The S&P 500 Index hit another set of fresh record highs last week (November 10 – 14, 2014) and has achieved the midpoint of our total return forecast (10 –15%) for the year with a 12% return year to date. While we continue to recommend keeping the majority of equity allocations in the United States, as we have for a while, we think it is a good time to look at opportunities that have lagged behind the strong U.S. stock market and may have become attractively valued, possibly setting the stage for a reversal. One such area is emerging markets (EM).

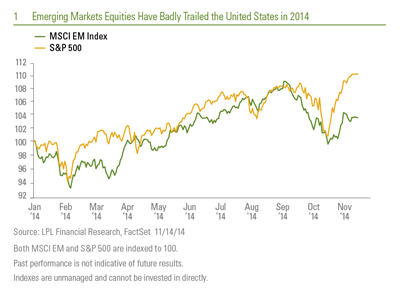

It has been another tough year for EM equities. The MSCI EM Index has returned just 1.4% year to date, far behind the S&P 500 (though MSCI EM Index has outpaced the developed foreign benchmark, the MSCI EAFE Index, which has returned -2.6% year to date) [Figure 1]. EM have struggled for many reasons, including but not limited to lackluster earnings, Federal Reserve (Fed) tapering and the subsequent end of quantitative easing (QE), related concerns about current account deficits due to trade imbalances and borrowing abroad, geopolitical unrest in Ukraine and the Middle East, the drop in commodity prices, a strong U.S. dollar, and growth fears in Europe and China. So with all of those challenges facing investors, is it time to buy EM? To answer that question, let’s look at fundamentals, valuations, and technicals.

Mixed Fundamentals but Poised to Improve

We believe emerging markets fundamental conditions — though somewhat mixed currently — may show improvement in 2015. Key elements to this assessment include our outlooks for economic growth, earnings, and policy:

- Slower growth still outpacing developed world; could pick up in 2015. Growth has slowed significantly in EM countries in aggregate over the past several years, led by the substantial slowdown in China. After growing gross domestic product (GDP) at roughly 8% in 2010, EM economic growth has averaged only about half that amount, or 4%, since 2012, still well above the sub-2% growth for the developed markets overall this year [Figure 2]. But as we discussed in our October 31, 2014, Weekly Economic Commentary, “Gauging Global Growth in 2014 & 2015,” emerging markets overall are expected to grow GDP a bit faster in 2015. Slightly better U.S. growth may help, although Europe (an even bigger export partner for EM) remains a wildcard. The Bloomberg-tracked consensus is currently calling for only a marginal improvement to 4.5% GDP growth in 2015, while the International Monetary Fund (IMF) expects EM growth to improve more substantially, by about a half percent to 4.9%.

- Muddled corporate earnings picture. EM earnings are not faring nearly as well as the United States. For the just completed third quarter of 2014, earnings for the MSCI EM Index are tracking to a 4.2% decline (about 70% of the index constituents have reported). The unexpected drop was driven mostly by the natural resources sectors due to falling commodity prices, which hit resource-producing countries such as Russia and Brazil particularly hard.

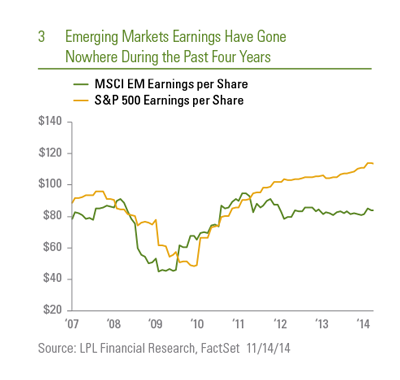

The earnings struggle in EM is perhaps more apparent when looking at a longer-term performance. Thanks to a series of missed expectations related to slower growth in key EM export markets, periods of tightening financial conditions, falling commodity prices, and in some cases inefficient government policies, EM earnings have essentially not grown at all since 2010. Meanwhile, during this time U.S. earnings have continued to power ahead [Figure 3].

Looking ahead, better global growth, particularly in the United States, and weaker currencies may help support EM exports and give earnings a boost in the coming quarters. And earnings for commodity companies may be poised for a rebound if commodity prices can stabilize (particularly oil), as we generally expect, based on our expectation for a supply response at lower prices. Risks to earnings include further reductions in economic growth forecasts and continued declines in commodity prices.

- Policy actions starting to help. The Fed has reined in stimulus by ending its QE program. However, we expect the European Central Bank (ECB) will initiate its version of QE in the coming months in an attempt to try to stimulate growth in Europe. We also expect Japan to continue its bold stimulus plan, and Chinese authorities have recently enacted targeted monetary policy stimulus. China has also taken steps to encourage small business lending and taken other targeted fiscal and administrative actions aimed at stabilizing its economy. India’s stock market has surged this year, following the election of Prime Minister Modi, and economic reforms and easing inflation pressures from lower oil prices are likely to improve the country’s finances and continue to encourage foreign investment. Mexico is beginning to reform its energy sector, opening it up to foreign investment to increase productivity.

Brazil seems to be lagging behind, but its lack of progress on the policy front likely sets the market’s bar low for improvement in 2015. Russia, while still a big question mark due to economic sanctions over the Ukraine conflict, is unlikely to derail EM. While there are surely policy risks across the EM landscape and patience may be required, in general we expect the policy environment in 2015 to be more supportive.

The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings

The Best Reason to Like EM: Valuations

The strongest reason to consider EM equities is valuation. On an absolute basis, the MSCI EM Index is trading at a forward price-to-earnings ratio (PE) of just 10.9 times, attractive given that the index has only been below 11 about one-third of the time since 1988, and earnings are expected to grow by mid- to high single digits over the next year (according to Thomson Reuters consensus data). On a relative basis, the MSCI EM Index PE trades at a 31% discount to the S&P 500, compared with an average discount of 21% over the past 20 years [Figure 4]. Developed foreign valuations (based on the MSCI EAFE Index) are also relatively low, though we find EM to be a more attractive international option. While valuation is clearly a positive, keep in mind these valuations are based on forward earnings estimates that may not be realized.

Forward price-to-earnings is a measure of the price-to-earnings ratio (PE) using forecasted earnings for the PE calculation. The earnings used are just an estimate and are not as reliable as current earnings data. Forward price-to-earnings ratio is based on earnings over the next four quarters.

Technicals Suggest Caution but a Potential Opportunity

Our technical analysis is signaling a cautious approach to EM, but the magnitude of the underperformance highlights the size of the potential opportunity. The MSCI EM Index is exhibiting negative momentum, having broken below its 200-day simple moving average while significantly underperforming the S&P 500 over the past year (moving averages are a way to measure price trend for a particular investment to determine momentum). But the MSCI EM Index is oversold based on the 14-day relative strength index (RSI), a measure of relative upside and downside performance (over

the past 14 trading days on a 0 – 100 scale), and performance relative to the S&P 500 has reached extremes that suggest it may be due for a reversal [Figures 5, 6].

Figure 5 shows the MSCI EM Index has fallen below the widely followed 50-, 100-, and 200-day moving averages, indicating downward momentum. The figure also shows that the RSI (14) indicator has fallen below 30, into what we consider to be oversold territory. This measure indicates a high percentage of down days relative to the number of up days during the past 14 trading days.

Looking longer term, the magnitude of EM underperformance over the past four years at more than 80% (as of November 14, 2014) suggests a potential mean reversion opportunity. So from a technical perspective, while EM have clearly struggled to gain and sustain performance momentum, the possibility of a short-term technical rebound and the potential to recapture some of the longer-term relative losses versus the U.S. stock market suggest a potential opportunity. This may be a case of high risk, high potential reward, although valuations suggest a cushion against downside risk in the longer term.

Favor Emerging Asia over Latin America or Emerging Europe

Emerging Asia is experiencing stronger economic and earnings growth than Latin America and the broad EM universe. Asia is also in a position to benefit from lower oil prices, as opposed to Brazil, Russia, Mexico, and other EM countries that depend heavily on natural resources activities. Finally, Asia, in general, has better current account situations and is therefore better able to withstand reduced stimulus from the United States. For example, China, the Philippines, Korea, Taiwan, and Malaysia all run current account surpluses while Brazil, Mexico, Peru, and Colombia all run current account deficits.

EM Opportunity Still Emerging

EM weakness may present an opportunity here. Valuations are compelling and EM may be situated to recapture some relative losses from a technical perspective, particularly in Asian markets. However, somewhat mixed fundamental and technical pictures suggest a better opportunity may be forthcoming. We continue to watch for evidence of a turn in performance, which may come with better earnings and stable oil prices, to consider a more positive view. At this point, the EM opportunity — while intriguing — is still emerging, and we maintain our preference for the United States.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1-329452 (Exp. 11/15)