third quarter economic growth appears to be tracking close to 3.5%. Last week’s data was mixed, with housing market numbers looking somewhat weak, but jobless claims falling more than expected.3 Overall, we believe the data show U.S. growth is continuing to accelerate.

2. The Consumer Price Index (CPI) fell for the first time in nearly 18 months.4 Headline CPI declined 0.2% in August and both headline and core CPI are now up 1.7% on a year-over-year basis.4 Looking ahead, we expect inflation to gradually trend higher, but rising inflation is far from being an issue.

3. Small cap stocks have underperformed large caps (as measured by the S&P 500 Index) so far this year,1 and we expect this trend will continue. At least some of this underperformance can be attributed to investors anticipating that Fed rate increases will remove some liquidity from the markets.

4. We expect commodity prices will continue to fall. Slowing growth in emerging markets (particularly China) and a stronger U.S. dollar have been hurting commodity prices. We expect these trends will continue, and expectations of Fed tightening are likely to put further downward pressure on this area of the market.

5. The period following mid-term elections has been historically strong for equities. According to BCA Research, since 1950, the S&P 500 Index experienced positive returns in every six-month period following the last 16 midterm elections, with an average gain of 16%.5

The Recipe for Further Equity Advances Appears Set

Although global economic growth has remained uneven, and parts of the world continue to struggle with high debt levels, equities have been able to maintain a surprisingly strong bull market. Accommodative monetary policy around the world has certainly helped as it has promoted high levels of liquidity and encouraged risk taking among investors.

Flare-ups in geopolitical hotspots have not yet been able to derail the markets, though that remains a possibility. The eurozone continues to face challenges but has remained relatively resilient in the face of the ongoing Russia-Ukraine conflict. And despite rising tensions in the Middle East, oil prices have been falling, which has been helping global economic growth.

Our view is that the broad backdrop should be conducive to continued equity market outperformance. We still expect to see a market correction at some point (perhaps one sparked by rising bond yields). But for now, we believe the economic environment and financial market fundamentals suggest equities should continue to outperform bonds. Some market participants speculate that equities are getting overheated and are approaching bubble territory, but we think such fears are premature. We believe equities should be able to make continued gains before this bull market ends.

1 Source: Morningstar Direct, as of 9/19/14 2 Source: Morningstar Direct and Bloomberg, as of 9/19/14 3 Source: U.S. Departments of Commerce and Labor 4 Source: U.S. Department of Labor 5 Source: BCA Research

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2014 Nuveen Investments, Inc. All rights reserved.

GPE-BDCOMM4-0914P 3234-INV-W09/15