This latest stock market pullback has provided an unwelcome reminder that stocks do not always go up in a straight line. Even within powerful bull markets such as this one, pullbacks of 5–10% have been quite common and do not mean the bull market is nearing an end. In this week’s commentary, we attempt to put the pullback into perspective. We look beyond this latest bout of volatility and share our thoughts on the current bull market, compare it with prior bull markets at this stage, and discuss why we do not think it’s coming to an end.

Pullbacks Don’t Mean the End of the Bull Market

Pullbacks such as this one, which has reached 5%, have been normal. Sometimes stocks get ahead of themselves. When they do, investor concerns can be magnified and profit taking might take stocks down more than might be justified by the fundamental news. We see this latest pullback as normal within the context of an ongoing and powerful bull market and do not see its causes (European and Chinese growth concerns, the rise of Islamic State militants, Ebola, the Russia-Ukraine conflict, etc.) as justifying something much bigger.

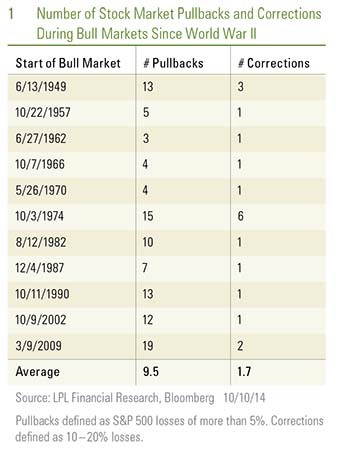

The S&P 500 has now experienced 19 pullbacks during this 5.5-year-old bull market, during which the index has risen by 182% (cumulative return of 217% including dividends). The 1990s bull market included 13 pullbacks; there were 12 during the 2002–2007 bull market. At an average of three to four pullbacks per year, we are in-line with history [Figure 1]. We understand the nervousness out there, but what we have just experienced looks pretty normal at this point.

When volatility has been so low for so long, normal volatility does not feel normal. Investors have become unaccustomed to what we would characterize as normal volatility. While most of the 5% drop came in a short period of time last week (October 6– 10), the level of volatility experienced last week is not at all uncommon within an ongoing economic expansion and bull market. Volatility tends to pick up as the business cycle passes its midpoint, which we believe it has. Reaching this stage just took longer than many had expected during the current cycle.

Also, keep in mind that the 335 drop in the Dow Jones Industrials that we experienced on Thursday, October 9, 2014, is not as dramatic as it once was. That loss was less than 2%, with the Dow near 17,000 when it occurred, compared with 3–4% losses associated with that number of points on the Dow earlier in the recovery.

These pullbacks do not mean the end of the bull market is near, nor does the fact that we have not had a 10% or more correction since 2011. In fact, most bull markets since World War II included only one correction of 10% or more, and the current bull has already had two (2010 and 2011). We do not believe the current economic and financial market backdrop has sufficiently deteriorated for the pullback to turn into a bear market, as we discuss below.

Why This Pullback Is Unlikely to Get Much Worse

So why do we think this pullback is unlikely to turn into a bear market? There are a number of reasons:

§ The economic backdrop in the United States remains healthy. Gross domestic product (GDP) is growing at above its long-term average, providing support for continued earnings growth; the U.S. labor market has created 2 million jobs over the past year; and the drop in oil prices may support stronger consumer spending.

§ Our favorite leading indicators, including the Conference Board’s Leading Economic Index (LEI), the Institute for Supply Management (ISM) Index, and the yield curve, suggest that the bull market may likely continue into 2015 and beyond, with a recession unlikely on the immediate horizon.

§ The European Central Bank (ECB) is likely to add a dose of monetary stimulus to spark growth in Europe, the source of much of the global growth fears that have driven recent stock market weakness. China stands ready to invigorate its economy as well.

§ Interest rates, and therefore borrowing costs for corporations, remain low. The Federal Reserve (Fed) is in no hurry to raise interest rates.

§ Valuations have become more attractive. Price-to-earnings ratios (PE) have not reached levels that suggest the end of the bull market is forthcoming, based on history. We view PEs, which have fallen about 0.5 points from their recent peak, as reasonable given growing earnings and low interest rates.

§ The S&P 500 is marginally above its 200-day moving average at 1905. Historically, this level has proven to be strong support. Although the index may dip slightly below this level in the near term, we expect the range around that level (1900 – 1910) to provide strong support for the index again and would not expect it to stay below that range for very long.

Bull Markets Don’t Die of Old Age

The current bull market is one of the most powerful ever at this stage, just over 5.5 years in [Figure 2]. Since March 9, 2009, when the current bull market began, the S&P 500 has risen 182% (total cumulative return of 217%), topping all other bull markets since World War II at this stage. The 1949 and 1982 bull markets were close, with gains of 170% and 163% (respectively) at this stage, but were not quite as strong.

So does that mean that this bull market is too old and should end? We don’t think so. Bull markets die of excesses, not old age, and we do not see the excesses that characterize an impending bear market. The labor markets are not strong enough yet to generate significant upward pressure on wages to drive inflation. U.S. factories have excess capacity. As a result, the Fed is unlikely to start hiking interest rates until the middle of 2015, and rate hikes are likely to be gradual. It will likely take numerous hikes to slow the U.S. economy enough to tip it into recession (and invert the yield curve), which is unlikely to come until at least 2016. We do not see stock valuations or broad investor sentiment as excessive. We expect this bull market to complete its sixth year in March 2015 and believe there is a strong likelihood that it continues well beyond that date.

Conclusion

We do not believe the volatility seen in recent weeks, which is in-line with historical trends, is an early signal of a recession or bear market. Nor do we think the age of this bull market means it should end, given the favorable economic backdrop, central bank support, and reasonable valuations. Although we will continue to watch our favorite leading indicators for warning signs of something bigger, we think this latest bout of volatility is nothing more than a normal, though unwelcome, interruption within a long-term bull market. We maintain our positive outlook for stocks for the remainder of 2014 and into 2015.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

Price-to-earnings ratio is a valuation ratio of a company’s current share price compared to its per-share earnings.

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Tracking #1-317792 (Exp. 10/15)