Powerful, Nearly Six-Year-Old Bull Market Should Continue

We believe stocks will deliver mid- to high-single-digit returns in 2015, with a focus on earnings over valuations. We believe 3% economic growth, benign global monetary policy, and a more favorable policy climate from Washington indicate that the powerful, nearly six-year-old bull market should continue.

Historically since WWII, the average annual gain on stocks has been 7–9%. Thus, our forecast is in-line with average stock market growth. We forecast a 5 – 9% gain, including dividends, for U.S. stocks in 2015 as measured by the S&P 500. This gain is derived from earnings per share (EPS) for S&P 500 companies growing 5 – 10%. Earnings gains are supported by our expectation of improved global economic growth and stable profit margins in 2015. We expect stocks, not bonds, to be the precious cargo for investors in 2015.

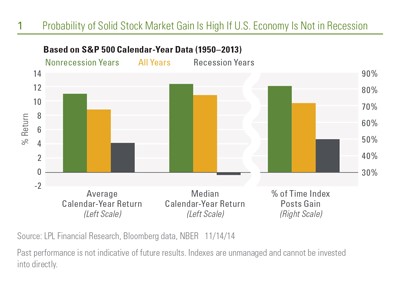

The coming year will be one marked by transitions. Cycles that are in transition can cause potential fluctuations and volatility even if they have historically provided solid stock market performance. The most important cycle, the economic cycle, is unlikely to reach a recession destination in 2015, positioning the stock market to potentially offer up solid gains to investors. In fact, since 1950, in years during which the U.S. economy does not enter recession, the odds of a positive year for the S&P 500 were 82%, with an average gain of 11%. Recessions do not run on a set schedule and are difficult to pinpoint in advance, but our belief, based on our favorite leading indicators for the economy, is that the probability of recession is very low and stocks could potentially send investors solid returns in the coming year [Figure 1].

Earnings Should Do the Heavy Lifting

We expect earnings, and not valuations, to do the heavy lifting in producing potential stock market gains for investors in 2015. Steady, though not spectacular, economic growth in the United States and mixed, but largely stable, growth overseas may support continued low- to mid-single-digit revenue growth for the S&P 500. As the economic cycle advances further, cost pressures may begin to emerge and limit companies’ ability to expand profit margins. However, with limited wage pressures, currently low commodity prices (for non-commodity producers), and low borrowing costs, profit margins should remain relatively stable. In addition, share buybacks by corporations — though slowing — may continue to lift the EPS calculation. Based on this, we believe the S&P 500 is on schedule to potentially deliver a year of high-single-digit EPS growth.

Monetary Policy in Transit As Fed Policy Shifts

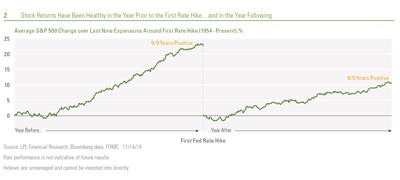

Monetary policy is in transit in 2015, when stocks will face a transition from the very loose monetary policy of the Fed’s quantitative easing (QE) program, which ended in October 2014, to an environment in which the Fed begins to hike interest rates. Although this transition may contribute to an increase in stock market volatility in the short term, we do not expect the start of Fed rate hikes to derail the stock market in 2015. In fact, history has shown that stocks performed well when the Fed began to hike interest rates, due to the better economic and profit growth that prompted the Fed to act to combat inflation [Figure 2]. Over the past 50 years, the first hike has tended to occur a bit before the halfway point of economic cycles and well before bull markets have ended.

Weighing the Risks: This Bull Market Has Not Yet Reached Its Final Destination

Despite the favorable backdrop of improving economic growth and attractive corporate fundamentals, meaningful risks remain for stocks in 2015. The Eurozone, which is teetering on the brink of another recession, and the possibility of a further slowdown in China, both present risks to global growth. Structural constraints may also slow Europe’s return to reasonable growth levels.

Geopolitical risks, such as the Russia-Ukraine conflict and the rise of Islamic State militants, remain on investors’ minds as potential risks that could drive increased volatility during 2015, as they did at times during 2014. Last, the possibility exists that a policy mistake in Washington — such as another debt ceiling debacle — could take stocks off schedule, though even with a Republican-controlled Congress and Democratic president we see that possibility as quite remote.

Weighing Value

Valuations for the S&P 500 remain slightly above the long-term average price-to-earnings ratio (PE) of between 16 and 17 times trailing earnings, indicating a slightly expensive market. However, valuations have had virtually no predictive power in timing market tops or major pullbacks. But over long time periods, such as over the next 10 years, PE ratios have a strong historical record of forecasting the market’s direction [Figure 3]. Important to note, even when valuations indicate performance below the historical averages, they rarely point to negative returns. Thus, while valuations are the single most important long-term factor affecting stock prices, in the short term, they are much less impactful.

Valuations can tell you when the market has become fully priced and may be more vulnerable to any deterioration in the economic cycle; but we do not view slightly above-average valuations as a risk to continued stock market gains in 2015. Our expectations that stock market returns track mid- to high-single-digit earnings growth suggest valuations are less likely to get out of hand.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1-332621 (Exp. 12/15