Economic Data Continues to Impress, Driving Equities Higher

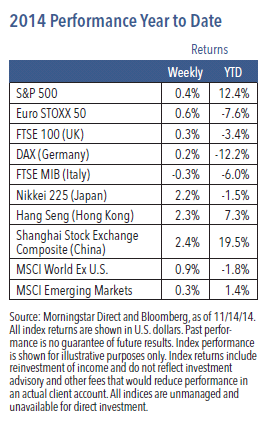

Once again, a combination of solid economic data, decent earnings results and receding fears of global deflation pushed stock prices higher. The S&P 500 Index rose for a fourth consecutive week, gaining 0.4%.1 The telecommunications and technology sectors showed particular strength while utilities and energy lagged.1

Lower Oil Prices Present More Benefits Than Risks

One of the biggest financial stories over the past several months has been falling oil prices. Brent crude prices were down over 5% last week while West Texas Intermediate prices fell almost 4%.1

Falling oil and commodity prices have stoked global deflation fears and are putting pressure on energy producers (including the U.S. energy industry). Ultimately, however, we believe that falling oil and commodity prices are mostly positive for the global economy. Lower prices are boosting consumer spending, and at the end of the day we believe falling oil and commodity prices will prove to be reflationary rather than deflationary.

Weekly Top Themes

1. We expect consumer spending will continue to rise. Retail sales for October rose 0.3% and were better than expected.2 Looking ahead, we believe the combination of an improving labor market, low inflation and falling energy prices should support additional spending increases.

2. Those same factors are strengthening consumer confidence. The preliminary November reading of the University of Michigan/Thomson Reuters consumer sentiment index was 89.4, its highest level since the middle of 2007.3

3. Growth outside the United States continues to struggle, with the eurozone economy only growing 0.6% in the third quarter.4

4. Investors may be overly complacent about the timing for the first Federal Reserve rake hike. Although most anticipate the Fed will not begin increasing rates until the middle of 2015, falling unemployment and signs that wages may be starting to climb could prompt the central bank to act earlier.

5. Political gridlock remains the norm in the aftermath of the U.S. mid-terms. The current hot topic is immigration reform, with President Obama indicating he may take executive action as early as this week and Republicans warning that such a move could jeopardize the potential for future cooperation.

An Improving U.S. Economy Should Boost Global Growth and Equity Prices

We are one month past the 10% correction that occurred from mid-September to mid-October. In retrospect, that setback appears to have been just a brief and temporary interruption in the midst of an ongoing bull market. Markets have since recovered and have been posting new highs, yet investors remain on edge and appear concerned about the state of the economy, geopolitical uncertainties and lingering deflation threats, particularly in Europe.

Our take is that U.S. economic growth is set to improve. Lower levels of government spending over the past couple of years have been a modest headwind, but we expect spending levels to rise somewhat. More important, private sector growth has been solid and is improving. At this point, we are forecasting that gross domestic product should expand by an average of 3% over the coming quarters. This is hardly the fastest pace we’ve seen over the last several decades, but it does represent a higher gear than what the United States has experienced since the Great Recession ended.

This level of growth should be enough to provide a lift to the broader global economy. It should also be strong enough to support continued growth in corporate earnings, which, in turn, should provide a tailwind to equity prices. We expect volatility to continue and remain on the watch for risks that could result in another pullback in prices (for example, the timing of the Fed’s decision to enact its first rate hike). Over the long term, however, we are retaining our positive view toward most risk assets, including equities.

1 Source: Morningstar Direct and Bloomberg, as of 11/14/14 2 Source: U.S. Department of Commerce 3 The University of Michigan/Thomson Reuters 4 Source: Eurostat

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2014 Nuveen Investments, Inc. All rights reserved.

GPE-BDCOMM3-1114P 4537-INV-W11/15