“Credit expansion is the government’s foremost tool in their struggle against the market economy. In their hands it is the magic wand designed to conjure away the scarcity of capital goods, to lower the rate of interest or to abolish it altogether, to finance lavish government spending, to expropriate the capitalists, to contrive everlasting booms, and to make everybody prosperous.”

Ludwig von Mises, 1881-1973

Economist, Philosopher and Teacher

Author of “Human Action: A Treatise on Economics”

Born in the city of Lemberg in the Austrian-Hungarian empire (present-day Ukraine) (future-day Russia?), Ludwig von Mises would be a familiar figure to those interested in the intellectual underpinnings of economic libertarianism. He was an important contributor to the Austrian school of economic thought, which, while ultimately losing mainstream support to the Keynesians and their followers, has still remained influential in certain circles as an alternative. Von Mises was also an extreme skeptic of the “prosperity” engendered by credit booms, which is why he graces our front page today.

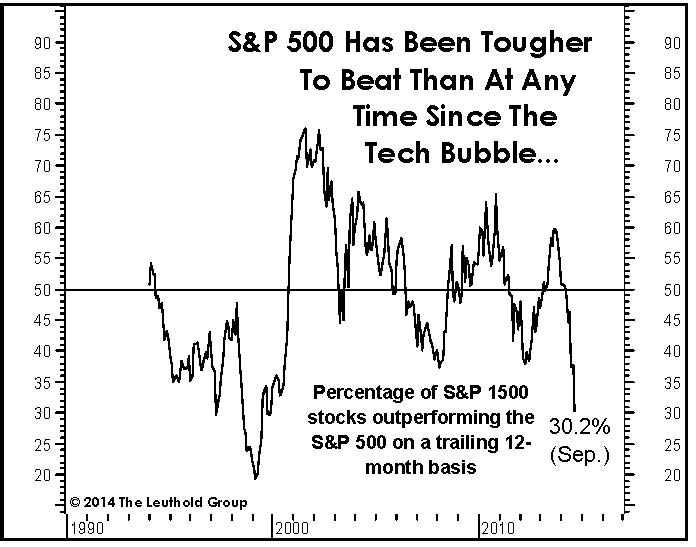

But before we address that topic, let’s review the equity market, which has seen a rough road of late. As we write, 62% of S&P 500 stocks are more than 10% off their highs and 49% of the stocks in the Russell 2000 small cap index are more than 20% off their highs. Both the broad NYSE composite and the Dow Jones Industrial Average (DJIA) sit in loss territory for the year to date. Just last month the S&P 500 Index hit all-time highs to great fanfare as the biggest IPO in history, Alibaba, came roaring into public existence. It may surprise some to learn that most stocks were declining even while the S&P was making new highs. Hence even before October’s sharp drop, the reality is that the majority of stocks were already negative for the year. Such divergent “market internals” are traditionally not a good sign... as is being increasingly validated as we go to press.

Investment results have been sharply divided along the lines of company size (i.e. market capitalization). This past quarter, small cap stocks lagged large cap stocks by over eight percent, a trouncing not seen since the first quarter of 1999 which slightly proceeded the bursting of the tech bubble. Standard & Poor’s tracks 1,500 stocks; the chart to the left shows their year-to-date performance through October 6th after sorting by market cap size. Rarely do we see markets with such schizophrenic multiple personalities.

One might think that at any time half of stocks would be outperforming the market “average” simply due to the nature of averages... but not so, because the S&P market index is not actually a traditional equal-weighted average but is instead heavily weighted toward the aforementioned (better performing) larger market cap stocks. Hence, as the chart at right shows, over the last 12 months only 30% of those 1,500 stocks mentioned earlier were beating the S&P 500 Index as of the end of September. This is again indicative of a narrowing environment not seen since the late 1990’s tech bubble.

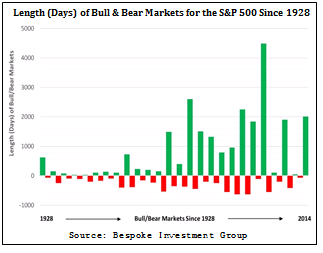

The chart to the below shows the length, or duration, of bull and bear markets, defined as advances of at least 20% following a decline of at least 20% (and vice versa). The current bull market, which began in March of 2009, crossed the 2,000 day mark last month... making it pretty long in the tooth as far as these things have historically progressed. In recognition of both this and rising equity valuations, we raised cash to roughly 15%, taking profits in our Lands’ End position after it was spun off from Sears Holdings (equivalent to $13 per Sears share), and selling General Electric given our belief that it will more or less trade with the broader market. While any stock portfolio remains exposed to the vagaries of the market, our more recently purchased positions are intended to be somewhat less tied to the direction of the overall U.S. equity market (i.e. Navient, Turkcell, Vectrus).

Transitioning back to credit booms and busts, we’d like to present a short vignette on this quarter’s quoted figure, Ludwig von Mises. Supposedly, every week he would walk through the great passageway of the Kreditanstalt Bank in Vienna and, wary of its great expansion of credit, would remark to his confidante, “That will be a big smash”. For five years this was his consistent lament... until the market cataclysms of 1929 and the institution’s ultimate bankruptcy in 1931. Von Mises wouldn’t have been a good money manager, calling the failure a full seven years too early, but ultimately he was correct.

Von Mises held that credit booms caused by an artificially low cost of credit lead to poorly allocated spending, or malinvestments (think Alaska’s “Bridge to Nowhere”). This eventually leads to an inevitable smash/bust when such malinvestments are eventually exposed for what they are. It has similarly been observed in macroeconomics that fixed investment spending booms (i.e. willy nilly construction booms) eventually lead to busts as well. If he were still alive today, von Mises would no doubt have no small amount of criticism for Western financial systems. We contend, however, that he might first have gazed across the Pacific and remarked, “That will be a big smash”.

Nowhere in the world has there been a credit-financed fixed-investment boom like the one China has had. Forty-seven percent of China’s 2013 output came from fixed investment. This contrasts with developed economies generally below 20% and other emerging market economies generally below 30%.

Further, fully 14% of China’s urban labor is employed in construction. Put in more (sorry...) concrete terms, China has used more cement in the last three years than the U.S. used in the entire 20th century. Economies around the world have adapted to help support China’s building boom. For example, the world’s output of iron ore has roughly tripled since 2000. Thus it’s been fixed investments... the building of high speed rail systems, glittering new cities, and houses, lots of houses... which have powered the Chinese economic engine. Could China’s semi-communistic system have directed all these investments successfully/profitably? If not, what happens if these investments turn out to have been malinvestments? What happens to all those urban workers when they run out of useful things to build?

Malinvestment in American housing resulted in a slew of defaults by the builders, financiers, and owners of homes. These defaults were followed by no small amount of economic disruption. In China, there is no such slew of defaults... for now. China’s Communist party orchestrated the boom of previous decades partially by controlling the state-owned banks and using them to allocate credit to desired areas of growth. Want a supertanker business in Southeast China? Well simply call your friends at the banks and tell them to lend a couple billion yuan to the shipbuilder of your choice. (Naturally the official issuing such a directive will be driven solely by rational, impartial economic analysis and nothing else). And if those shipbuilders can’t pay back the loans at maturity...? Why, simply have the bank make a new loan to replace the old one (i.e. sweep it under the rug)... we wouldn’t want our party officials or corporate officers looking silly now would we? In the U.S., despite relatively independent regulators, free competition, and a vigorous free press, companies can sometimes hide their losses for years. In China, with no such tradition, where information is under much stricter control and with a possibly complicit government, we have no doubt that such losses could be hidden for a much longer duration, but not indefinitely, and not without some consequences leaking out.

The potential for exposure and recognition of these losses might be a ticking time bomb because China is pretty levered, and leverage magnifies downturns. China’s debt has burgeoned while its economic growth has slowed (see chart above). A prominent financial commentator has mused that if Russia is a gas station pretending to be a country (as quipped by Senator John McCain), then China is a bank pretending to be a country. China’s banking assets sum to $26 trillion, 257% of China’s GDP; this compares with much lower ratios for the U.S. and other large emerging economies (see chart above left) but is in line with the developed (and precarious) financial systems in Europe[1].

While warnings about the potential repercussions of China’s rapid growth are not new, we believe these warnings suffer from a “failure of imagination” in terms of how severe the consequences might be. This is reminiscent of banks, when asked before the financial crisis to show how they might fare in a severe economic disturbance, not one showed that it would eat through even a third of its regulatory capital (we now know they not only ate through all their capital but required billions of additional padding from the government). We often hear so-called “China Bears” talking about three to four percent growth in China, or a “China slowdown”, or “China softening”. Oh what a tragedy those small single digit GDP growth numbers would represent! The last time we checked, financial crises usually result in negative growth numbers. See the above chart showing economic growth rates of the Asian Tigers before and after the East Asian crisis of 1997.

If China experiences a credit collapse, we think the damage to the world economy (and the image of the Chinese miracle) could be much worse than commonly depicted. If it were to experience a 10 percentage point decline in GDP growth as did the countries above, China would be facing negative three percent GDP growth[2].

While we aren’t predicting an imminent collapse, some cracks are starting to emerge in the economic façade of the eastern monolith.

First, in the housing market:

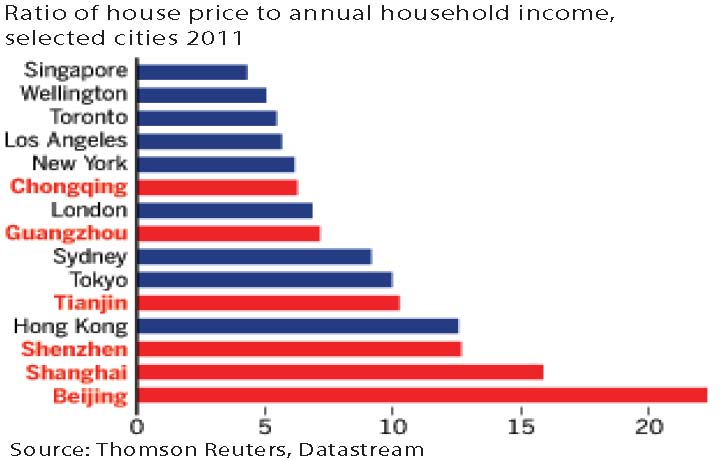

- China’s housing has long been unaffordable – see chart at right

- Chinese households hold a lot of their wealth in housing – 41% as of 2011 vs 26% for the U.S. We read news reports of families owning six vacant apartments, etc.

- Chinese housing prices have been declining for five straight months, at a recently accelerating rate, amid double digit declines in transaction volumes

- The government has recently gone from working to prevent home price speculation/appreciation, to undertaking opposite efforts to prop up prices

Second, in the commodities market:

- In recent years China has represented an incredible 40%+ share of global consumption of commodities such as copper and steel (see charts at right)... as well as many others

- Since 2010, industrial commodities have declined in price as follows: aluminum -16%; copper -25%; coal -44%; iron ore -51%

- In the not-so-distant past, the price of crude oil was in triple digits and was assumed to remain there for eternity. As of mid-October, oil prices are on the verge of tripping below $80, having fallen precipitously as new supply in the form of North American shale has emerged and the “previously-accepted-as-fact” juggernaut of increasing emerging market demand for oil has failed to show up in sufficient strength

We write this mainly to inform our readers as to some of our views on the state of the world. All the hysteria around China’s rise in the 21st century reminds of similar hysteria around Japan’s rise in the 80’s; the rise is real but exaggerated and far from bulletproof. At Knightsbridge, we are not macro investors and do not seek to make bets on overseas economic collapse. Indeed, as von Mises’ example with the Kreditanstalt Bank shows, it is very easy to be disastrously early in predicting collapse. However, we do seek to use our views to help manage risk. Indeed, our views on the risks of a Chinese stumble and on the commodity boom associated with its rise, contributed to our retrospectively helpful decisions to sell Freeport-McMoRan (FCX, exposure to copper) and McDermott International (MDR, obsolete business if oil prices fall sufficiently). If we had let our Chinese demand concerns further influence our opinion on oil, then we might have sold Pengrowth Energy (PGH), which now appears would have been a wise move.

Recent economic events (Chinese and European weakness, lower oil prices) might lead the Fed to forestall raising interest rates and leave them “lower for longer”. While we certainly did not predict this, we are reminded of the warning we issued earlier this year not to bet on the “fact” that interest rates would rise. Indeed, as we write this, the 10-year treasury has dipped below two percent. To paraphrase an old saying from macro investing, “what’s obvious is obviously wrong”.

Despite recent market conditions and the negative tone of this letter, we don’t advise clients to brace for disaster just yet. As mentioned, we recently raised cash to help weather stormy conditions and, for long-term investors at least, price declines are usually temporary. At the appropriate time, we will be seeking to use the new lower price tags on American companies to your benefit, by purchasing some that are on sale.

One soon-to-be-potentially-favorable aspect of market conditions is illustrated on the chart to the left. When it comes to mid-term election years, the period from November through the next April has in the past produced outsized gains in the S&P 500 Index. This has been a consistent trend, with U.S. equities higher a year after each of the past 16 mid-term elections. Even if there is no economic reason behind this, the psychological effect of the pattern helps to perpetuate this phenomenon.

After the financial crisis, we sometimes heard from people we respect that they thought the stock market would do just fine, but they were worried about American business. They turned out to be more or less right. We now think the situation might be reversing: American business seems to be back on more solid footing but the market is looking weak. Even in the event of a continued market pull-back, the fact that businesses appear to be on solid footing should be of some comfort, because absent a recession, pull-backs tend to be more modest with quicker recoveries.

As always, we humbly thank you for the trust you place in us.

Very Truly Yours,

[1] This metric doesn’t always present a fair comparison because of different financial system structures. For example, in the U.S., companies are much more likely to have debt in the form of bonds which don’t count as banking system assets whereas in Europe bank debt is much more prevalent. Furthermore, it is generally the case that developed economies can much more safely support higher levels of financial assets and so a similar level would represent a higher state of fragility for an emerging economy such as China.

[2] To be fair, after its financial crisis, Japan did not have negative economic growth rates... but they did (and do) have decades of low single digit rates which, if seen in China, would also be a dramatic shock.

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.