Unemployment drops to six year low

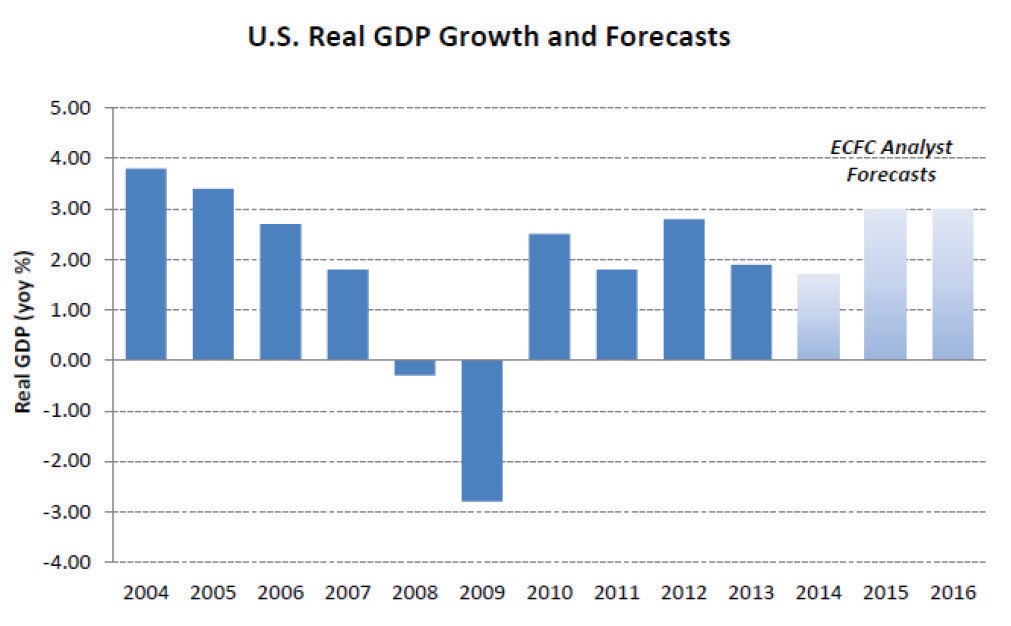

The U.S. economy continues to move forward in its slow but steady recovery. Recent reports show the unemployment rate dropping below 6.0% for the first time since 2008. A GDP growth rate of 4.6% in the second quarter also confirmed many economists’ expectations after a slow start to the year. This is in contrast to a Eurozone economy, which is struggling with deflation concerns in spite of continued efforts by the European Central Bank to ease its monetary policy. Several countries, including Germany and France, have seen their 2-year borrowing rates drop to a negative rate, effectively making banks pay interest for keeping deposits. This measure, along with other programs, is intended to promote lending and growth in countries that are lagging during the recovery.

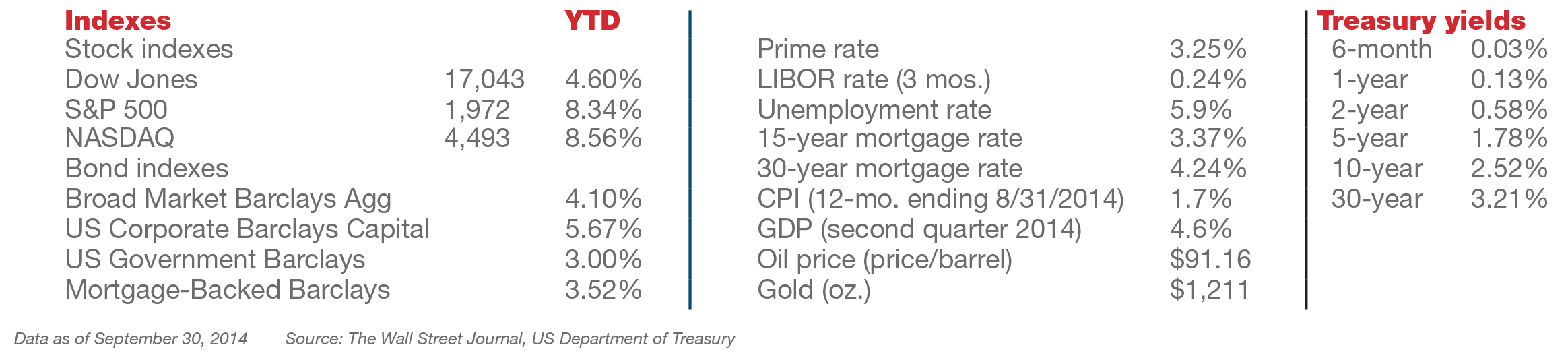

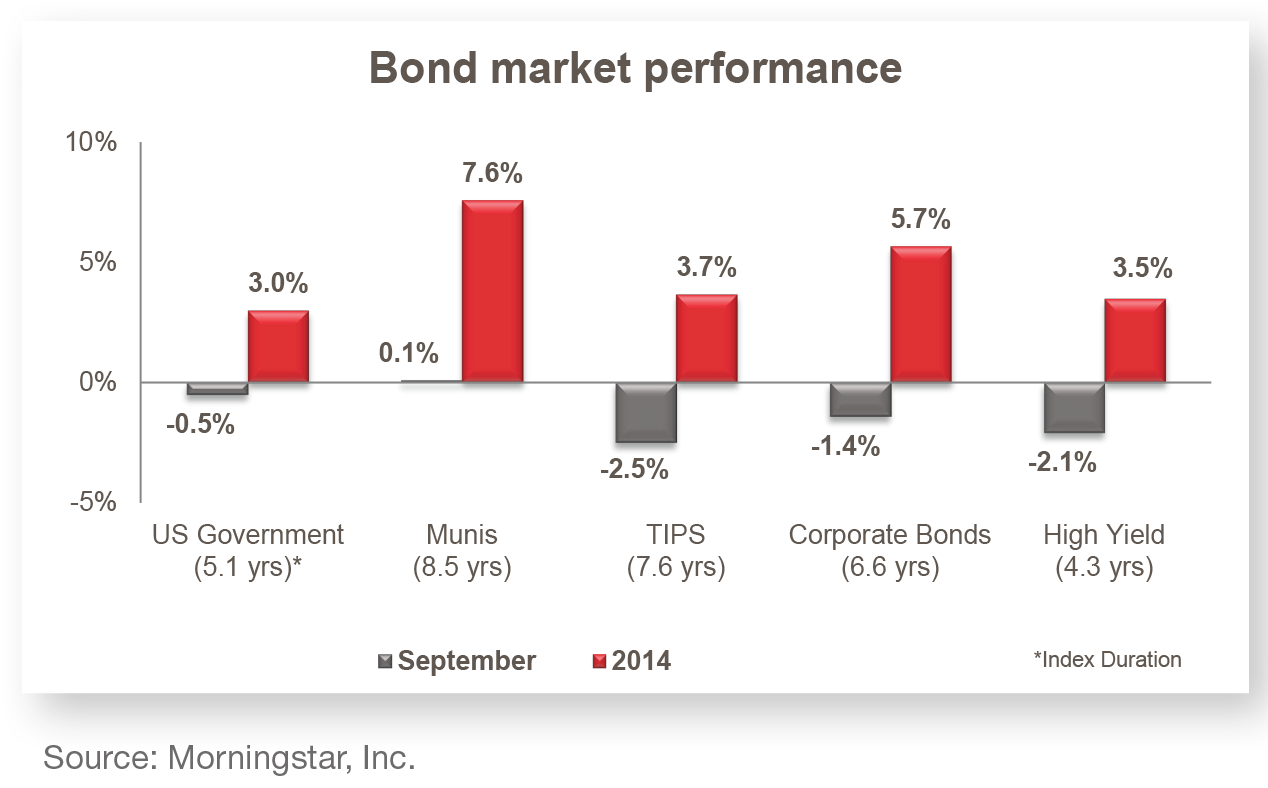

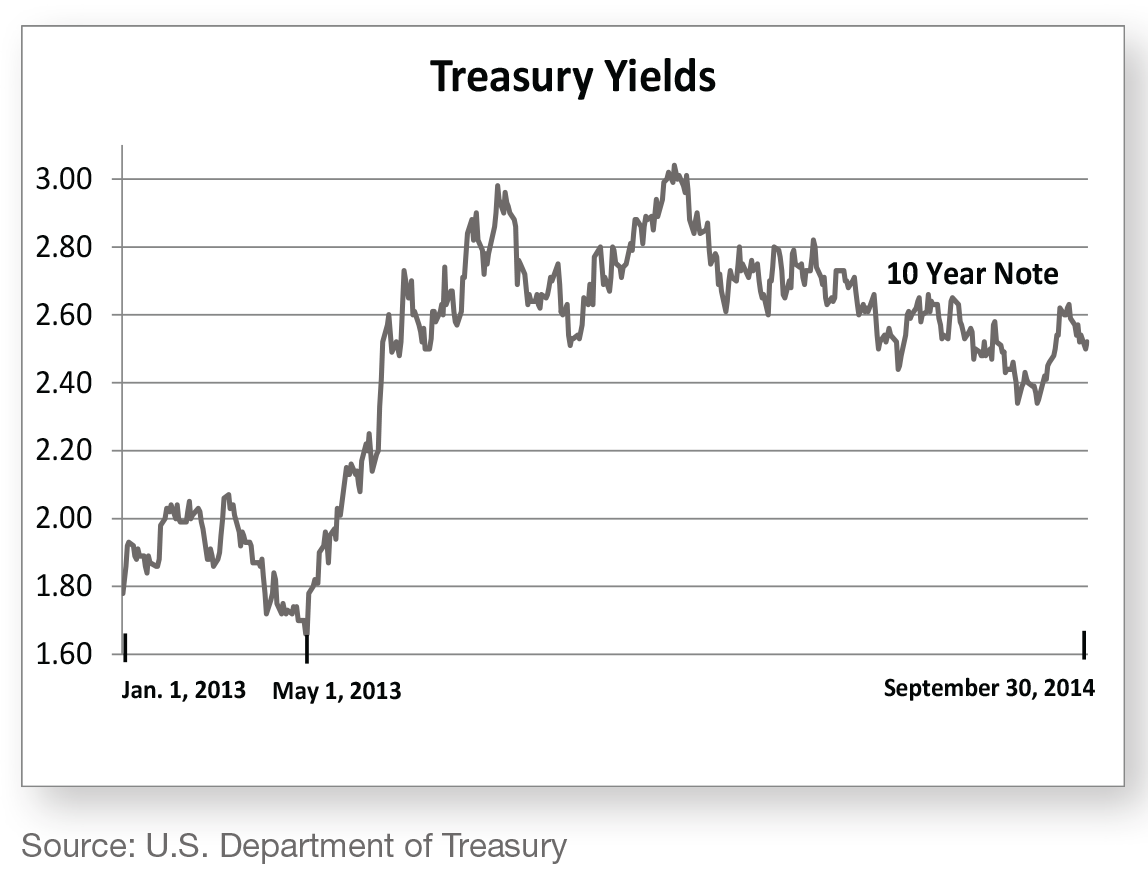

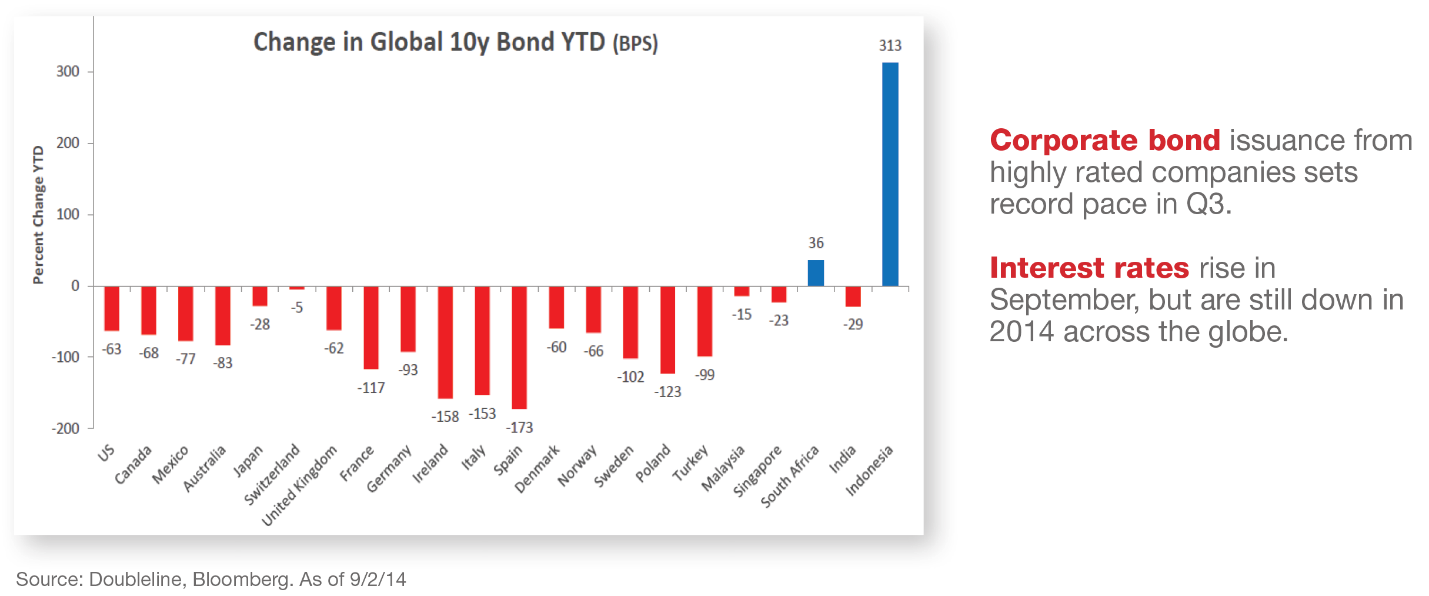

Bonds fall in September, still showing strong YTD

Interest rates generally rose during the month of September, but are still well below where they began 2014. Despite the Federal Reserve ending their bond buying program in October, demand for U.S. fixed income continues to be robust. This is in large part because of continued downward pressure on interest rates globally. As our chart in the subsequent fixed income section will show, 10-year government bond yields for several major foreign countries have fallen much farther than in the U.S. Rates on domestic sovereign debt are now four times higher than Japanese bonds and two times the yield of comparable German bonds. Also making headlines in late September was the departure of Bill Gross from PIMCO. The long-term impact that this will have on PIMCO investors is still largely unknown, but we do envision large outflows from mutual funds that Bill Gross was managing over the short-term.

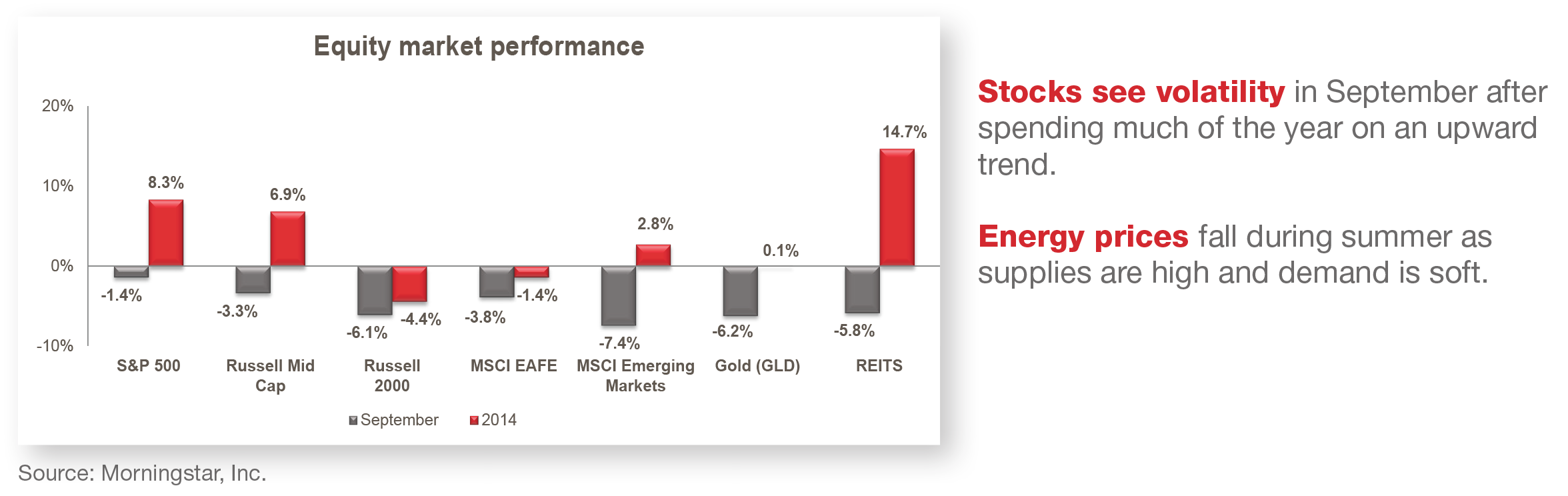

Stocks hold quarterly gains, but volatility increases

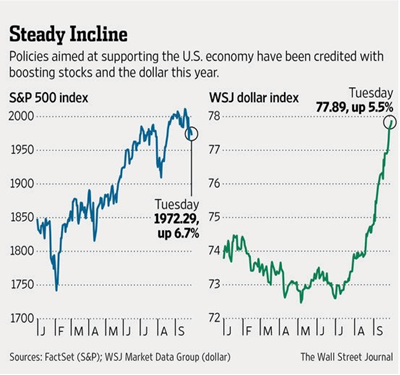

Domestic large cap stock index returns remained positive for the third quarter, notwithstanding a bout of increased volatility at quarter-end. The month of September proved difficult for many areas of the market, including foreign equities and alternative assets such as precious metals. commodities and real estate. We are seeing a significant strengthening of the dollar against other world currencies as the U.S. economy continues its expansion and other central banks continue to incorporate new stimulus programs. The dollar rose more than 8% against the Euro and Yen during the third quarter, reducing the return of the MSCI EAFE (international equity) Index for U.S.-based investors by approximately 5.5% year-to-date. The recent downward movement in the stock markets has some investors talking “correction” once again, and growth concerns overseas finally seem to affecting the performance of the domestic markets. We believe there is still more room for improvement for foreign economies, while the U.S. seems to be a more stable environment.

Bronfman E.L. Rothschild, LP is a registered investment advisor. Securities, when offered, are offered through Baker Tilly Capital, LLC, member of FINRA and SIPC; Office of Supervisory Jurisdiction located at 10 Terrace Court, Madison, WI 53718, phone 800.362.7301. Bronfman E.L. Rothschild, LP and Baker Tilly Capital, LLC are not affiliated.

This publication should not be viewed as a recommendation, an offer to sell, or a solicitation of an offer to buy a particular security or service. The commentary provided is for informational purposes only and should not be relied on for accounting, legal, tax, or investment advice. Financial information is from third-party sources. While such information is believed to be reliable, it is not verified or guaranteed. Performance of any indexes is provided for reference and competitive purposes only without factoring any fees, commissions, and other charges. Individual results achieved by investors will be different from those of the indexes. Indexes are unmanaged; one cannot invest directly into an index. The views and opinions expressed are those of Bronfman E.L. Rothschild, LP, and they are subject to change at any time. Past performance does not imply or guarantee future results. Investing in securities involves risks, including possible loss of principal. Diversification cannot assure a profit or guarantee against a loss. Investing involves other forms of risk that are not described here. For that reason, you should contact an investment professional before acting on any information in this publication.

© 2014 Bronfman E.L. Rothschild, LP

Stocks see short term swings, but end quarter higher.

Equity Market Performance

Bond Market Performance

Bronfman E.L. Rothschild, LP is a registered investment advisor. Securities, when offered, are offered through Baker Tilly Capital, LLC, member of FINRA and SIPC; Office of

Supervisory Jurisdiction located at 10 Terrace Court, Madison, WI 53718, phone 800.362.7301. Bronfman E.L. Rothschild, LP and Baker Tilly Capital, LLC are not affiliated.

This publication should not be viewed as a recommendation, an offer to sell, or a solicitation of an offer to buy a particular security or service. The commentary provided is for informational purposes only and should not be relied on for accounting, legal, tax, or investment advice. Financial information is from third-party sources. While such information is believed to be reliable, it is not verified or guaranteed. Performance of any indexes is provided for reference and competitive purposes only without factoring any fees, commissions, and other charges. Individual results achieved by investors will be different from those of the indexes. Indexes are unmanaged; one cannot invest directly into an index. The views and opinions expressed are those of Bronfman E.L. Rothschild, LP, and they are subject to change at any time. Past performance does not imply or guarantee future results. Investing in securities involves risks, including possible loss of principal. Diversification cannot assure a profit or guarantee against a loss. Investing involves other forms of risk that are not described here. For that reason, you should contact an investment professional before acting on any information in this publication.

© 2014 Bronfman E.L. Rothschild, LP