Bullish on Gold Priced in Euro Gold Priced in Dollars, Not So Much

Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

In this week’s discussion we revisit our earlier analysis looking at the relationship between the gold price and real interest rates. Over the last three months the gold price in dollar terms has fallen 9% moving briefly below $1,200 and naturally raising concerns amongst investors that this pull-back may extend as the dollar continues to strengthen against a broad basket of currencies. By way of contrast the gold price in euro terms has fallen 1.5% and we examine some of the key factors driving the relative move in the two gold prices to try and develop a better understanding of the potential for prices to either move higher or lower over the next three months.

In the chart above we present a five year look back on the price of gold in dollars overlaid with our measure of the value of the dollar, the euro/US dollar exchange rate and the yield on the US 10 year inflation-linked bond, a market measure of the 10 year real interest rate. Note that the real yield axis has been inverted with values reading from high to low moving upwards on the axis. This is to make the direction of the data series consistent with the gold price on the chart with lower real yields being associated with a high gold price.

When we last examined this relationship at the beginning of August the real yield was at 0.14% but has since moved back higher to its current level, 0.478%. The move higher in real yield was also matched by a rise in the value of the dollar on currency markets, as measured by the euro/US dollar FX rate. And both of these variables have exerted a powerful downward effect on the price of gold in dollars which has fallen from 1310 to 1207 (-7.8%).

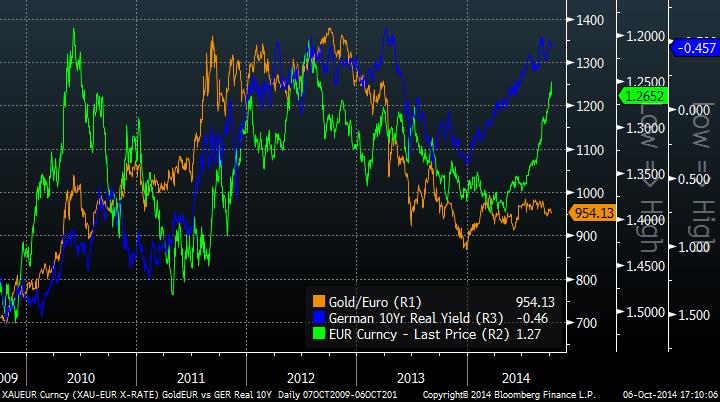

In the chart below we chart the same data over the same time horizon but instead focus on the gold price in euro. We note that both the real yield axis and the euro/US dollar axis (a measure of euro strength) have been inverted with values reading from high to low moving upwards on the axis. This is to make the direction of the two data series consistent with moves in the gold price with lower real yields and a lower euro/US dollar FX rate (weaker euro) being associated with a higher gold price in euro.

In contrast to the gold price in dollars the gold price in euro has largely been stable since August but this has been in an environment of a sharply lower euro/US dollar FX rate (-4%) indicating a much weaker euro and sharply lower euro real yields falling from -0.32% when we last looked at the chart to the current -0.457%. Both of these variables would be expected to be positive for the gold price in euro terms.

Given these large moves in terms of euro weakness and increasingly negative real yields we find the stability of the gold price in euro surprising and would expect to see some amount of “catch-up” in terms of higher prices if the previous historical relationships were to reestablish themselves. There is of course also the possibility of a sharply stronger euro going forward accompanied with higher real yields but we find this outcome to be less probable given the growing divergence in the trajectory of monetary policy between the Federal Reserve and the European Central Bank and also the vicious cycle of disinflation and low GDP growth in which the Euro area appears to be trapped.

In terms of the gold price in dollars, we do not anticipate any sharp moves in US real yields in the immediate feature as the economy recovers albeit at a slow pace. Based on the relationship we observe in the chart, should the dollar stabilize at current levels we would expect the gold price in dollars to also stabilize at current levels but it will certainly be vulnerable to further weakness should the strength in the dollar seen over the last few months extend.