Overseas, policies already in place -- and those that we expect to be enacted over the course of 2015 -- are likely to be big drivers of global growth. We expect the U.S. economy will expand at a rate of 3% or slightly higher in 2015, which matches the average growth rate over the past 50 years. This forecast is based on contributions from consumer spending, business capital spending, and housing, which are poised to advance at historically average or better growth rates in 2015. Net exports and the government sector should trail behind. As the economy continues to grow at a moderate pace in 2015, we expect this expansion to potentially take us into 2016, where we could likely find tightening labor market conditions and a rising fed funds rate.

This week’s commentary features content from LPL Financial Research’s Outlook 2015: In Transit.

The United States is in the middle stage of the economic expansion, presenting investment opportunities and risks for investors. While the U.S. economy has grown over time, the growth has not been in a straight line. The variations in the pace of growth around the long-term trend are called economic cycles. Economic cycles have four distinct stages: recession, early (recovery), middle (mature), and late (aging).

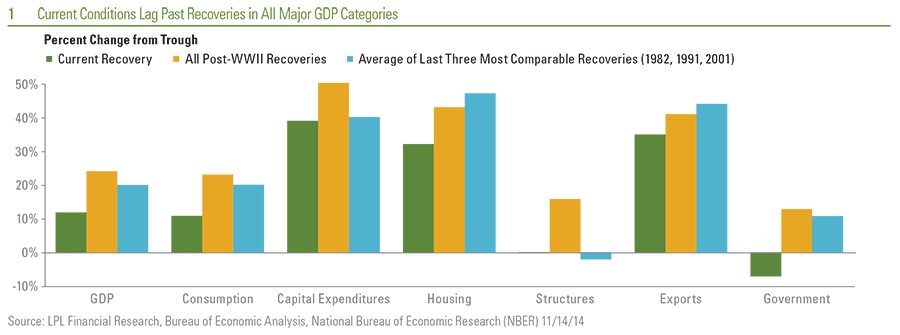

By historical standards, the economic recovery that began in mid-2009 has been by far the most tepid recovery on record, with GDP through third quarter 2014 just 11% above its 2009 trough. In all recoveries since the end of World War II (WWII), the economy expanded 24% on average in the first five years of recovery. The current recovery even lags the last three (beginning in 1982, 1991, and 2001), which we believe are the most comparable. Five years into those recoveries, the economy stood 16% above its recession lows. The pace of this recovery thus far has lagged behind those prior in each of the major GDP categories [Figure 1].

The Upside to a Slower Pace

Although the weak pace of this recovery has been frustrating for both the public and policymakers alike, there have been several silver linings. The lackluster expansion has put downward pressure on hiring, wages, and in turn, inflation, as the economy continues to operate well below its long-term potential growth rate. The lack of inflation has allowed the Federal Reserve (Fed) to be patient in its journey toward removing the massive amount of stimulus it has added to the economy since 2008; but another solid year of economic growth in 2015 could tighten labor market conditions and likely begin to drive wages higher. This transition from a subpar recovery to a more normal recovery in 2015 is likely to convince the Fed -- which ended its quantitative easing (QE) program on schedule in October 2014 -- that the economy has made enough progress to start normalizing policy. In the latter half of 2015 or early 2016, the Fed may begin slowly raising its fed funds rate target, starting the long journey back to more normal, and higher, rates. Importantly, the start of Fed rate hikes does not signal the end of economic expansions. Indeed, since 1950, the start of Fed rate hikes meant that the economy was roughly 40% through the expansion.

Tracking Our Progress Through the Expansion

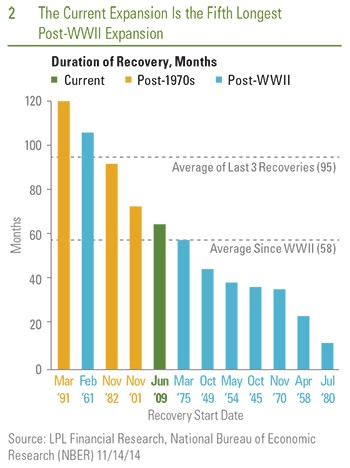

At 65 months (through the end of November 2014), the current recovery is the fifth-longest expansion since World War II, and is already longer than the average economic recovery since that time (58 months).* Looking back over just the past 50 years, the average expansion has been 71 months. On that basis, the current recovery may surpass the average in the middle of 2016 [Figure 2]. On average, the last three expansions -- the ones that began in 1982, 1991, and 2001 -- lasted 95 months. Using those three expansions as the standard, the current economic expansion still has the legs to potentially deliver growth for the next couple of years. This economic expansion is likely entering its latter half, which is marked by strong economic growth but also the potential for rising inflation, accelerating wage growth, and eventual Fed rate hikes. All expansions come to an end, but 2015 does not appear to be the final destination for this current economic recovery.

*According to the National Bureau of Economic Research, the nonpartisan think tank that determines business cycle start and end dates.

Labor Market Likely to Build on 2014 Improvement

The labor market is a lagging indicator of overall economic activity. The current economic expansion began in June 2009, but the private sector economy did not regularly begin creating jobs until early 2010. Since then, the economy has added 10.3 million jobs, or just under 200,000 jobs per month. In the 12 months ending in October 2014, the economy created nearly 220,000 jobs per month, despite a run of harsh winter weather that held down job growth in late 2013 and early 2014. Looking ahead to 2015, if GDP growth achieves our 3% forecast, the economy should routinely create between 200,000 and 250,000 jobs per month, as it has during the middle of every business cycle over the past 30 years when economic growth was between 3% and 4%.

Labor market indicators are making progress, but most have not yet reached their destination. Please see our Tracking Yellen’s Indicators infographic in our Outlook 2015 publication.

Overseas Markets to Move Toward Stability in 2015

Overseas, policies already in place -- and those that we expect to be enacted over the course of 2015 -- are likely to be big drivers of global growth, impacting most of the world’s largest economies outside of the United States. The Eurozone has endured two recessions since 2007, and its fractured financial system continues to cause a delay in its long-overdue return to growth. However, actions taken by the European Central Bank (ECB) in late 2014 may set the stage for a transition to a more stable environment. We expect the ECB will increase the pace of its QE program in 2015, and governments in the Eurozone will begin to finally loosen fiscal policy.

China’s economy is still in the midst of varied growth and a changing economy. From growing at a 10 - 12% rate in the early to late 2000s, China is currently growing at closer to 7%,** and its economy is more dependent on domestic consumption than trade and investment. China’s housing bubble deflated slowly over the course of 2014 and may continue to deflate in 2015 and beyond; the consequences of that deflation to the rest of the Chinese economy may continue to be felt in 2015, adding to economic and market volatility. With low inflation as well as massive currency and fiscal reserves, China has the ability to continue helping its economy shift. As it does so -- and as other reliant economies adjust to the transition -- it may cause an increased level of economic volatility across the globe.

*According to the National Bureau of Statistics of China.

Returns on investments in foreign securities could be more volatile than, or trail the returns on, investments in U.S. securities. Investments in securities issued by entities based outside the United States pose distinct risks, since political and economic events unique to a country or region will affect those markets and their issues.

Deflation is a prolonged period of falling prices and wages.

Japan’s economy has traveled in and out of recession, deflation, and depression for the better part of the past 25 years. Yet, bold actions by Japanese policymakers (fiscal and monetary) over the past several years could begin to transport Japan’s economy toward more fully contributing to global growth in 2015 and beyond. After announcing an expansion to its QE program at the end of October 2014, it is likely that the Bank of Japan will enact another round of QE in 2015, as it attempts to break the decades-long cycle of deflation. But the journey out of deflation cannot be made by monetary policy alone, and for Japan to add to global growth in 2015, coordination between the Japanese government and the Bank of Japan is critical.

We will continue to monitor current government policies around the world -- and those to come -- for their potential ramifications on the U.S. economy and global economic growth to look for signs that the global economic expansion remains on schedule.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Throughout this document, expansion and recovery are used interchangeably. For more detail on the economic cycle, please see our infographic on page 10 of the Mid-Year Outlook 2014.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking #1-332665 (Exp. 12/15)