Voya Fixed Income Perspectives September 2014

Bond Market Outlook

Global Interest Rates: We are negative on duration risk both strategically and tactically.

Global Currencies: We remain overweight the U.S. dollar versus other developed market currencies and continue to play EM currencies tactically.

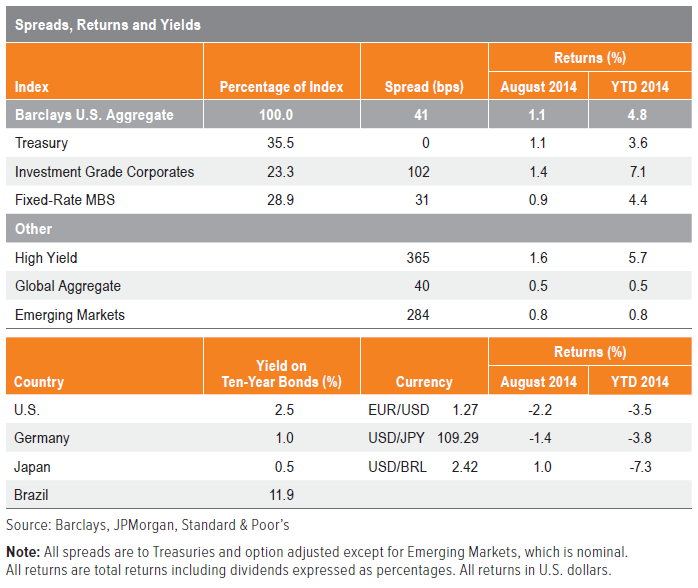

Corporates: Spreads are fairly valued, and there is potential for tightening in the coming months; excess returns, however, will be driven primarily by carry or yield.

High Yield: Spreads have widened significantly and are now attractive given still-solid fundamentals and low default risk.

Mortgages: We are neutral on agencies given an uncertain interest rate outlook; we continue to favor non-agency mortgages and CMBS.

Emerging Markets: We continue to favor corporates over sovereigns, with a bias for hard currency over local currency

Macro Overview

- Change is in the air, and it’s evident beyond the riot of color overwhelming our natural landscape. Market dynamics, too, are shifting, with the yield on the U.S. two-year Treasury inching higher and the U.S. dollar appreciating. Both not only suggest markets are pricing in a stronger U.S. economy, they are also potential harbingers that the end of zero interest rate policy is near.

- Despite U.S. economic data that continues to surprise to the upside — including much better than expected second quarter GDP growth, housing starts at multi-year highs and payroll trends moving in the right direction — the Fed has reiterated that it will be a “considerable time” until rate hikes begin. While the U.S. economy is exhibiting the type of cyclical strength that should bias short term interest rates higher and the dollar stronger, its long-term prospects have the central bank less enthused. Wage inflation, for example, remains extremely low, consistent with below-target core PCE, the Fed’s favored inflation metric.

- Moreover, weak global growth means inflationary pressures outside U.S. borders remain benign. In Europe, for instance, the ECB’s plan to expand its balance sheet through the purchase of asset-backed securities is encouraging, though the circumstances forcing its introduction — including near-zero inflation — certainly are not. And while the outcome of the Scottish referendum succeeded in keeping the U.K. intact, the potential for political upheaval and divergence persists, as does the uncertainty that comes with having Russia as a major trading partner. These and other factors will likely continue to test the scope of Draghi’s “whatever it takes” policy.

- Dollar strength will also be reflected in lower commodity prices, particularly given weaker data out of China. While a dividend for the U.S. consumer, this dynamic will pressure energy and food costs lower, thereby keeping inflationary pressures contained and buying more time for the Fed.

- Just as autumn turns to winter slowly, changes in U.S. monetary policy will be gradual. We retain our preference for U.S.-centric investments like high yield and CMBS. The potential for episodic volatility persists, however, underscoring the importance of adding protection against tail risks now.

Sector Overviews

Global Interest Rates

- With U.S. data continuing to improve, each FOMC communication has the potential to catalyze higher volatility and higher yield risks, which have been implicit in rich valuations for some time. Still, the net level of global accommodation remains positive; the ECB and BOJ are locked into accommodative policy for the foreseeable future given weak economic fundamentals, and global inflation pressures are very weak. The liquidity influx from China has abated somewhat but remains a net positive.

- Globally, continued yield hunger and central bank activity will keep G10 government rates at already-rich levels. However, any slowdown in foreign central bank buying could be a potential catalyst for a correction, particularly as the Fed becomes a net remover of accommodation. As we prepare for Fed rate hikes and an upward cycle in global interest rates, we are negative on global interest rate risk from both a strategic and tactical perspective.

Global Currencies

- Positive U.S. economic momentum and the potential for higher U.S. yields are driving U.S. dollar strength versus other major currencies, a dynamic being furthered by global economic weakness and the prolonged expectation of central bank accommodation outside U.S. borders. As such, we remain overweight the dollar versus the euro and yen in developed markets, and continue to play EM currencies on a tactical basis as the downturn in commodity prices continues.

Investment Grade Corporates

- The outlook for the U.S. economy is positive for risk appetite and supportive of corporate spreads, but interest rate volatility and a large new-issue calendar could inspire technical pressures in the coming months. Still, the fundamental backdrop remains good, with corporate revenue, EBITDA and capital expenditures growth improving sequentially during the second quarter. International weakness is a concern, as is the tick up in leverage, but we continue to view spreads as fairly valued and see the potential for spread tightening in the near term. Carry or yield, however, will be the primary driver of excess returns.

High Yield Corporates

- The combination of equity markets at all-time highs and high yield spreads at year-to-date wides was enough to stem outflows from the high yield market during the month. Higher quality outperformed lower quality in the recovery, leaving BB returns beating CCC returns for the year. The magnitude of the flow reversal was not enough to fully offsetthe correction, and recent volatility has spreads again approaching their 2014 wides. With corporate fundamentals in good shape and the risk of defaults low, spreads are attractive at these cheaper levels. We expect spreads to persist at current or lower levels for some time.

Mortgages

- The supply and demand dynamic remains favorable for mortgages in the near term, with gross issuance remaining extremely low on a year-over year basis. And despite improving domestic data, global conditions continue to dampen the probability of significantly higher rates. From a valuation perspective, however, lower coupons provide limited carry, at-the-money coupons hold significant extension risk, and higher coupon pools are at high dollar prices and tight spread levels. The potential for interest rate volatility and spotty demand outside the Fed are significant risks that could pressure mortgages across the coupon stack in the coming months. As a result, we are neutral on agency mortgages.

- We continue to favor non-agency mortgages and CMBS. The housing recovery still has plenty of runway, and the carry/spread compression potential offered by both asset classes is attractive as compared to other spread sectors. Commercial real estate lending standards have deteriorated, but from very stringent levels. The biggest risk in the near term is the new-issue supply pipeline, as demand has the potential to be lackluster in response to increased volatility in other risk markets. There will be a premium on security selection going forward.

Emerging Markets

- Growth and inflation across emerging markets is divergent, but we see higher probability of downside surprises here given weak demand from the G3 and weak global trade in general. Though uncertainty around the Fed’s tightening path is a cause for concern and weaker commodity prices are a risk to the asset class overall, global liquidity conditions are generally supportive of emerging markets. As such, flows are not leaving the asset class but are being circulated within it. For example, tensions between Russia and Ukraine are redirecting flows away from Central Europe and toward Latin America and Asia. We continue to favor corporates over sovereigns, with a bias for hard currency issues over local currency ones.

This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance does not guarantee future results.

©2014 VoyaInvestments Distributor, LLC • 230 Park Ave, New York, NY 10169

CMMC-FIMONTHLY 093014 • CN0916-22479-1016 • 10587 • 163124

RETIREMENT | INVESTMENTS | INSURANCE