Optimizing a Portfolio Allocation to Gold

Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

Gold continues to be an attractive asset class that many investors wish to hold in their portfolios primarily for its diversification benefits and defensive characteristics during periods of high risk aversion in global markets. And notably many investors gain their gold exposure via exchange traded products given the ease of access, liquidity and the transparency they offer, particularly to retail investors who historically faced numerous barriers to holding gold in their portfolios.

Many investors would firmly place gold and precious metals in general within the ‘commodity’ risk bucket but in doing so this has sometimes meant that holders of gold have failed to take into account one of the biggest factors impacting its performance into their asset allocation decision process, namely currency exposure. In short, when an investor buys gold in whatever form they choose whether it be ETF, coins or bars, they are also explicitly expressing a currency view.

Gold is primarily traded in US dollars and indeed the most popular gold-linked exchange traded funds offer investors the ability to hold gold in dollar denominated terms. But a critical component of assessing the expected performance of a gold investment in a portfolio is understanding that the gold investor is expressing the view that they expect gold to increase in value relative to the financing currency i.e. the currency used to make the gold purchase, which in most cases is the dollar. So while an investor may have a view on the fundamentals of the gold market, by holding gold, in addition to being exposed to risk factors that drive its fundamental value the investor is also exposed to the risk factors that drive the value of the financing currency on foreign exchange markets.

Choice of Financing Currency Matters

We can illustrate easily why this is the case by using the example of an investor that buys gold financed in European euro i.e. gold priced in euro terms. When an investor buys gold financed in euro they are expressing the view that they expect the price of gold to increase in terms of the number of euro for which it can be exchanged at a future date. If their view is correct they will be able to sell the gold and receive more euro for the amount of gold they hold, than was used to make the original purchase. An investor that buys gold in euro is therefore expressing a directional view on both gold and the euro – they are expressing the view that as the euro weakens on currency markets they would expect, all things being equal, to receive more euro for a given amount of gold. Similarly as the euro strengthens they would expect to receive fewer euro for a given amount of gold. In market speak the investor is said to be long gold, short euro. And it is this short exposure to the financing currency (in this instance the euro) in addition to long exposure to the fundamentals of the gold market that drive the performance of an investment in gold.

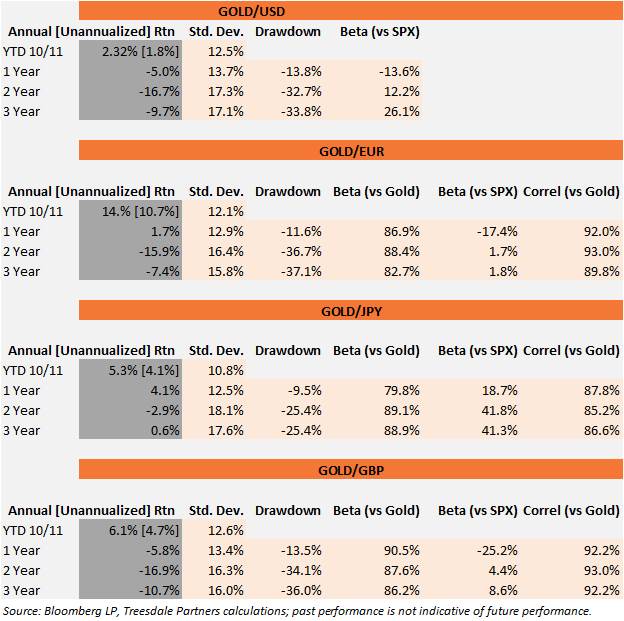

So having established that the financing currency is a key component of gold performance, it follows then that a holding of gold in euro terms will likely result in a quite different risk exposure for the investor than say a holding of gold in dollars. In other words choice of financing currency matters. And we can show this effect by looking at the relative performance of four different gold investments, financed in dollars, euro, yen and pounds respectively.

The first striking feature about the performance of these gold prices is the wide variation in performance depending on the financing currency used to make the gold purchase. Gold financed with euro year-to-date has returned 10.7% while at the other end of the performance spectrum gold priced in dollars has returned 1.8% and with a higher standard deviation. The next best performer year-to-date has been gold financed in pounds returning 4.7%. Interestingly gold priced in yen has experienced the best one, two and three year performance of all the gold prices returning 0.6% annualized (essentially unchanged) compared to the -9.7% annualized performance of gold priced in dollars.

The single biggest factor driving the divergence in performance has been the relative weaknesses of the respective financing currencies on the currency markets. Year to date the euro has weakened by 8% versus the dollar helping to propel the gold price in euro terms higher while over the last three years the yen has weakened by 30% versus the dollar leading to the three year outperformance of gold in yen terms versus gold prices denominated in other currencies including the dollar.

Choice of Financing Currency also Impacts Gold’s Defensive Qualities

In addition to impacting performance, the choice of financing currency for a gold investment also has significant bearing on its defensive qualities. In particular it can be shown that historically the price of gold in dollars has tended to underperform the price of gold in non-dollar currencies during periods of heightened market stress. The crucial differentiator here has been the unique role of the dollar in global markets as the reserve currency of choice for a number of reasons, most notably the depth of dollar denominated asset markets and the perceived ‘safe-haven’ status of the dollar.

During periods of heightened stress investors have often sought to swap assets into dollars as a way to seek protection from rising uncertainty in other markets. But ironically it is this defensive surge in demand for dollars that has often worked to reduce the effectiveness of holding gold as a defensive asset. As the dollar strengthens on currency markets this has the direct effect of pushing down the value of gold priced in dollars - put differently the number of dollars that an investor would expect to receive from selling an ounce of gold, all things being equal, would be expected to fall. For this reason, an investor seeking to hold gold for its diversification and defensive qualities can potentially enhance these desirable characteristics by having an allocation to gold in non-dollar denominated currencies in addition to their dollar denominated allocation.

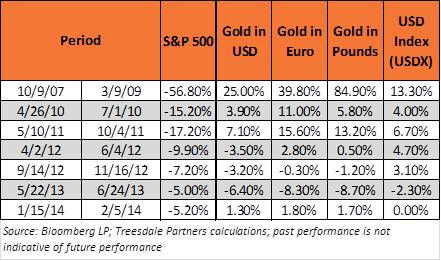

Historically Gold Financed in Non-Dollar Currencies Outperforms During Stress Periods

To show this effect the analysis below looks at the performance of gold priced in dollars, euro and pounds during periods in which there was a sharp rise in risk aversion. For the purposes of the discussion a “sharp rise in risk aversion” is defined as any period from and including the 2007 credit crisis in which there was a peak-to-trough fall of 5% or more in the S&P 500 index. The results are presented in the table below.

There are two main patterns to observe. Firstly, in every period other than the May-June 2013 period gold priced in euro and gold priced in pounds outperformed gold priced in dollars. This was driven by the fact that during these periods the US dollar showed broad based strength as investors concerned about the heightened level of uncertainty swapped assets into dollars. And as the dollar strengthened from the rising demand, as might be expected, the price of gold in dollars was adversely affected. In contrast gold priced in euro and gold priced in pounds by not being exposed to the dollar were less impacted by dollar strength during these stress periods. In the last column in the table a broad measure of the value of the dollar is shown using the Intercontinental Exchange Trade Weighted Dollar Index (USDX) as a proxy. In every period other than May-June 2013 the dollar as measured by USDX strengthened which contributed to the underperformance of gold priced in dollars relative to non-dollar financed gold. But in the period in which the dollar was weak we see that the gold price in dollars outperformed the other currencies.