By John Del Vecchio, CFA, portfolio manager of Ranger Alternative Management and AdvisorShares Ranger Equity Bear ETF (HDGE)

The price / sales ratio is often used as a valuation metric in the place of earnings because of the common belief that revenues are harder to manipulate than earnings. In my book, What’s Behind the Numbers? (McGraw-Hill, 2012), I debunk that theory and outline many ways that management teams can aggressively manage the top-line. Nevertheless, the price / sales ratio is useful because there are fewer inputs, such as reserves, tax issues, share buybacks, and recurring charges, than earnings that can be used to manage the reported results.

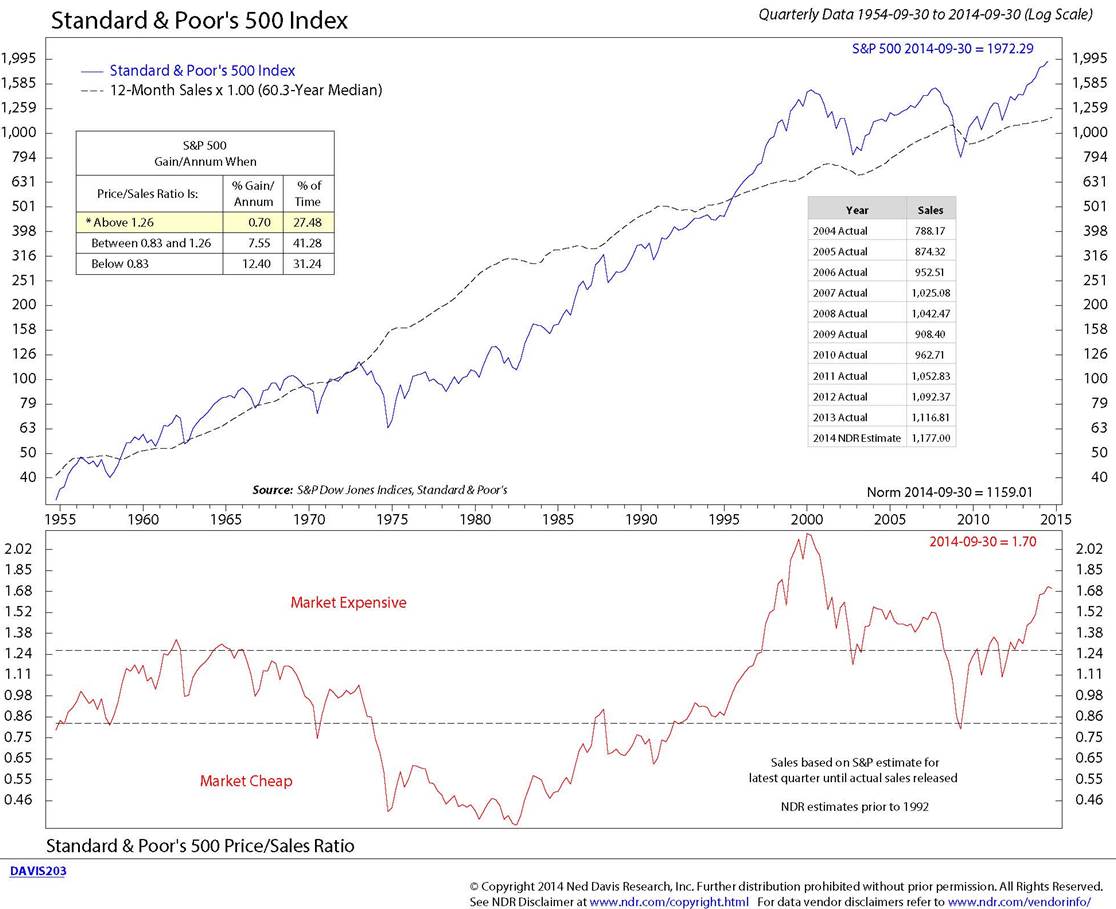

Not only is the price / sales ratio useful for individual stocks, but also for the market as a whole. At the end of the third quarter of 2014, the price / sales ratio on the S&P 500 stood at 1.70x. This is exceedingly high and is flashing a bright red warning sign for the broader market. As you can see in the chart below, according to Ned Davis Research, that level is only breached 27% of the time with an annual gain of just 70 bps.

What I find particularly interesting is that the level of the price / sales ratio is well outside normal bounds going back to the 1950’s. Yes, it’s lower than 2000, but there are significant differences between the market today and back in 2000. For example, technology companies dominated the S&P 500 at the end of the last century. Those companies often had significant multiples relative to their revenues as investors bid up shares in anticipation of the growth of Internet commerce, networking, and software applications. Because the S&P 500 is a market capitalization weighted index, as those companies became larger, they skewed the price / sales ratio higher. As the bubble burst, we all know what the fallout was. In my mind it was an aberration.

What’s different today, compared with 2000 is that the overall market is much more overvalued. There is no one sector completely dominating the stock market. The overvaluation is much broader. It’s also higher than during the Financial Bubble of 2005-07. While one could have gained relative performance on the long side by avoiding technology stocks in 2000-02 of financial stocks in 2007-08, there’s little to know opportunity to do so today. What the price / sales ratio is telling you today is that everything is richly priced, and at level unlike anything is the last 60 years.

This presents a big risk because when the market trend turns to the downside; there will be nowhere to hide.