There have been a lot of bad movie sequels. Remember Ghostbusters II? Grease 2? Blues Brothers 2000? In the case of this Weekly Market Commentary, “Don’t Fight the Fed ECB? (Part 2 of 2),” we hope you find the sequel at least as good as the original, perhaps something closer to The Godfather: Part II than The Godfather: Part III.

Last week we answered the question of whether the latest bold stimulus measures by the European Central Bank (ECB) are a buy signal for European equities. We highlighted key differences between buying Europe now and the United States several years ago during the start of the Federal Reserve’s (Fed) quantitative easing (QE) programs. The different pictures for growth, valuations, and corporate profits in Europe versus the United States lead us to conclude that we should take a broader view to evaluate the investment opportunity in Europe. To that end, this week we take a deeper dive into the investment opportunity in Europe and evaluate fundamentals, valuations, and technicals — none of which we find particularly compelling at this time.

What We Would Like to See to Get More Positive on Europe

Higher inflation. Inflation rising back above 1% would suggest the ECB’s asset-backed securities purchase plan is helping to avert deflation.

Stronger loan demand. More loan demand would be welcomed as a sign that the fractured banking system is being repaired and no longer constraining growth.

Lower earnings expectations. More realistic earnings expectations that are more easily achievable may help reduce risk of market sell-offs in response to earnings failing to meet forecasts.

Cheaper valuations. European stocks usually trade at a discount to U.S. stocks due to a different sector mix and slower growth, but we don’t find the current discount attractive.

Better relative strength. We would like to see European stocks establish relative momentum versus the United States before becoming more positive on the region.

A Broader Look at Europe

Although we view the ECB stimulus measures positively, the differences between Europe now and the United States a few years ago, and the fact that Europe’s stimulus moves may not be as effective as what the United States has done, tell us not to overemphasize the ECB in making decisions on Europe. So we turn to our investment process, with its emphasis on fundamentals, valuations, and technicals, and look at some of the key factors that shape our current view of European equity markets:

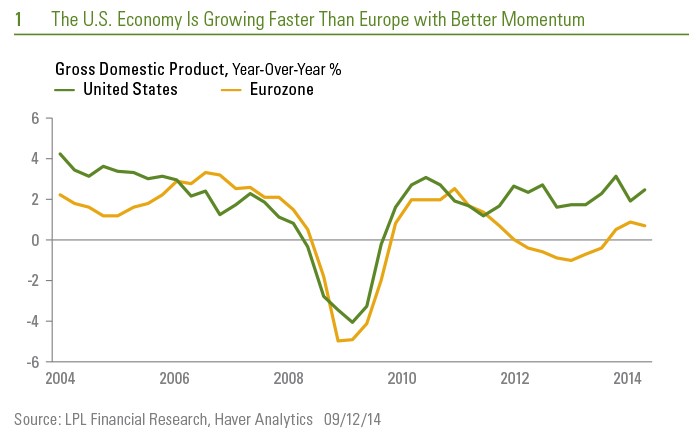

- Economic growth is lackluster. The latest ECB action was driven by the dismal set of Eurozone economic data for July and August 2014, which highlights the lackluster economic growth Europe is experiencing and increases the risk of a growth shortfall in the coming months. Eurozone economic confidence dipped to 100.6 in August 2014, a nine-month low. German unemployment unexpectedly rose in August, and retail sales in Italy in July were down 2.6% from a year ago. Based on the forward-looking components of the data released for July and August 2014, we do not expect near-term improvement in the sluggish 1% pace of gross domestic product (GDP) growth in the Eurozone, and the risk of recession has risen.

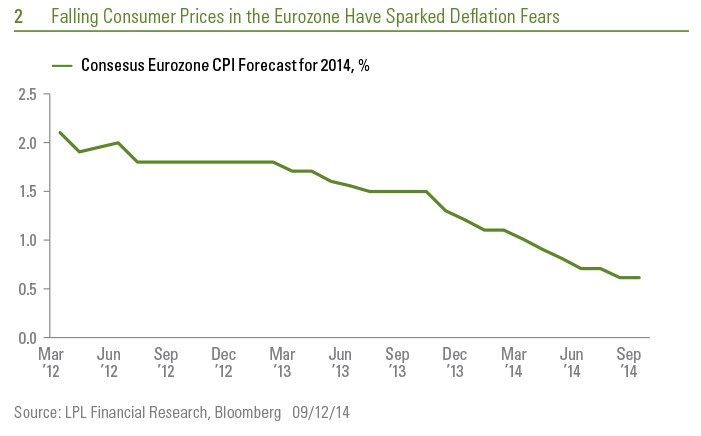

- Deflation risk is rising. Sluggish growth has led to lower inflation and increasing fears of deflation in the Eurozone. The most recent inflation reading for August 2014 of 0.3% year over year (based on the Consumer Price Index [CPI]), well below the ECB’s 2% target and the lowest level since just after the financial crisis, is cause for the ECB’s and investors’ concern. Low inflation expectations are also worrying. During the past year, Bloomberg-tracked economists’ expectations for the Eurozone’s CPI for 2014 have fallen from 1.5% to 0.6% [Figure 2]. In Spain, deflation has already taken hold, with its August 2014 CPI reading down 0.5% from the year-ago period. Italy has seen similar declines in prices. Even Germany’s somewhat healthier economy saw prices rise just 0.8% from a year ago, well below the ECB’s 2% target.

The financial transmission mechanism in Europe is still not working. Unless the fractured banking system can be repaired, the impact of the ECB’s just-announced asset-backed securities (ABS) purchase plan, or even outright QE, could be muted. The necessary credit to fuel economic growth is not getting through the banks to the businesses — particularly small businesses — and households that need it, due to the fractured European banking system (discussed in our Weekly Economic Commentary, “Central Bankapalooza,” on September 2, 2014). In July, according to data released on August 28, 2014, money supply growth was about 2% versus the prior year, whereas bank lending to the private sector fell by 3% [Figure 3]. The ECB’s new bank lending program (referred to by the acronym TLTRO) experienced much weaker than expected demand last week, providing further evidence that the banking system in Europe is not functioning properly and growth is constrained.

- Earnings expectations may be too high. Based on recent weak economic data out of the Eurozone and Europe’s recent track record of missing earnings estimates (Q2 2014 earnings came in 6% shy of June 30, 2014 estimates), earnings may disappoint investors. The Thomson-tracked consensus is calling for double-digit earnings growth in both the third and fourth quarter of 2014 and in the first half of 2015, despite marginal revenue growth expectations and expected GDP growth around 1% (based on the Bloomberg-tracked consensus of economists). The sluggish economic environment increases our fear that the high hurdle for earnings growth will not be met and may disappoint investors.

- Geopolitical risks are high. Geopolitical risks are present for all markets globally, but they are particularly acute for Europe. Because of Europe’s energy dependence on Russia and Ukraine and its closer trading ties to Russia, the Russia-Ukraine conflict in particular impacts Europe more than the United States and other regions. Europe’s close proximity to the Middle East also contributes to heightened geopolitical risk, given the turmoil in Iraq and Syria.

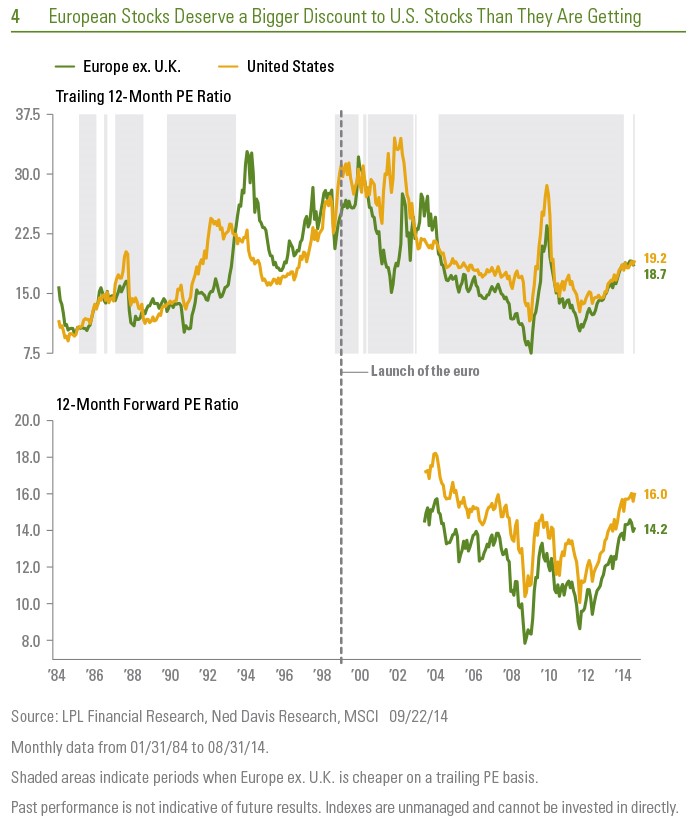

- We believe European stocks should trade more cheaply relative to U.S. stocks. A bigger valuation discount for Europe versus the United States is warranted given the divergence in economic growth and momentum, and greater structural constraints on Europe’s growth. Figure 4 (bottom panel) shows European stocks are trading at about a 10% discount to U.S. stocks, measured by the forward 12-month price-to-earnings ratio (PE) for the MSCI Europe Index (excluding the United Kingdom) versus the MSCI U.S. Index (similar to the S&P 500). On a trailing 12-month PE basis, the PE discount is even smaller (19.2 versus 18.7, or less than 3%), perhaps providing a stronger argument for the U.S. market being more attractively valued. On a relative basis versus the United States, Europe’s PEs (trailing and forward) are 4 – 5% above their averages during the current bull market.

-

European market’s technicals are inferior to the United States. From a technical perspective, European equities look less appealing to us than the United States. The two accompanying price charts [Figure 5] tell different stories from a trend perspective. The MSCI Europe Index in absolute terms (top panel) is exhibiting a bullish weekly trend, identified by the positive slope of the 40-week simple moving average (SMA) over the past two years (the orange line in the chart). From an absolute perspective, European equities continue to make higher highs and higher lows, which may make them attractive as a possible buy-and-hold type investment based on technical analysis.

However, the bottom panel of Figure 5, which shows the MSCI Europe Index relative to the U.S. stock market (based on the S&P 500), tells a different story. It is exhibiting a bearish weekly trend, identified by the negative slope of the 40-week SMA over the past two years (orange line). A negative sloping weekly trend means that the MSCI Europe Index continues to underperform the S&P 500 Index, suggesting a more positive technical picture for U.S. equities. Although this trend may reverse, we do not believe fundamentals and valuations are supportive enough to consider a positive recommendation before we get technical confirmation of a turn in momentum.

Conclusion

Part one of this two-part series told us to stay close to home and the sequel tells us to do the same. We continue to recommend that investors “fight the ECB.” We do not believe the additional stimulus — even at its boldest — is enough for us to recommend European equities over U.S. equities. We do not find the fundamentals particularly compelling at this point, given the lackluster economic and profit growth outlook for the Eurozone and the risk of deflation. We do not believe European stock valuations are attractive relative to those in the United Sates. And the technical picture for the United States looks better to us than that of Europe.

Bottom line, we continue to favor the United States over Europe, but we will continue to watch for opportunities to go overseas later this year and in 2015. For investors looking for overseas equity market exposure, we suggest looking at the emerging markets, where we see a better combination of fundamentals, valuations, and technicals.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

Forward price-to-earnings is a measure of the price-to-earnings ratio (PE) using forecasted earnings for the PE calculation. PE is a valuation ratio of a company’s current share price compared to its per-share earnings.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The MSCI Europe Index captures large and mid cap representation across 15 developed markets (DM) countries in Europe.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking # 1-310165 (Exp. 09/15)