- We believe the oil sell-off is overdone and expect the commodity to find a floor in the low $80s.

- We expect firming global growth to increase the market’s confidence in global oil demand despite weakness in Europe.

- Energy service stocks are particularly oversold and may be attractive as the services-intensive U.S. energy renaissance continues.

Oil Hits the Skids

The S&P 500 fell 1% last week (October 13-17, 2014) in volatile trading, leading market participants and media pundits to speculate on how far the stock market slide--now just over 6% from the September 18, 2014, closing high--might go. In last week’s Weekly Market Commentary, “Pullback Perspective,” we cited the economic backdrop, central bank support, and valuations as reasons the pullback was unlikely to turn into a bear market (a 20% decline). This week we turn to an area that has already entered bear market territory and discuss our outlook for oil and the energy sector.

Oil has a significant impact on several key sectors of the economy, such as consumer spending, capital spending, and the transport sector.

Why Does Oil Matter?

Oil has a significant impact on several key sectors of the economy:

- Consumer spending. Consumers spend, on average, 4% of their income on energy (including oil, natural gas, refined gasoline, etc.). As a result, a sharp drop in energy costs can help provide a boost to consumer spending, particularly important as holiday shopping and winter heating season approach.

- Capital spending. Energy accounts for one-quarter of all capital spending globally, more than any other sector. Oil and gas exploration and production is very capital intensive, and significant infrastructure investments are needed to support the U.S. energy boom.

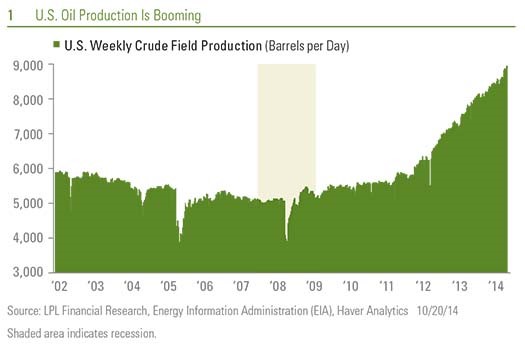

- Transport sector. Oil influences transports as a cost (fuel for airlines, shippers, trucks, etc.), but it also provides growth opportunities as an increasing amount of oil and petroleum products are transported by truck and rail due to the boom in U.S. energy production [Figure 1].

Keys to Finding a Floor

After falling 25% from its summer 2014 highs, West Texas Intermediate (WTI) crude oil, a long-accepted benchmark for U.S. oil prices, began to find its footing in the $81-82 range late last week (October 13-17, 2014). We believe this lower range may hold for several reasons:

- Slower global growth is already reflected in oil demand forecasts. Expectations for global oil demand have fallen significantly in recent months in response to slower growth in Europe, which is teetering on the brink of another recession. The International Energy Agency (IEA) cut its outlook for 2014 oil demand growth by 200,000 barrels per day, or 22%, from the agency’s prior forecast of 900,000. To give some perspective, total global oil demand is around 92 million barrels per day. The still firm demand outlook in the United States (despite ties to Europe), likely additional stimulus from China, and the expected demand boost from lower prices should reduce the chances of further material downgrades to global demand expectations.

- OPEC pressures are intensifying. Saudi Arabia has effectively engaged in a global price war, reportedly expressing comfort with prices as low as $80 to help drive down non-OPEC supply and defend its market share against U.S. shale production. We do not believe that Saudi Arabia, or OPEC, will tolerate prices much below $80 for very long. At lower prices, pressure would intensify to reduce supply from OPEC producers that require higher prices to balance budgets and maintain domestic political and social stability, such as Venezuela, Nigeria, and Iran. The next OPEC meeting is on November 27, 2014.

- Marginal cost support. With many domestic producers citing profitability down to prices as low as $60, we believe the downside is too great for OPEC to try to force significant production out of the market. The IEA has stated that just 4% of U.S. shale output needs prices above the $80 level to be profitable.

- Geopolitical risks. The potential for supply disruptions from uprisings in less stable oil producing regions may be underappreciated by the market with oil prices in the low $80s globally. Some of the recent drop in oil has been driven by output gains in Libya and Iraq despite civil wars in both countries, and security risks in Algeria and Nigeria are high. The longer oil prices stay low, the greater the potential for unrest.

- Oversold conditions technically. The swift and severe drop has left oil deeply oversold. Based on the 14-day relative strength index (RSI), a measure of oversold conditions, oil has reached oversold levels not seen since May 2012. Based on historical data, price declines of this severity leave a high probability of a potential oversold bounce or move higher in price [Figure 2].

Recovery May Be Bumpy

There are several risks to the downside for oil that suggest its recovery from recent lows may be bumpy:

- Elevated U.S. inventories. Additional pipeline development, export-friendly policies, and stronger demand are needed to help clear out excess inventories in the United States [Figure 3]. Though it will take time, more U.S. exports could put downward pressure on domestic inventories and support prices. Globally, the oil market is expected to be slightly oversupplied in 2015.

- OPEC is a wildcard. With so many U.S. producers profitable at prices well below $80, and as fracking technology continues to advance, the possibility exists that Saudi Arabia would attempt to test the market at $75 or lower to see how much production it could shake out of the market. We see this possibility as low, but higher cost production in the United States, Iran, and Russia could be targets for possible OPEC market share gains.

- Global growth may slow further. We do not have much confidence that growth in Europe will improve, as we discussed last month in our two-part Weekly Market Commentary, “Don’t Fight the ECB?” A prolonged recession in the Eurozone could put additional downward pressure on global oil demand.

- Currency risk. A strong U.S. dollar makes commodities priced globally in dollars more expensive for foreign buyers. Oil has exhibited inverse correlation with the dollar in recent years and may fall further (or rise more slowly) should the dollar strength continue.

Energy Sector Opportunities

We believe the energy sector may be a good place for investors to look for bargains now that the market is pricing in much lower oil prices and valuations have fallen. We would expect higher oil prices to support an eventual rebound in energy stocks in the coming months, further bolstered by extreme oversold conditions [Figure 4] and favorable seasonality. Specifically, energy service stocks are particularly oversold and may be attractive as the services-intensive U.S. energy renaissance continues. We view master limited partnerships (MLP) and their rich yields as attractive, after the group sold off sharply on fears of reduced U.S. production at lower prices. Significant infrastructure investment is required for the U.S. energy renaissance, and we believe the pipeline MLPs, which have experienced more energy price sensitivity in recent weeks than we believe is warranted, remain well positioned to take advantage of that opportunity.

We believe the oil sell-off is overdone and expect the commodity to find a floor in the low $80s. We expect firming global growth to increase the market’s confidence in global oil demand despite weakness in Europe. At the same time, we expect the prospect for (or actual) tighter OPEC supply will provide support for prices in this range. Booming U.S. production and a global price war present manageable risks, in our view, and we would expect the market to find its supply-demand equilibrium--and in turn, more solid footing--in fairly short order.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

Investing in MLPs involves a high degree of risk including risks related to cash flow, dilution, and voting rights. MLPs may trade less frequently than larger companies due to their smaller capitalizations, which may result in erratic price movement or difficulty in buying or selling. MLPs are subject to significant regulation and may be adversely affected by changes in the regulatory environment including the risk that an MLP could lose its tax status as a partnership.

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1-320410 (Exp. 10/15)