By: Tim Gramatovich, CFA, CIO and Heather Rupp, CFA, Director of Research for Peritus Asset Management, the sub-advisory firm of the AdvisorShares Peritus High Yield ETF (HYLD)

Here are some of the reasons we believe that the high yield bond market looks attractive at current levels:

- MODERATE RISK: With default being the primary risk for high yield bonds and bank loan investing, we see no systemic default spike on the horizon, as maturities have been largely pushed out to 2017 and beyond1, companies have maintained reasonable discipline through this cycle, and capital markets remain functional, with CLO issuance setting records and high yield new issues continuing to print.

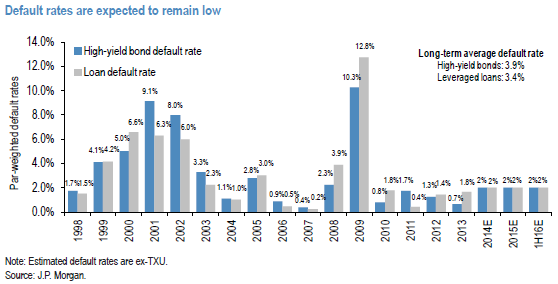

The current projections are for default rates to remain at about half of their historical level through the next couple years.2

- ATTRACTIVE SPREADS: With much of the secondary high yield market having been indiscriminately sold, we are now back to spread levels of 527bps on the index.3 This compares to historical median spread levels of 519bps over the last nearly 30 years.4 So we are at median spread levels, but with a well below average default outlook. While a portion of the index continues to trade at tight spreads to call prices, we are seeing plenty of bonds at 750 basis points, or more, over the 5-year Treasury, which is among the best we’ve seen when combined with overall risk outlook.

- U.S. FOCUS: Most high yield companies, and specifically our general area of focus in the mid-sized issuers, are largely domestically focused, which can serve to avoid some of the headwinds of a stronger U.S. dollar impacting exports and the conversion of foreign profits and weakening economic activity in other areas of the world, both of which we expect to be a drag on broad multinational companies and thus the major stock market averages.

- ALPHA POTENTIAL: The high yield and floating rate loan markets have dramatically expanded, now at $3 trillion, allowing active investors to work to create value through a variety of mechanisms, just like in a stock investing, including:

- Industry exposure—Strategically allocating to an industry we see as undervalued.

- Capital structure positioning—Secured or subordinate securities, taking advantage of what we see as the best risk/return potential within a company’s capital structure.

- Yield-to-Call—“Cushion” bonds for which we expect a near-term call.

- Avoiding negative convexity—Avoiding securities at large premiums over call prices.

- VOLATILITY: Volatility can create a great entry point, as often the average retail investor sells on emotion rather than fundamentals, thus creating potential opportunities for active managers to put on positions at a discount in individual securities within their portfolios, but also potential opportunities for those investing in these funds.

- APPEALING VALUE: The high yield market provides what we see as attractive, tangible income to investors. As we had mentioned, we are seeing plenty of opportunities at 750bps above the 5-year Treasury, which is now sub 1.5%, so if you theoretically could build a portfolio with a yield of 9%, and a default rate of 2%, with a recovery rate of 40% (the historical average)5, we are looking at a theoretical loss rate of 1.2% and a risk-adjusted yield of 7.8%.6 This compares to 1.5% on the 5-Year Treasury, 2.2% on the 10-Year Treasury, 2.89% on investment grade, and 1.99% on the municipal bonds.7 On a relative value, we believe the high yield market offers very compelling value.

1 Acciavatti, Peter D., Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Credit Strategy Weekly Update.” J.P. Morgan, North American High Yield and Leveraged Loan Research. October 3, 2014, p. 9.

2 Acciavatti, Peter D., Tony Linares, Nelson Jantzen, CFA, Rahul Sharma, and Chuanxin Li. “Credit Strategy Weekly Update.” J.P. Morgan, North American High Yield and Leveraged Loan Research. October 3, 2014, p. 11. As noted, the current default rate excludes the impact of TXU.

3 Index referenced is the Credit Suisse High Yield Index. The Credit Suisse High Yield Index is designed to mirror the investible universe of the $US-denominated high yield debt market. Data sourced from Credit Suisse, as of 10/14/14.

4 Historical spread data covers the period from 1/31/1986 to 9/30/2014.

5 The last 37 years of data have shown a recovery rate of 42.85%. Blau, Jonathan, James Esposito, and Daniyal Khan. “2014 Leveraged Finance Outlook and 2013 Annual Review,” Credit Suisse Global Leveraged Finance. February 6, 2014, p. 217

6 HYPOTHETICAL ONLY. These calculations assume that credit spreads remain constant and do not factor in any fees or expenses or changes in price movements for other reasons, including security fundamentals, etc. Actual results may be materially different. Default rates based on projected trends but actual results may be materially different.

7 U.S. 5 and 10 Year Treasury Note is sourced from the U.S. Department of Treasury, Daily Treasury Curve Rates. Investment Grade yield to worst based on the Barclays Corporate Investment Grade Index, which consists of publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and the quality requirements (source Barclays Capital). Municipal yield to worst based on the Barclays Municipal Bond Index, which covers the long-term, tax-exempt bond market (source Barclays Capital). All data as of 10/14/14.