While Fed watchers continue to debate the timing of the first post-2008 hike in the Federal Funds rate (first or second quarter of 2015), we believe the first move toward tighter policy occurred in January when the Fed first reduced the rate of its monthly bond purchases by $10 billion to $75 billion. Our opinion isn’t based on any intricate knowledge of Fed liquidity flows, but simply on the subsequent action of two key stock market segments:

- Small Caps, which have historically shown much greater sensitivity to Fed rate hikes than Large Caps, rallied into a March 4th bull market high before subsequently underperforming the S&P 500 by 10% in the following six months. Similar phases of Small Cap underperformance were observed in the immediate aftermath of rate hikes in 1983, 1988 and 1994 (although not in 2004).

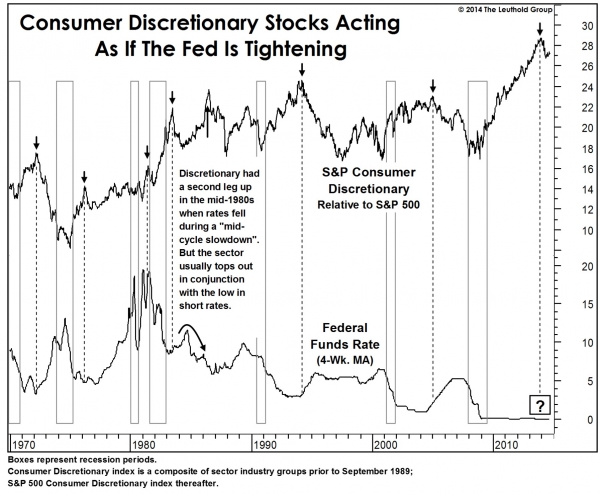

- The S&P 500 Consumer Discretionary sector peaked on a relative performance basis on January 2nd—the first trading day of the first month of the tapering program. We’ve repeatedly noted this sector has historically shown greater vulnerability to Fed rate hikes than any other sector (including the Financials, which are more sensitive to changes in the yield curve slope). Consumer Discretionary stocks looked broadly overvalued long before that initial tapering move, and the fact that the sector’s relative strength high occurred in the same month of the first taper seems more than a coincidence.

Among the current wide range of projections, we think the forecasts of Fed tightening in January 2015 are the most accurate… they’re late by only one year.

© Leuthold Weeden Capital Management