The U.S. labor market data has improved in the last six months now that many measures have reached cyclical highs. For the Federal Reserve though, this is not enough. They want to see this data feed through to a broader rise in incomes and wages, and ultimately spending. This will be necessary to bend the economic trajectory toward sustainably higher growth. Many statistics indicate that we may be on the cusp of stronger gains in wages. It is clear the output gap is now much narrower, and that excessive labor market slack has dissipated with the unemployment rate at 5.8%, the underemployment rate at a cycle low of 11.5%, and the employment to population ratio at 59.2%, the best since the recession ended. The share of job creation in lower-wage industries or part-time jobs has lessened this year, which is also encouraging. However, progress on wages has been scattered, frustratingly slow, and difficult to assess—many measures display only tentative or unconvincing trends. Furthermore, it is unclear if the recent nudge in select data is due to less slack (a more persistent source of wage pressures) or government-related measures to support worker income and benefits such as minimum wage hikes.

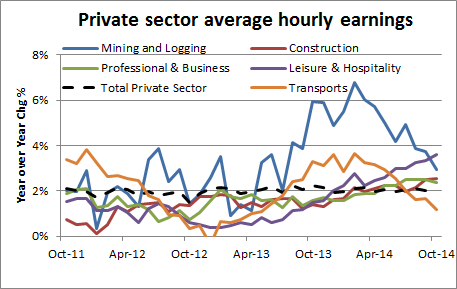

Normally, as slack in the labor market diminishes, workers should have more negotiating power on wages. The Yellen Fed has focused on average hourly earnings in the total private sector to gauge progress in hourly pay per worker. This narrower metric has remained static growing at a very flat 2% annual gain, although there have been shifts in underlying industries beneath the surface. Occupations with some scarcity of qualified labor have seen some wage pressures, such as transportation, construction and mining. However, the gains look more one-time, with advances in 2013 now slowing in both mining and transportation. Leisure/hospitality’ continued wage gains are likely related to higher minimum wages recently enacted in some states (and less to increasing demand for these workers). This sector has the most meagre level of wages in the private sector at $14 per hour (up 50 cents p/h in a year). The faster gains there are probably one-time as well and mainly on a state-by-state basis. Focusing only on production and non-supervisory jobs in these industries shows little differences too. While the faster overall annual rise of 2.2% is encouraging, most sectors are decelerating with only construction and leisure/hospitality sectors seeing a pickup—again likely due to one-time minimum wage hikes.

The broadest measure of compensation is the Employment Cost Index, a much more comprehensive measure that includes wages, bonuses and employer-provided monetary benefits like health insurance; it also covers both hourly and salaried workers. This data reflects a very recent pickup in both wages and benefits with total compensation rising 2.3%, the highest since late 2008, up from about 2% in the last few years. However, this is still much lower than the average gains of 3-4% gains seen in 2000 – 2007.

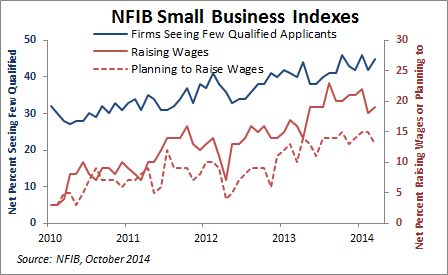

Survey data from small businesses does show a rising percentage of employers increasing wages and greater intentions to do so in the future. While minimum wage impacts have been noted, some of this may be associated with the poor quality of candidates they also cite as a factor in their hiring and staffing decisions. Many of these businesses point to poor communication skills and poor appearance as issues that reduce the pool of qualified labor applicants. As a result, they are willing to increase pay to hire candidates with desired qualifications and also to keep their current staff satisfied. While this is not considered hard data, it does correlate well with rising wages after some lag.

Faster job gains are important, but this only raises the aggregate level of income, and therefore the aggregate level of spending, to a modest degree. A more spirited pickup in overall wage growth is the key to a more sustained pickup in consumption and economic growth. While the data supports some firming in wage growth in the period ahead, it also does not point to much wage inflation either. This may be the best of both worlds for the Fed, and they will likely cheer—and not worry about—any assist from rising wages.

Disclosure

The views expressed are as of 11/17/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

1062246