Oracles Present State Looks Great But Challenges Lie in Wait

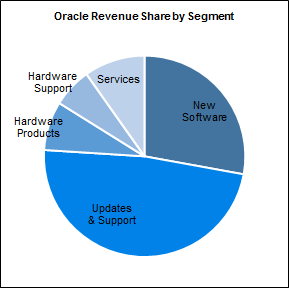

You may think of Oracle (ORCL) as a company that sells software. In fact, at its core, it is a company that sells software updates.

Oracle has four other segments-including "New Software"-but all of them are simply shovels used to feed business into the mighty furnace of Oracle's Updates & Supports segment.

The Updates & Support business-comprising nearly half of Oracle's revenue stream-is phenomenally profitable, with operating margins of close to 90%.

Because Oracle's traditional enterprise database software is such an integral part of highly-critical accounting and other business systems, and because millions of dollars is spent customizing Oracle's software to a given client's needs, once a client has committed to using an Oracle product, they are tied into an inexorable upgrade cycle.

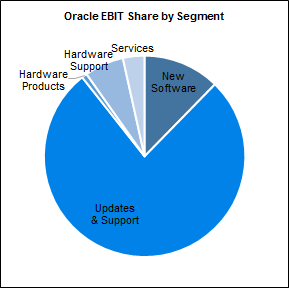

Every time the cycle turns, Oracle generates huge profits. You can see this at a single glance at this chart, showing per-segment earnings before interest and taxes (EBIT) contribution.

Operational Leverage

You may notice that the "Hardware Products" piece of the EBIT pie is almost diminishingly small. Pundits attacked Ellison for structuring the 2010 acquisition of high-performance hardware firm, Sun Microsystems for this very reason. "What good could come," they asked "if high-margin Oracle buys a low margin hardware business?"

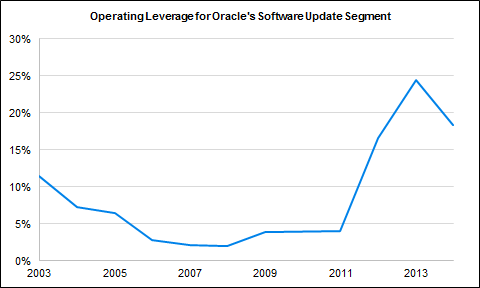

However, as this author pointed out in the first YCharts Focus Report on Oracle, we do not think it is mere chance that ever since Oracle bought Sun, Oracle's vitally important Updates & Supports business experienced an enormous uptick in operating leverage.[1]

Analyzing the most recent financial statements of Oracle in our most recent report, it is clear that the operating leverage boost we identified in our last report has continued, though to a somewhat less-pronounced degree.

This crooked smile ending with a value of 18% means in practice that while Software Updates' segment revenues increased by (a still robust) 6% in fiscal year 2014, the segment's profits grew even faster—at a rate of 7%.

The fact that operational leverage continues to be strong in comparison with prior years is, in this author's opinion, a positive sign that speaks to the continued success of the Sun acquisition for Oracle and its shareholders.

Future Challenges

Oracle is doing what it does best-generating huge amounts of profits using its dual pacemaker/disposable razor strategy.

Hardware sales look to have stabilized and, as explained above, Oracle's most important segment is converting revenues to profits increasingly efficiently. If Oracle were a machine, it would be humming along at peak performance.

However, this does not mean that an investment in Oracle is a fire-and-forget affair. In fact, the company is reaching a critical transition point, underscored by founder Larry Ellison turning the CEO reins over to Hurd and Catz.

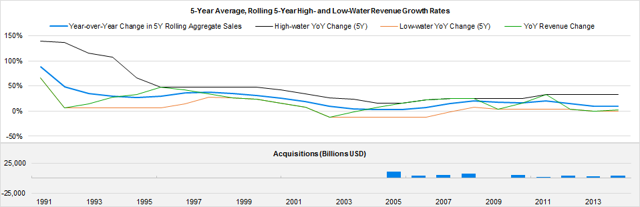

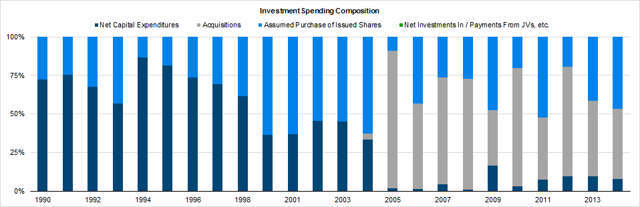

As is obvious in the chart below, Oracle began an acquisition binge about 10 years ago, when its organic growth had begun to slow.

Over the past several years, it has spent an average of about half its Owners' Cash Profits (which we define as Cash Flow from Operations, less an estimate of the money required to maintain the firm as a going concern[2]) on investments designed to boost future profit growth.

While profits continue to grow, they are growing more slowly, and we think this means Oracle's investments are giving it less and less of a boost. When you're small, all you need is good ideas. When you're big, you need good big ideas, and those are rarer.

It is at this stage in a company's existence that it can either make a bold, transformative move to redefine itself [e.g., Apple (AAPL) turning from a manufacturer of niche computer systems into a designer and marketer of consumer products] or it must take its foot off the investment gas pedal and start to return more profits to shareholders.

The risk with the first course is that the bold, transformative move will fail [e.g., Ron Johnson's JC Penney (JCP)], permanently damaging the company. The risk with the second course is that it takes too long for management to realize that its investments are no longer creating value. In this case, the stock runs the risk of becoming "dead money" until management figures out the mistake and corrects it.

Oracle: Dead Money Candidate?

Of the two risks, this author is relatively more worried about the latter. Oracle's capital expenditure requirements are very low. With its present Owners' Cash Profit margin level in the mid-30% range, its present average investment spending implies a Free Cash Flow to Owners level in the sub-20% range (we define Free Cash Flow to Owners as Owners' Cash Profits less money spent on investments designed to boost future profit growth[3]).

If Oracle could gracefully cut its investment level to somewhere around one-fifth of its owners cash profits (i.e., cutting its present rate of expenditures by more than half), it could materially increase the amount of FCFO it is generating, even if revenues were slow growing and profit margins stabilized.

But if it were going to cut something, what would it cut?

Its acquisition strategy ties into its critical Software Updates business-acquired technology is incorporated into future rounds of updates to Oracle's products. So cutting back on these acquisitions would potentially hurt Oracle's most important business line.

However, we estimate that roughly 40% of its "investment" dollars are going to fund anti-dilutionary stock buybacks (i.e., back-door compensation to executives and other employees). Cutting into these expenditures will not be easy either.

This issue will most likely affect medium-term growth rates since the impact of today's corporate acquisitions are greatest a few years after they are made and integrated. Changing assumptions about these growth rates can have a large effect on valuations.

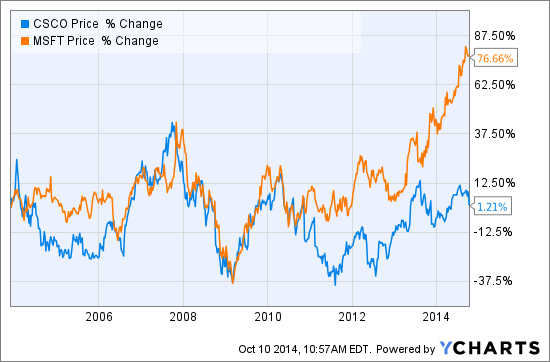

In our valuation analysis, a feasible worst-case scenario generates a valuation in the upper-$20 range. This scenario--in which Oracle continues to make increasingly hard-to-integrate acquisitions that make increasingly diminishing improvements to the company's profit growth without appreciably boosting revenue growth--is not dissimilar to the case of networking giant Cisco Systems (CSCO).

Cisco is the poster child of Old Tech Dead Money--a dubious title it won from Microsoft (MSFT) since the end of 2010.

Could the same fate befall Oracle? Without the new CEOs Catz and Hurd making hard decisions about future investments and growth strat

[1] Operating leverage means that as additional dollars of revenue flow in, the firm becomes increasingly efficient at converting those revenues into profits.

[2] For a full explanation of Owners’ Cash Profits (OCP), please see our Valuation Methodology webinar replay.

[3] For a full explanation of Free Cash Flow to Owners, again, please see our Valuation Methodology webinar replay.