Yesterday’s S&P 500 close of 1928 marked a 4% correction since the index peaked at 2011 on September 18, 2014.

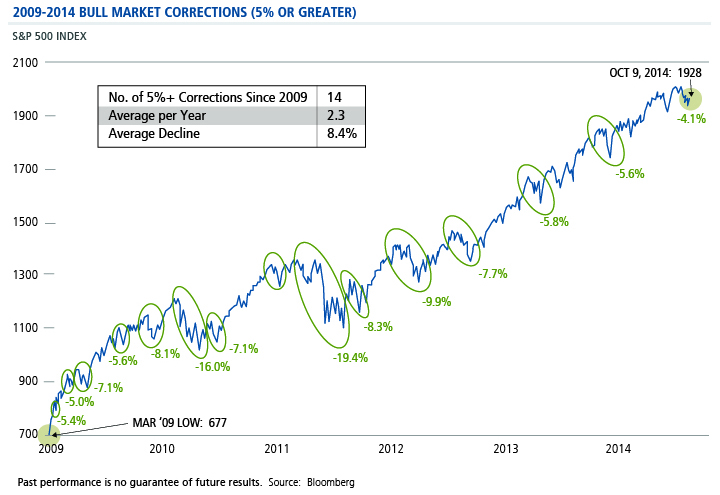

Let’s keep this in perspective: If the market falls another 1% to 1910, it would mark the fifteenth correction of 5% or more since this bull market began in March of 2009. On average, there have been two 5%+ corrections per year since the bull market began in 2009. The most recent was the 5.6% correction in January, which also resulted from concerns about slowing global economic growth.

Past performance is no guarantee of future results. Source: Bloomberg.

This correction feels no different than others: We’ve had a spike in volatility to around 19 off of July’s record low of 11 (as measured by the VIX) as the market has gyrated from worrying about too much growth leading to an early Fed rate hike to worrying about too little growth as European Central Bank President Mario Draghi and German finance officials disagree about the efficacy of quantitative easing.

In the end, we believe this correction and spike in volatility will end when investors conclude the upward trajectory of corporate earnings will continue. With expected S&P 500 2015 earnings growth of 6%, the S&P 500 could earn $124 in 2015, which implies a 15.5x P/E multiple, or a 6.4% earnings yield. Relative to today’s 2.3% 10-year Treasury yield, equities remain in the cheapest quartile of valuation relative to bonds over the past 60 years. Furthermore, corporate buybacks and M&A—which remain at their highest levels since 2007—put a floor on the equity market. If stocks fall further, we believe corporations awash in cash and able to borrow at some of the lowest rates in decades will continue to buy either their own or someone else’s stock. For most companies, both actions are highly accretive and will likely continue as long as borrowing costs remain low and/or earnings yields stay high.

We believe the 3Q earnings season, which moves into full swing next week, combined with greater unity by European officials on how to jump start economic growth, and additional soothing comments from our own Fed about keeping short-term rates low for a considerable time, should allow this correction to dissipate without incident, propelling the five-and-a-half year bull market to new highs.

© Calamos Investments