Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

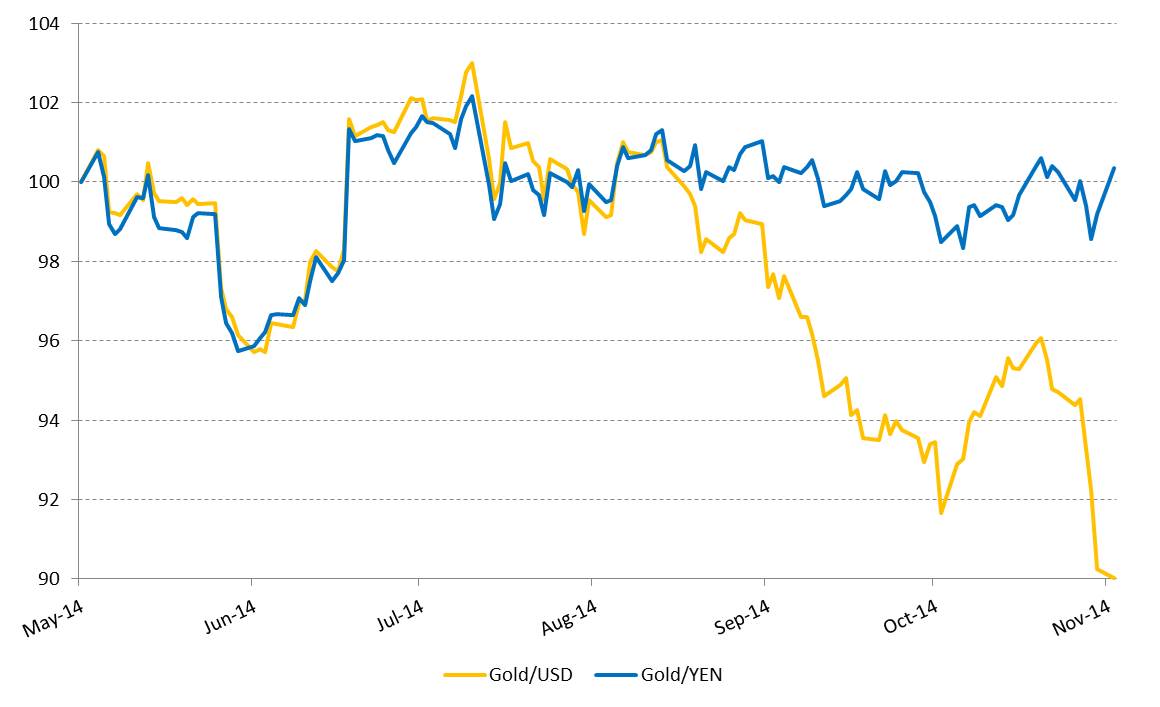

Since the beginning of August there has been a striking divergence in the relative performance of gold priced in US dollars versus gold priced in yen. Gold in yen has outperformed its dollar cousin by just over 10% over a period of three months. In fact year-to-date gold priced in yen has returned +5.3% with a 10.7% annualized standard deviation while gold in dollars has returned -2.6% with a 12.5% annualized standard deviation. Notably the gold price in yen terms has been largely stable during the jump in volatility of the last month while the gold price in dollars has suffered a significant drop.

Source: Bloomberg LP; Treesdale Partners calculations | Past performance is not indicative of future results.

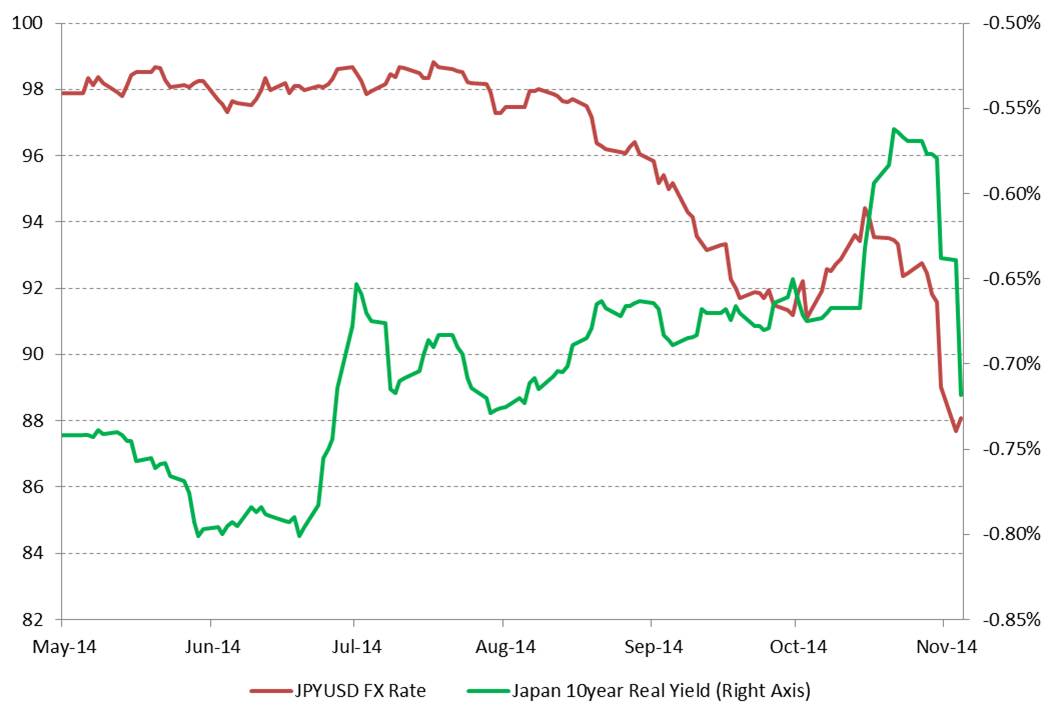

The primary factor driving this relative performance has been the strength of the dollar which put a large dent in the gold price in dollars but also significantly weakened the yen versus the dollar. In the chart below we chart the Yen/Dollar FX rate (on the left axis) and the 10 year Japanese real yield (on the right axis with an inverted scale). The strength in the dollar is clearly reflected in the FX performance with the yen weakening versus the dollar by over 11% over the same period. The resilience in the Gold price in yen terms was also strongly supported by the 10 year Japanese real yield (inflation-linked Japanese government bonds) which has fallen from a peak of -0.56% to the current -0.72% following the surprise announcement by the Bank of Japan to extend its asset purchase program.

Another notable factor supporting an investment in gold priced in yen terms is the positive carry that an investor can earn by financing their gold purchases in yen. The cost of carry of holding gold in yen is a function of the cost of holding gold in dollar terms plus the net cost of financing in yen and converting the proceeds into dollars.

Source: Bloomberg LP | Past performance is not indicative of future results.

Currently by financing gold purchases in yen an investor can earn a positive carry of approximately 0.42% on an annualized basis. Further it should be noted that the positive carry has been a consistent feature of holding gold in yen terms for the past year.

Looking forward we would expect the factors that have driven this dynamic in the gold price in yen terms relative to gold in dollars to be maintained and perhaps even strengthen. In particular, the large divergence in monetary policy between the US Federal Reserve which has recently ended its asset purchase program and the Japanese Bank of Japan which has dramatically extended its program, would be expected to persist and perhaps increase into the foreseeable future.

The message here for investors that wish to maintain an allocation to gold in the face of a resurgent dollar is that the choice of financing currency is of crucial importance. While past performance is certainly no guarantee of how the future will unfold, investors buying gold in yen terms have been able to find some calm in the face of a gathering storm.