Portfolio Effects of Holding Gold in Yen Terms

Treesdale Partners, portfolio manager of the AdvisorShares Gartman Gold/Euro ETF (GEUR), AdvisorShares Gartman Gold/British Pound ETF (GGBP), AdvisorShares Gartman Gold/Yen ETF (GYEN) and AdvisorShares International Gold ETF (GLDE), share their thoughts about the gold space.

Last week in “Gold in Yen – Calm in the Eye if the Storm” we focused on the factors behind the significant outperformance of gold priced in yen versus gold priced in dollars, identifying the strength of the dollar as the primary factor pushing down the price of gold in dollars. While on the currency side, the strength of dollar resulted in significant weakness in the YEN/USD FX rate.

Source: Bloomberg LP; Treesdale Partners calculations; past performance is no guarantee of future performance

This week we consider briefly the impact on portfolio efficiency that an investor would have experienced from holding gold priced in yen versus gold priced in dollars. This should be of interest to investors in the event that the current macro-economic dynamic of a stronger dollar and weaker yen, driven by the large divergence in monetary policy between the US and Japan, persists into the medium to long-term.

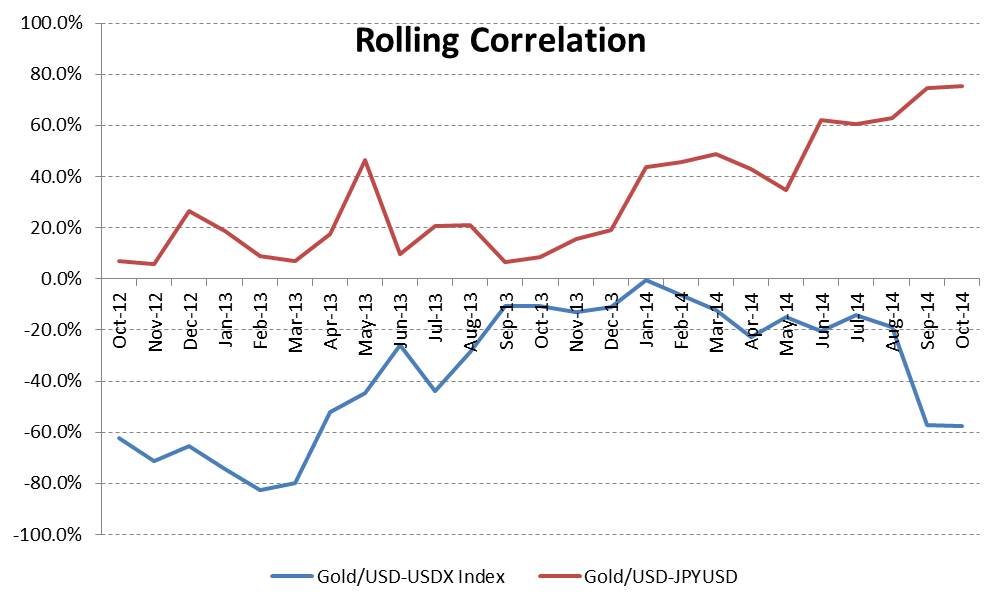

In the chart above we attempt to explain some of the outperformance of gold priced in yen by plotting the realized correlation between the price of gold in dollars and the USDX dollar index (a measure of the value of the dollar on FX markets) and the realized correlation between the gold price in dollars and YEN/USD FX rate. We see that the current market has been characterized by a strongly negative and falling correlation between gold and the USDX (-60%) and a strongly positive and rising correlation between gold and the YEN/USD FX rate (+75%). This suggests a strong three way relationship whereby as the dollar strengthened on currency markets the price of gold in dollars weakened but the strength in the dollar also impacted the yen with the weakening versus the dollar even as the gold price fell. In practical terms for an investor that held gold in yen, this has meant that although the strength in the dollar pushed down the price of gold in dollars, the yen financing position acted as an effective offset as the yen weakened mirroring the dollar strength – in effect the negative performance of gold in dollars was largely offset by the positive performance of the dollar versus the yen. In terms of actual performance numbers over the last three months the gold price in dollars has fallen 11.3% but the YEN/USD FX rate has also fallen by 11.7% so that on a net basis an investor holding gold financed in yen has experienced a net gain of +0.4%. In short while the gold price in dollars has experienced a steep decline over the last three months the gold price in yen has been essentially unchanged.

Source: Bloomberg LP; Treesdale Partners calculations; past performance is no guarantee of future performance

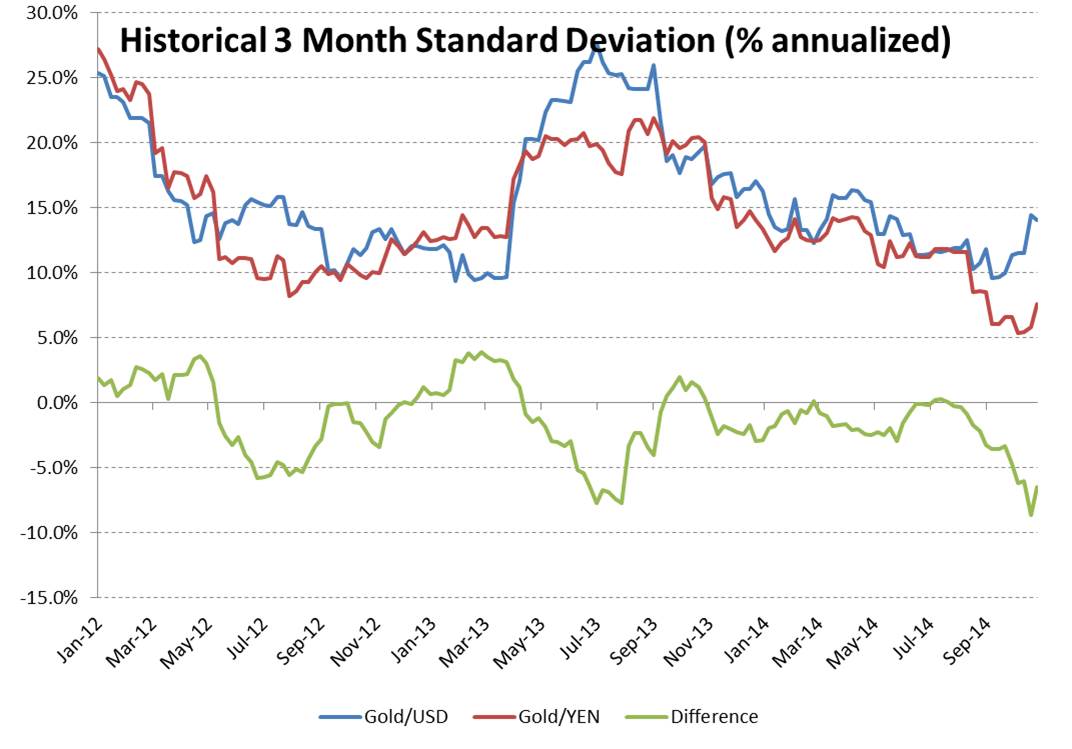

The other way in which these correlations have impacted portfolio efficiency is through their effect on the realized volatility (standard deviation) of the gold price in yen versus the gold price in dollars. As might be expected, the divergence in performance between the two prices has resulted in a large fall in the standard deviation of gold in yen relative to the standard deviation of gold in dollars. The second chart above plots the rolling three month standard deviation of both and shows that the difference in variability of gold in yen terms versus gold in dollars is at near term lows of -7%.

In summary the two charts above should help to demonstrate how the strong trend in correlation between gold and the dollar and gold and the yen have driven the outperformance of gold in yen versus gold in dollars while at the same time resulting in lower realized volatility for the investor.