This week, the U.S. Department of Commerce will provide the markets and the public with the first look at the health of the economy in the third quarter of 2014, when it releases the figures on gross domestic product (GDP). The consensus of economists, as polled by Bloomberg News, expects that the U.S. economy expanded at a 3% annualized rate in the quarter, after posting a 4.6% increase in the second quarter, which in turn, was a rebound from the weather-impacted 2.1% drop in GDP in the first quarter of 2014.

Although the Great Recession ended in the middle of 2009, and the U.S. economy (as measured by GDP) surpassed its pre-Great Recession peak in late 2011, many Americans still don’t feel comfortable about the economy. In a recent Gallup poll, nearly 40% of Americans listed one or more concerns about the economy as the most important problem facing the United States. While the latest reading is still far below the nearly 90% of Americans who listed economic issues as the biggest problem facing the United States in early 2009 (during the depths of the Great Recession), the 40% reading is still well above the “normal” level of around 20-25% seen in the mid-2000s.

Our view remains that the U.S. economy is in the middle stages of a recovery that began in mid-2009. Based on the data, the odds of a recession occurring in the next several years are low, as the slow pace of the recovery thus far has prevented the excesses that typically precede a recession -- overbuilding, overspending, overinvesting, etc. -- from building up. But the slow pace of the recovery -- especially the labor market, and in particular wage growth -- has contributed to the feeling among a large percentage of Americans that the economy is not where it should be at this stage in the business cycle.

The following figures provide a somewhat alternate look at the economy over the past several years. Without citing any of the usual government reported statistics (GDP, jobs report, retail sales, industrial production, durable goods orders, etc.), these figures on economic uncertainty, crane rental rates, and restaurant customer traffic tell a story that is remarkably similar to the one told by the official data on the economy: The economy is improving, and in many cases is back to normal, but in some areas remains stubbornly weak.

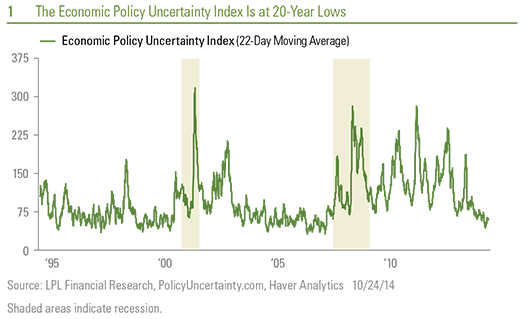

The Economic Policy Uncertainty Index is compiled by researchers at Stanford University and the University of Chicago, and it measures mentions of economic policy uncertainty in over 1,000 newspapers across the country [Figure 1]. While investors have plenty to worry about today, the index is currently near 20-year lows, despite fears of Ebola and worries about the Islamic State militants, Ukraine, and a global growth slowdown in Europe, China, and elsewhere. Earlier spikes in the Economic Policy Uncertainty Index included:

- 2008 and 2009, due to the Great Recession and the rancor over the fiscal stimulus, the Federal Reserve’s (Fed) quantitative easing (QE) program, the auto sector bailout, and the Troubled Asset Relief Program (TARP)

- 2010, around the debate and passage of the Affordable Care Act

- 2011, around the debt ceiling debacle and the downgrade of U.S. government debt by Standard & Poor’s

- 2012 and 2013, around the fiscal cliff, government shutdown, and

the sequester

In short, economic uncertainty -- likely a drag on economic growth in 2011, 2012, and 2013 -- has faded as a concern in 2014, consistent with the Fed’s most recent Beige Book. (See last week’s Weekly Economic Commentary, “Beige Book: Window on Main Street.”)

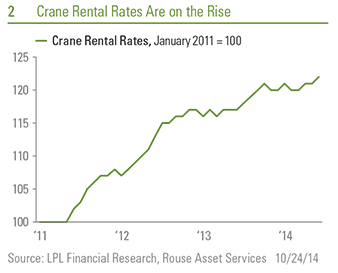

The crane rental rates in Figure 2 are collected by Rouse Asset Services and track the rental rates for boom cranes used on large construction sites around the country. Rates are up by nearly 25% since early 2011 (the earliest data we have available), and a quick look around any major metropolitan area around the country should tell you why. The rise of giant construction cranes across the country, after a long absence, is a very visible sign of the recovery in the economy. Although business spending on structures -- the area of the economy that is most closely tied to crane rental rates -- is not yet back to pre-Great Recession peaks, this segment of GDP typically lags the overall economy. Uncertainty around the durability of the recovery in the early years of this decade led to pent-up demand among businesses for new and expanded space, which has given rise to an uptick in activity at commercial building sites. Low rates to finance all the spending -- partially as a result of the Fed’s actions -- have helped. We continue to expect that business capital spending on structures may be a positive contributor to overall GDP growth in the coming quarters.

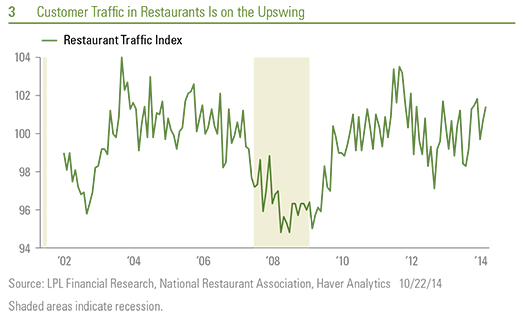

The data on customer traffic in restaurants, compiled by the National Restaurant Association, show that customer traffic in restaurants across the country is very close to being back to normal, after struggling in the early part of the recovery (2009 and 2010) and again around the fiscal issues in 2011 and 2012 [Figure 3]. While not quite back to the levels seen in 2004-2007, customer traffic in restaurants is on the upswing, and anyone who has been out to dinner on a weekend night lately knows that translates into long wait times for tables. A better housing market, the improved labor market, pent-up demand from earlier in the recovery, and the discipline to not overbuild restaurants in the prior cycle have led to the recent increase in customer traffic.

Although there are other “real world” indicators on the health of the U.S. economy (we promise to bring you more in forthcoming editions of the Weekly Economic Commentary), the three discussed here are indicative of the health of the U.S. economy more than five years into the economic expansion that began in mid-2009. It’s in recovery, but a slow recovery, and not quite “back to normal.” We hope you are not reading this while waiting for a table at your favorite restaurant!

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking # 1-322687 (Exp. 10/15)