How Plan Sponsors Can Prepare for the Coming Changes to Mortality Tables

The name may sound like something from Star Wars, but RP-2014 is actually the draft mortality tables released by the Society of Actuaries (SOA) earlier this year. These revised tables highlight longer life expectancies and faster increases in mortality improvements, affirming the well-established belief that individuals are living longer. The draft is currently under review by various stakeholders with the expectation that RP-2014 will be formalized this year.

The past 15 years have been a roller-coaster ride for the average pension plan’s funded status, which has been rising and dipping with financial markets and interest rate movements (Exhibit 1). The strong equity market returns of 2013 brought plan sponsors relief as they saw the average funded status climb, though some of last year’s gains may have been lost to the recent decline in interest rates. The recognition of the mortality improvements in RP-2014 will result in another dip in funded status.

Exhibit 1: Average S&P 500 funded status

Source: Columbia Management Investment Advisers, LLC

What does RP-2014 mean for your pension plan?

Over the last several years, increases in participants’ longevity have been recognized annually as pension plans experienced actuarial losses due to mortality improvements. RP-2014 will require plan sponsors to immediately recognize the improvements in participants’ mortality—resulting in a reduction in the funded status of the pension plan.

- The reduction in funded status will:

- Lower reporting funded status for both funding and accounting purposes

- Increase PBGC risk-based premiums

- Increase contribution requirements

- Increase the value of lump sum payments

The degree to which the mortality tables will affect funded status depends on the pension plan’s demographics. Factors such as female vs. male concentration, blue collar vs. white collar employees, and age distribution of plan participants will determine how a plan is affected by the adoption of a new mortality table. Estimates of the increase in liabilities usually range from about 3% to 10%, with a similar reduction in funded status. Cash balance plans will be less affected than traditional pension plans because the cash balance lump sum is not dependent on a mortality assumption.

Timing of RP-2014 implementation

If RP-2014 is formalized in 2014, many accounting firms will likely require that plan sponsors recognize the effect of the table when their next final statements are issued, December 31, 2014 for many companies. Sponsors who don’t immediately recognize the full effect of the mortality revisions will have to demonstrate why another mortality table provides a better estimate of the plan’s liability. The reduction in funded status due to the revised mortality tables will affect the company’s balance sheet through a decrease in shareholder’s equity (net of an income tax adjustment). In addition, the expense in the following years will be larger due to an increase in the interest charge on the larger Projected Benefit Obligation (PBO) and a potential increase in the amortization charge.

Consider a company with a PBO of $500 million which increases by 8% ($40 million) due to the new mortality table. The company’s shareholder’s equity would decrease by $24 million (assuming a 40% tax rate). The pension expense interest charge the following year, using a 4% discount rate would increase by $1.6 million. The increased amortization amount, if any, would depend on the company’s amortization approach for actuarial losses.

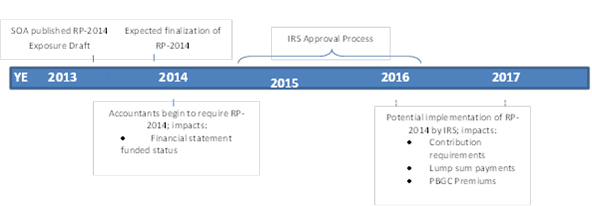

The recognition of the new mortality table will be longer for IRS purposes. The IRS has already published the mortality tables to be used for funding and lump sum payment purposes for 2014 and 2015. Any significant changes in IRS requirements, such as a new mortality table, are subject to a formal IRS approval process. That process can take as long as 18 months. If RP-2014 is formalized by the SOA in the next few months the IRS approval process might be completed in time for the adoption for 2016; however, it is likely that RP-2014 will not be required for IRS purposes until 2017. That would mean that contribution requirements, lump sum payments and PBGC payments would not be affected until then (Exhibit 2).

Exhibit 2: Timeline for IRS recognition of RP-2014

Source: Columbia Management Investment Advisers, LLC

Impact of longevity in a de-risking framework

Most plan sponsors closely monitor the funded status of their pension plans. Many have adopted investment strategies such as Liability Driven Investing (LDI) to decrease the volatility of the plan’s funded status, pension expense and contributions. How might plan sponsors respond to the change in mortality tables? Some may feel that the recognition of the mortality improvements of RP-2014 will eliminate potential future actuarial losses – making the increased IRS required contributions adequate to satisfy their funding goals. Others may decide to voluntarily increase their contributions in excess of the IRS required contributions to compensate for the reduction in funded status. Still others may review their LDI glide path strategy to adjust their asset allocation until the funded status improves.

Plan sponsors should identify which of the above actions meets its pension funding strategy and work closely with their advisors, investment managers and actuaries to implement the approach which best meets their objectives. Columbia Management’s Liability Driven Solutions team offers a fully customized LDI solution that adapts to a plan sponsor’s changes in liability assumptions, such as with RP-2014.

Disclosure

The views expressed are as of 9/22/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

1017945