How Exchange-Traded Futures Can Improve the Efficiency of Gold & Currency Linked ETFs

Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

With a number of gold and currency linked ETFs now using exchange traded futures to gain their gold and currency exposure versus the alternative of holding physical gold/hard foreign currency, we discuss below some of the key features of these futures markets which, in our view, mitigate most if not all of the concerns investor may have about these futures based ETPs.

-

Physical delivery / Exchange for Physical help to limit basis risk

Most gold ETFs that use futures to gain gold exposure will use the COMEX 100 ounce gold futures contract which is the most liquid gold futures contract in the world. The Commodity Exchange (COMEX) is a commodity exchange owned by the Chicago Mercantile Exchange (CME) - as part of its gold exchange the COMEX offers warehousing for its members. This facilitates a key feature of the COMEX gold future which is that it can be physically settled – in other words traders can choose to settle open contract positions they hold at maturity with delivery of physical gold. The warehousing facilities that the exchange offers provides a convenient method for traders to complete physical delivery with the gold held in the exchange’s vaults being readily transferred between members accounts at low cost. In practice the way this happens is that a member that chooses to store gold at the COMEX is able to classify some or all of its gold as “registered” meaning that these bars are available for delivery to settle open futures positions. In effect “registered” gold provides backing for the futures contracts traded on the exchange and while the ratio of registered gold to futures contracts outstanding fluctuates on a daily basis, this physical delivery mechanism that the exchange provides is a key feature for the efficient functioning of the gold futures market. Similarly the foreign exchange (FX) futures contracts that trade on the CME are all settle for physical delivery. Ultimately from the point of view of an investor, the major implication of the physical delivery mechanism is that the price of gold or FX rates on futures markets must by definition closely track the price of gold or FX rates on cash markets otherwise there would be an opportunity to trade one market against the other and earn risk free profits.

Another feature of futures markets that mitigates the potential for so-called “basis risk” (the extent to which prices in the futures market are different from prices in the cash market is the “exchange for physical” (EFP) mechanism. In an EFP transaction, one market participant holds a long asset position via a futures contract while another market participant holds the exact same long asset position but via the physical market. If the participant that holds the futures contract wishes to switch into a physical holding and the other wishes to switch their physical holding into a futures position, it is possible for the two parties to agree to exchange their respective holdings in a private off-exchange agreement but then settle the transaction on the exchange. There are a number of commercial reasons for why the two parties might want to do this but fundamentally, from the point of view of an investor in a futures-backed ETF, the EFP mechanism provides another control mechanism limiting the potential for basis risk between the two markets. -

Bridging liquidity between the cash and futures markets

Another significant benefit of the EFP mechanism is that it effectively provides a bridge between the liquidity available in the futures market and that available in the cash market. Traders in the cash market are able to provide liquidity to the futures markets, hedge their risk in the cash market but then swap the hedge from the cash market to the futures market using the EFP mechanism. In effect, this means that for a market participant looking to transact on the futures market, the true extent of available liquidity is not just the liquidity available in the futures markets but a greater amount reflecting the liquidity available on both markets. And given that the liquidity in cash markets can at times be multiples of what is readily “visible” on futures market, this can significantly extend the depth of futures markets allowing market participants greater capacity to transact larger transactions.

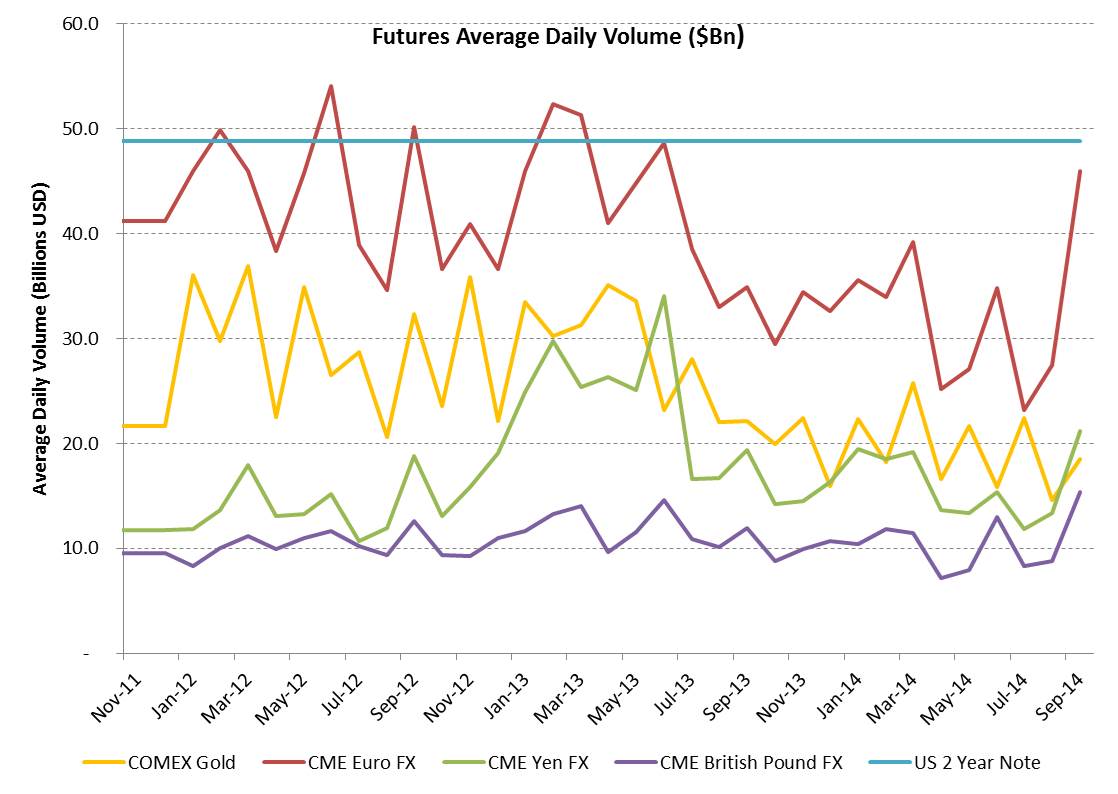

Source: Chicago Mercantile Exchange. Past performance is not indicative of future results.

The chart above shows the average daily volume trades (in USD billions) of gold, euro, yen and pound contracts on the CME, with the average daily volume for the 2 year US note, a highly liquid contract also on the CME, shown for reference. In combination with cash markets, this chart reflects the huge capacity available for executing both gold and FX transactions on futures markets.

-

Block trades also enhance liquidity

A block trade is mechanism available to futures market participants that permit them to negotiate an off-exchange transaction but then settle the transaction on the exchange in the traditional manner. A block trade must generally be reported to the exchange within 5-15 minutes depending on the specific contract transacted. The benefit of the block trade is that it gives participants the ability to execute a large transaction at a “fair and reasonable single price” that is negotiated privately between the two participants and which would be difficult to achieve if the transaction was negotiated openly on the exchange. Block trades must meet minimum size thresholds and are open only to “eligible contract participants” pre-approved by the exchange. -

“Trade at Settlement” can help to reduce tracking error

Another feature of the COMEX gold future that facilitates efficient execution is the Trade At Settlement (TAS) facility. TAS matches bids and offers from market participants who wish to execute their futures trades at the exchange’s Daily Settlement Price. By using TAS, a futures-backed gold ETF can be guaranteed execution at or close to the Daily Settlement Price thereby avoiding the need to execute the transaction in the open market. Tracking error is also therefore minimized as the Daily Settlement Price is the price used to calculate the ETF’s NAV at the close. -

Mitigating credit risk

The final feature of futures markets which is of critical importance to investors in futures-backed ETFs is that they place the credit risk (the risk that either participant in the transaction does not meet their obligations) that the participant faces against the exchange rather than against the other participant in the transaction. So while both participants may negotiate and agree a transaction directly with each other, in the process of settling the transaction, both participants’ counterpart in the transaction is transformed to become the exchange (rather than the other participant). And to the extent that an exchange is a regulated entity mandated to demand “adequate” amounts of collateral from participants to protect against market risk, this significantly mitigates the risk that a futures-backed ETF might bear from transacting off-exchange with any individual market participant.