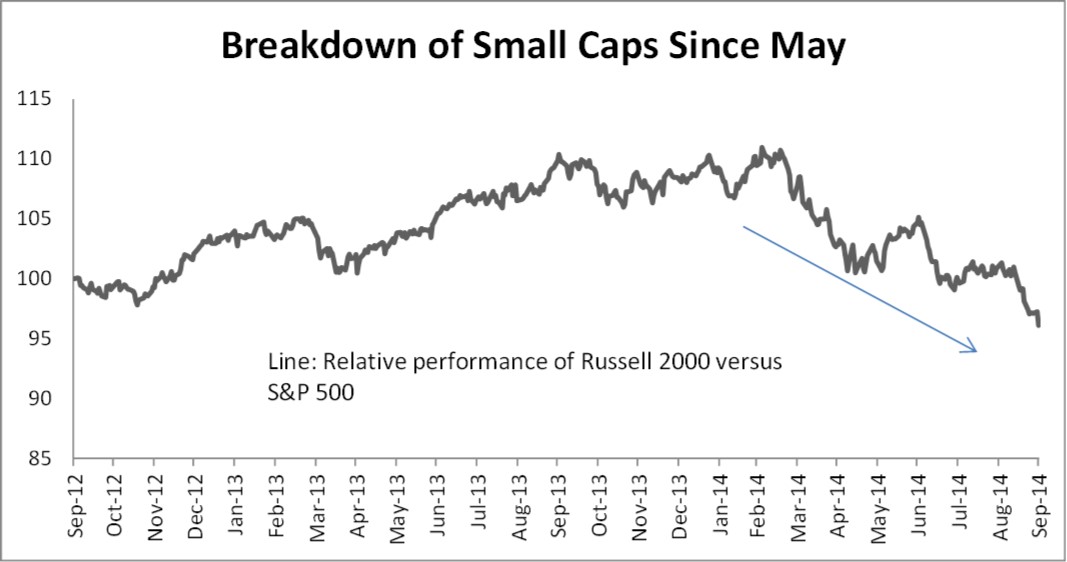

There is no shortage of discussions on Small Cap underperformance of late (see the familiar Chart 1). Many reasons have been proposed to account for the recent momentum breakdown:

Chart 1

- Small Caps have had a good run for a number of years and performed well last year too. It's time for profit taking.

- Small Cap valuations are running high. This is true based on our decades long data which monitors the relative valuations of Small Caps versus Large Caps (see "Stock Market Internals" section).

- Market sentiment turned negative; high risk, volatile Small Caps take a beating.

Here we throw in yet another idea as food for thought. This rationale takes a deeper look at the fundamentals: the leverage of companies' balance sheets. With the Fed mulling over a rate increase, investors may have already started to avoid companies with excess leverage. Unfortunately, the data suggests that Small Caps, on average, are in this camp.

Leverage Ratios Creeping Up Among Small Caps

Our data crunching shows that the leverage ratios have been creeping up among Small Caps since the 2010 lows (relative to Large Caps). From a leverage affordability standpoint (interest rate coverage ratio for example), Small Caps are also showing signs of deterioration.

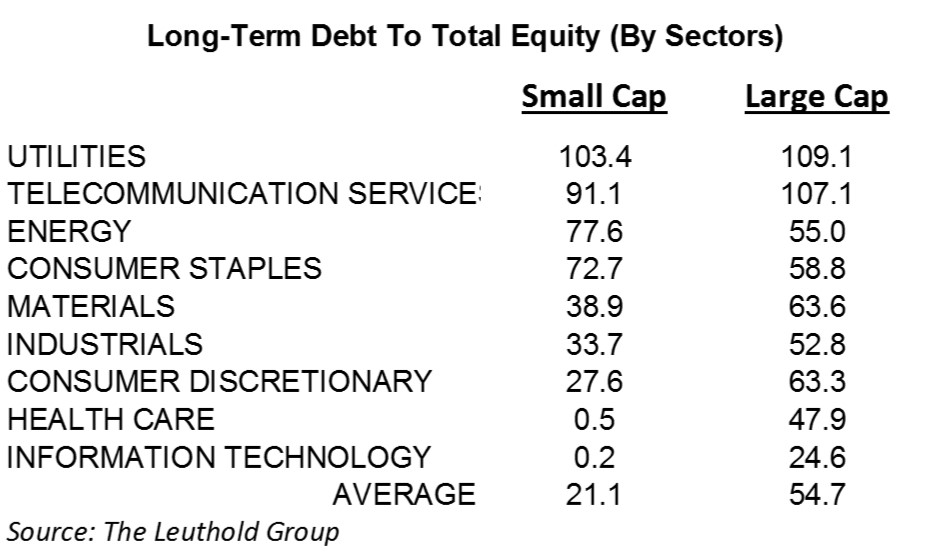

We looked at two leverage ratios: 1) Total Debt to Total Assets; and, 2) Long Term Debt to Equity. Each is presented as a ratio of ratios (Charts 2 and 3), to demonstrate Small Caps' leverage relative to Large Caps. Rising lines mean rising leverage among Small Caps relative to their Large Cap counterparts.

Both charts show the rising trend of Small Cap leverage since the 2010 low. Total Debt to Total Assets ratio of ratios is approaching its long run average, while the Long Term Debt to Equity ratio of ratios has exceeded its long term average, a significant jump from 2010.

Chart 2

Chart 3

Charts 2 and 3 also show that Small Cap leverage levels have historically been lower than Large Caps' (long-term average ratio of ratios is below one). This is not surprising since loans are normally harder to come by for higher risk, small companies, especially in Health Care and Tech sectors, where Small Cap companies have generally relied on equity funding, instead of loans.

As of now, average Total Debt to Total Assets among Small Caps stands at 16.0%, lower than Large Caps' 26.8% (Table 1). However, breaking down by sectors, we see that leverage is significantly lower for Small Caps' Health Care and Info Tech sectors, which drags down the average. Small companies in Consumer Staples, Energy, and Telecommunication Services actually have higher leverage ratios than their corresponding Large Cap sectors. A similar pattern can be observed when looking at the Long Term Debt to Total Equity ratio (Table 2).

Table 1

Table 2

Loans May Become Less Affordable Among Small Caps

Sometimes low leverage ratios do not speak for a better balance sheet, if a company's earnings power does not keep up with the cost of servicing loans. Chart 4 shows that Small Caps' interest coverage ratio (EBIT/interest expenses) relative to Large Caps' has been on the decline since 1998, and now stands at historical lows.

Rising interest rates could further exacerbate this situation as small companies tend to have floating rate bank loans or bonds with shorter maturities. The latter means that most Small Cap companies may have to refinance their loans at higher interest rates leading to even higher loan service expenses.

Chart 4

Conclusion

Small Caps' balance sheets and debt servicing capacity are not in the healthiest state to weather higher interest rates (relative to Large Caps). This could be part of the big picture of weakening Small Cap performance. Small Cap investors should place an emphasis on companies with relatively stronger balance sheets, and higher earnings power in order to accommodate an environment of rising interest rates.

© The Leuthold Group