Disclaimer

The information, tools and material presented herein are provided for informational purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments. This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. You should independently evaluate particular investments and consult an independent financial adviser before making any investments.

We review in details where we stand in terms of the US and World leading indicators and point to some of the unsettling recent developments which should be watched carefully over the coming months. Happy holidays and happy New Year!

The set of indicators we review comprises

- US shadow policy rate;

- US Treasury yield curve;

- US TIPS yield curve;

- Global business cycles interplay (OECD CLI);

- G7 growth and inflation (OECD MEI);

- World trade and industrial production;

- US conventional growth leading indicator;

- US coincident inflation indicator;

- US job creation;

- US growth and inflation based on Macro-Yield model, small and large datasets;

- US GDP-based leading indicator.

For the details on the methodology and explanations refer to the previous Commentaries.[1][2][3]

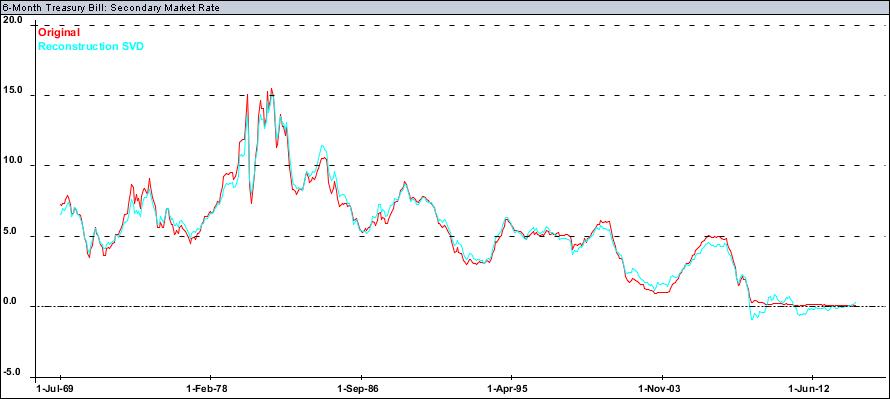

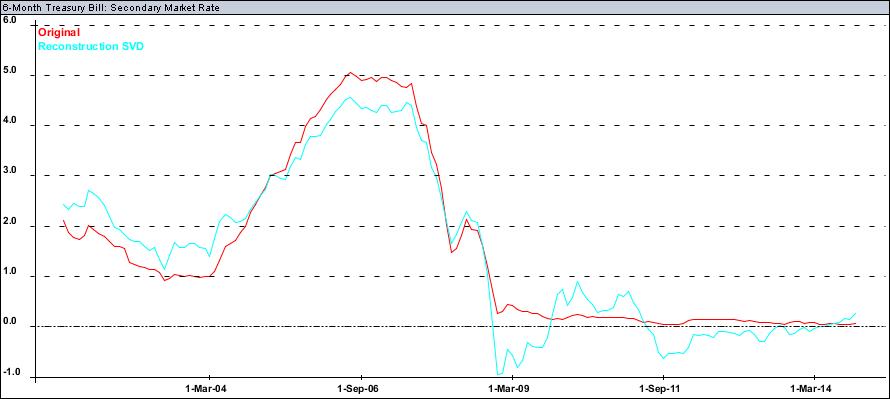

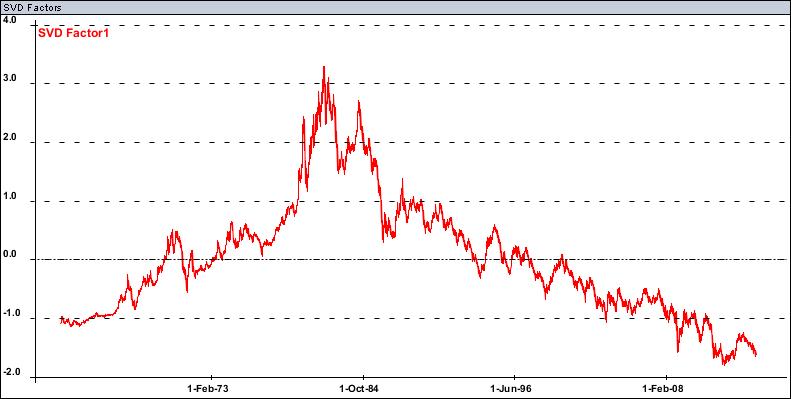

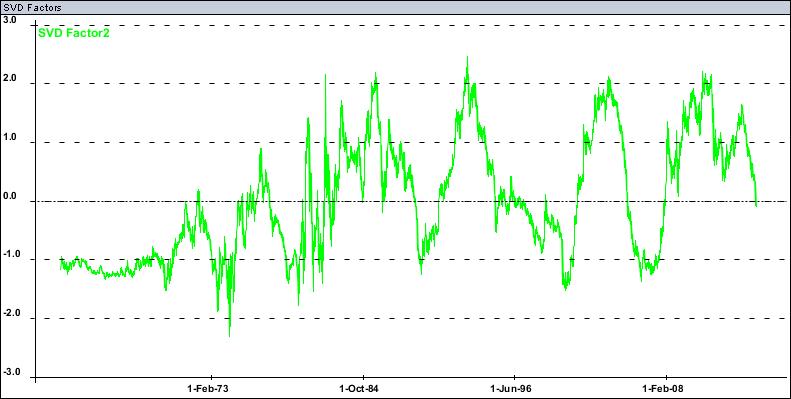

US shadow policy rate

We use the proprietary methodology to construct the shadow Fed Funds rate implied by other economic and financial information (methodology is similar to the recent BIS work[4]). Below the Fed Funds rate and its shadow reconstruction over the last 45 years are presented

Here is the more recent snapshot

As one can see the Fed has been effectively tightening since May 2013 Taper announcement with some recent acceleration.

US Treasury yield curve

As we cautioned in February 2014[5][6] the yield curve level is going down and the curve is flattening to the levels not seen since the Global Financial Crisis

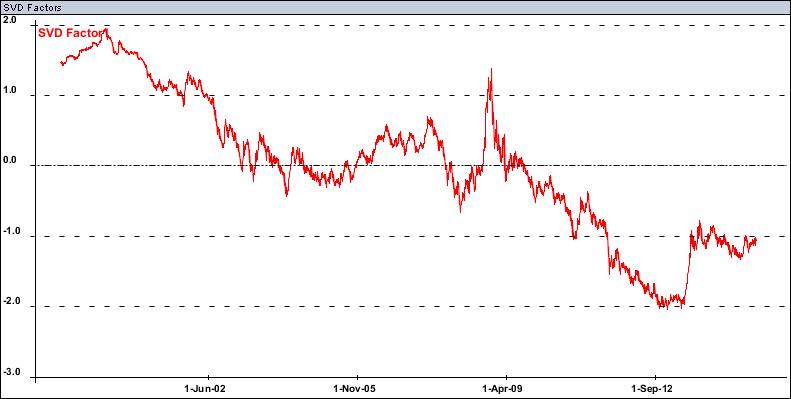

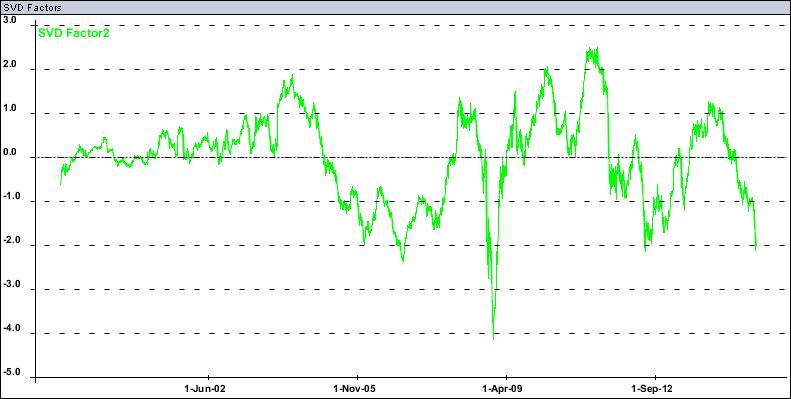

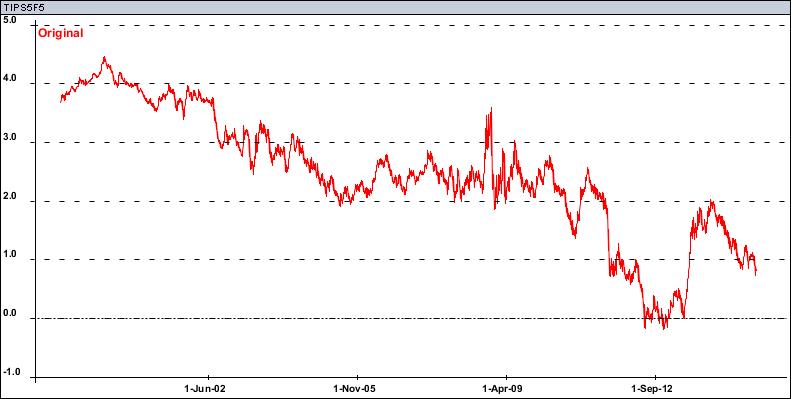

US TIPS yield curve

The level of the TIPS yield curve remained relatively flat post Taper Tantrum

but together with the Treasury yield curve the TIPS yield curve was flattening since December 2013 and reached some extreme historic flattening recently

This is of course also reflected in 5Y5Y forward rates

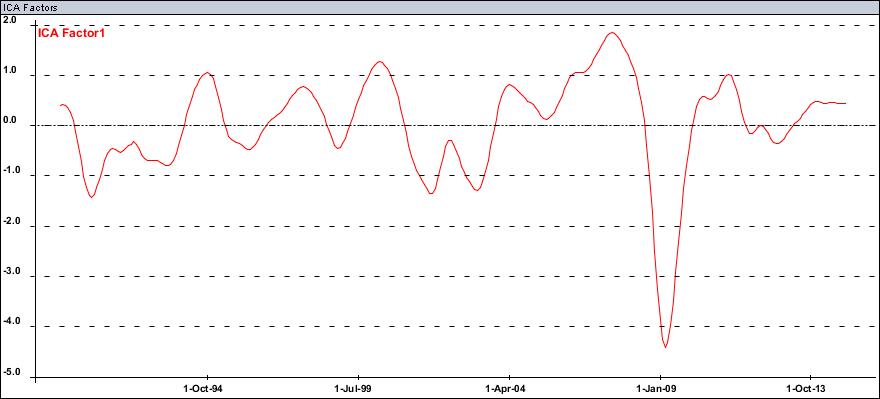

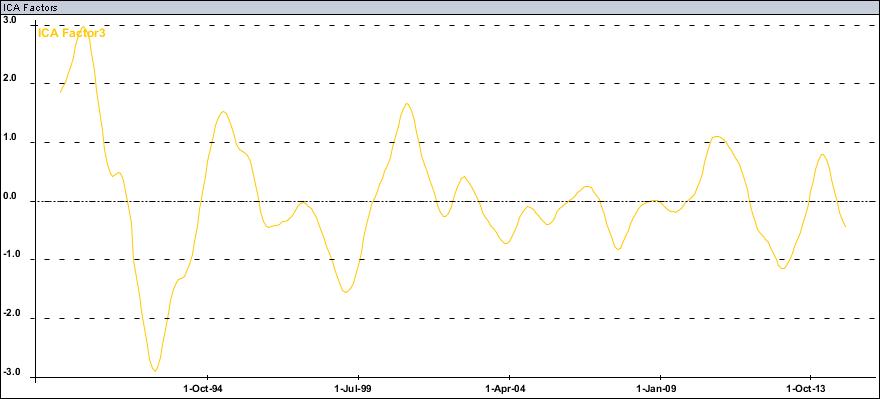

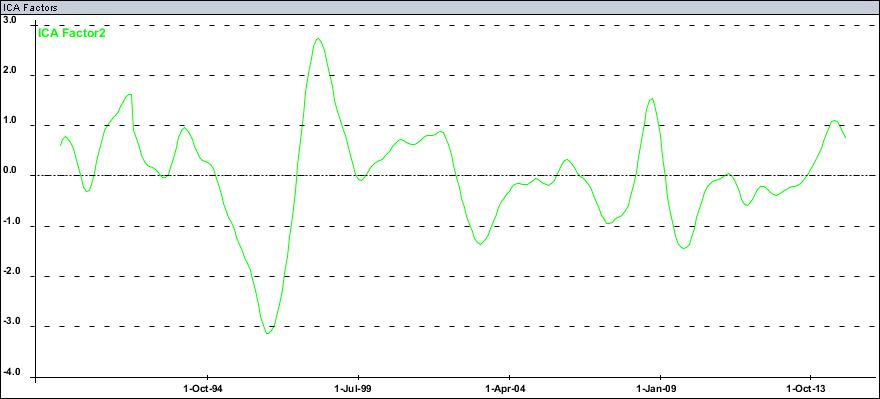

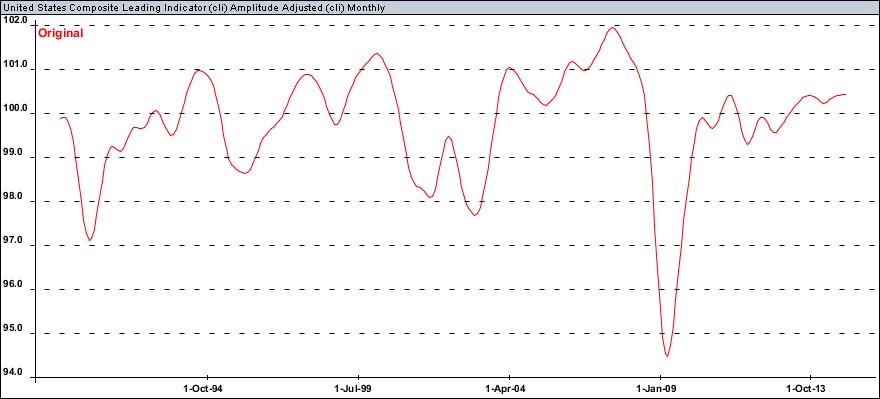

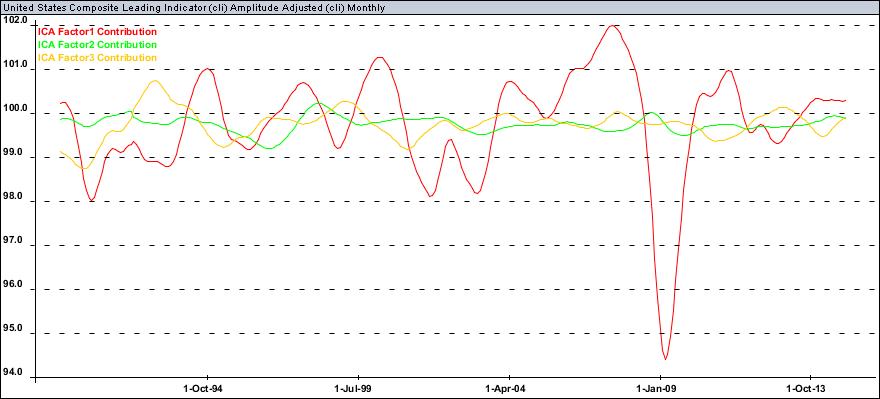

Global business cycles interplay (OECD CLI)

We use OECD CLI dataset (see the previous Dynamika Commentaries for explanation[7][8]).

Global Business Cycle Factor: what an unseen plateau! Where to now?

Europe Idiosyncratic Factor (outperformance of Europe versus Global Factor): Europe continues to underperform.

Asia Idiosyncratic Factor (underperformance of Asia versus Global Factor): China seems has turned the corner.

The US is the most interesting case as it seems to be doing well but for the wrong reasons.

Given recent plateau in the Global Factor the US was mostly uplifted by Europe deterioration and uplifted be recent asia deceleration. Here is how all three factors contributed to the US

You can see how the end of 2012 slowdown was avoided thanks to the uplifting Europe pain. Most recent European calamity also helps the US big time.

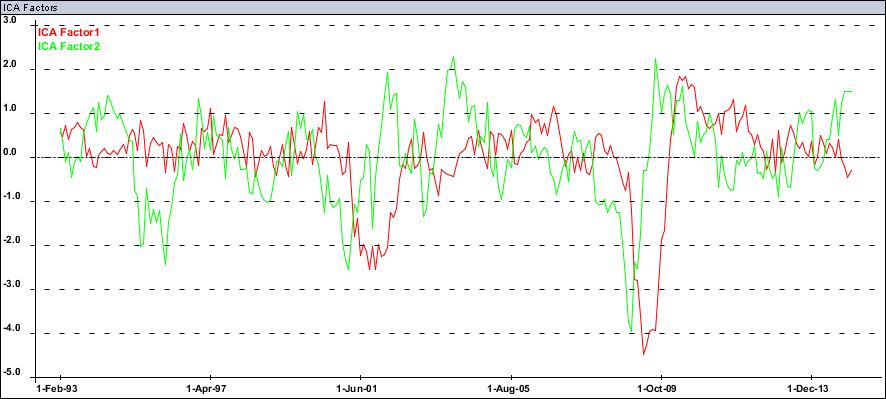

G7 growth and inflation (OECD MEI)

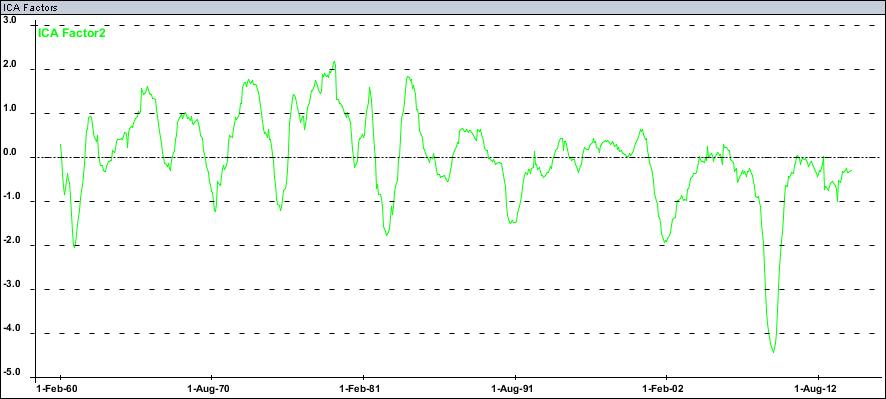

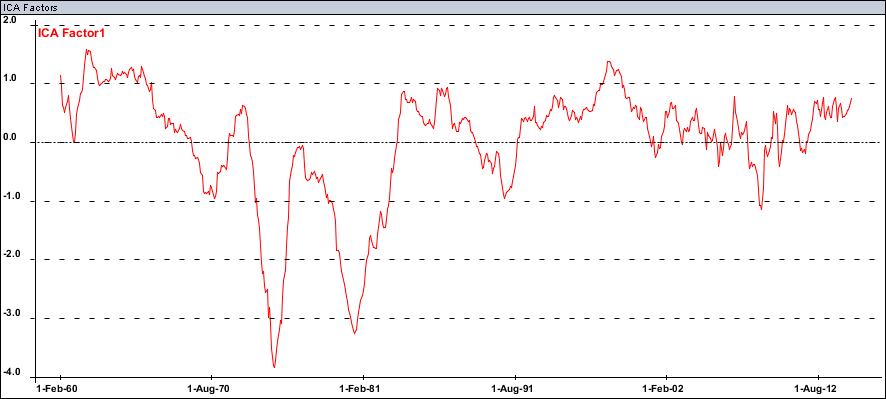

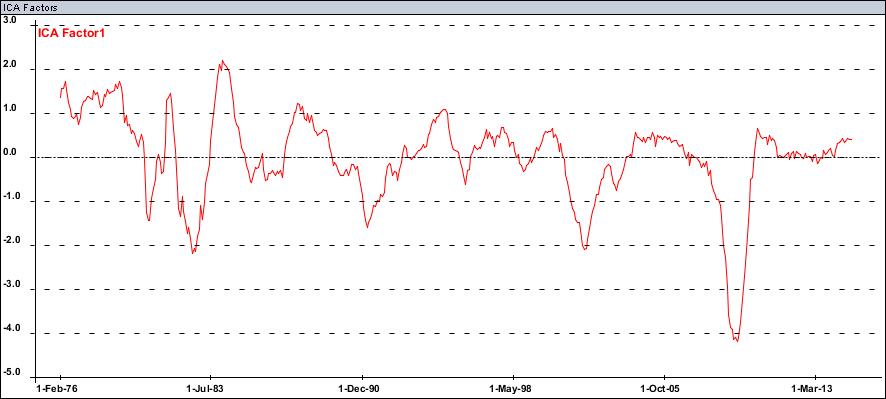

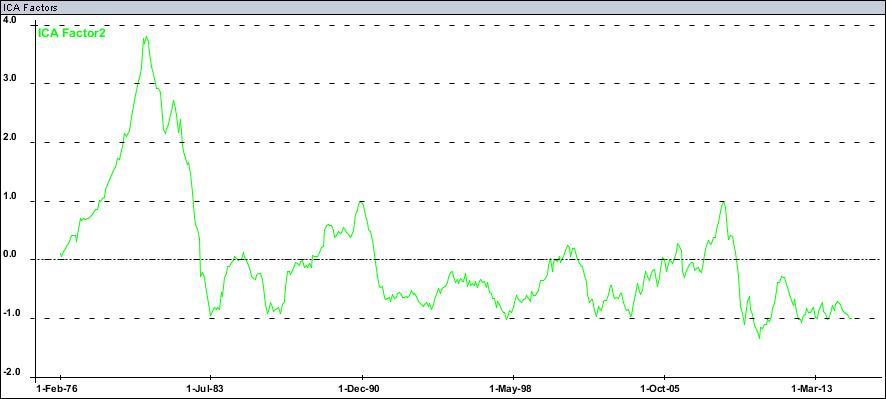

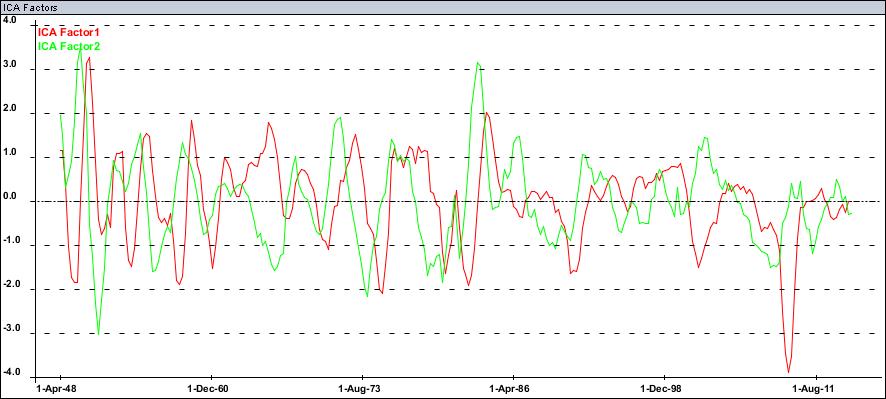

We use OECD MEI dataset to extract growth and inflation factors for each of the G7 countries (US, Japan, Germany, France, Italy, Canada, UK). Here are for example the US growth and inflation (sorry, inverted) factors (last data-point is October 2014):

Next we look what drives these 14 factors and come up with G7 growth factor

and G7 inflation factor

Not too optimistic though dataset and is very Euro-centric.

World trade and industrial production

World trade indicator based on common factor

World industrial production indicator based on common factor

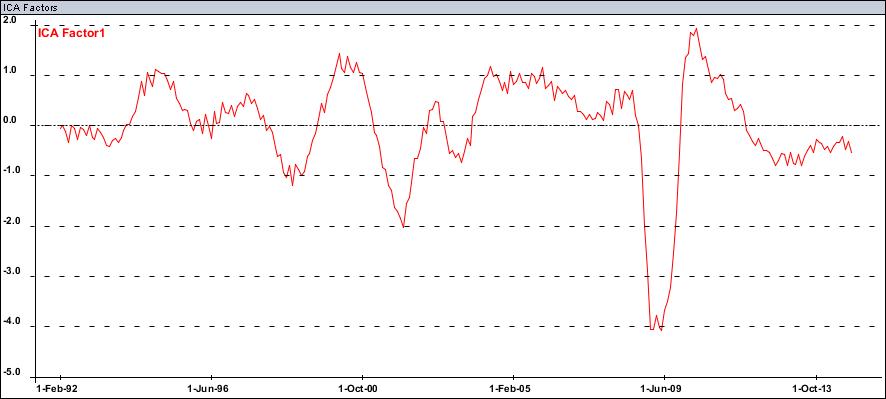

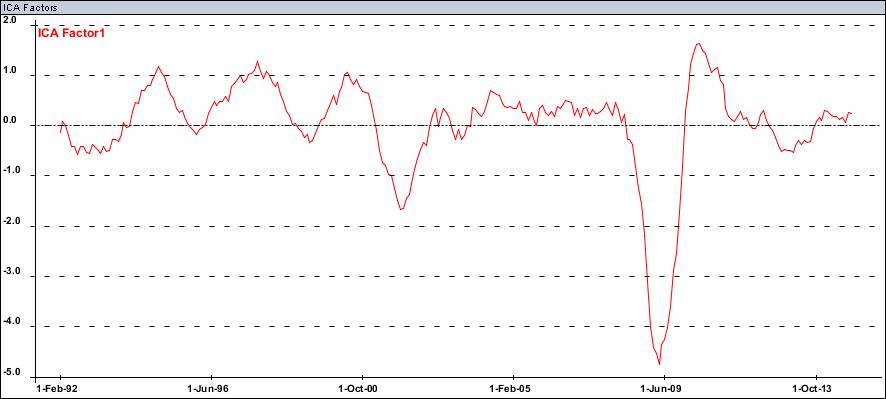

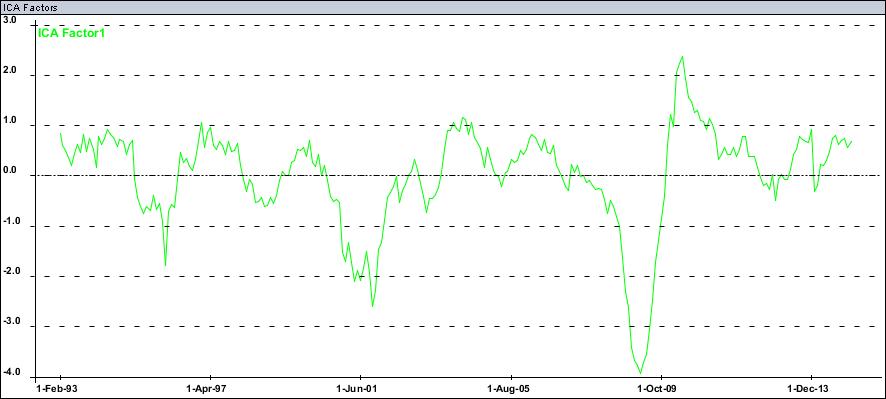

US conventional growth leading indicator

Our conventional US growth leading indicator

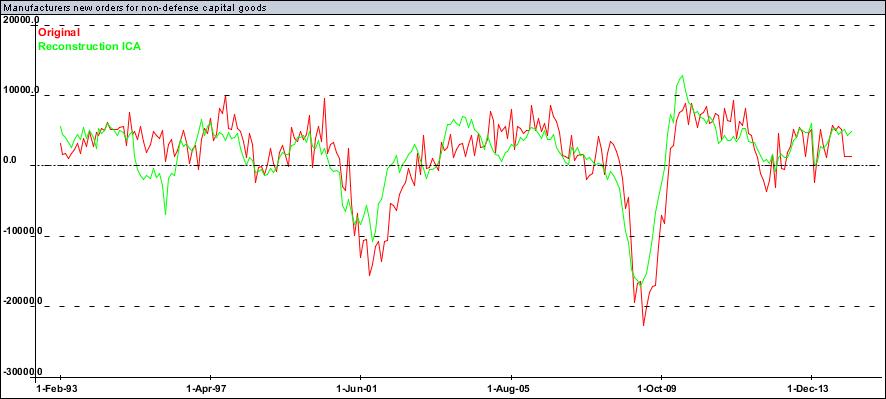

Important to note that manufacturers new orders for non-defense capital goods have not been following suite recently and surprised to the downside

It is also noteworthy that decomposing leading indicators into two leading factors instead of one we see one surging leading indicator with higher lead (green) which is driven by PMI new orders and second factor which is now more of a coincident indicator and which continues to slowdown.

It is hard to say what is going on and we will be watching it carefully in the coming months.

US coincident inflation indicator

Our coincident inflation indicator shows no inflation in sight

US job creation

Our job creation indicator based on Establishment Survey data still looks solid (though it is lagging indicator):

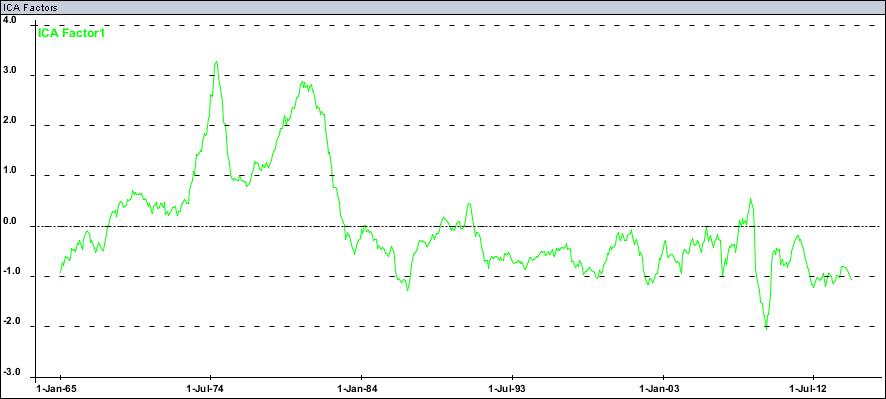

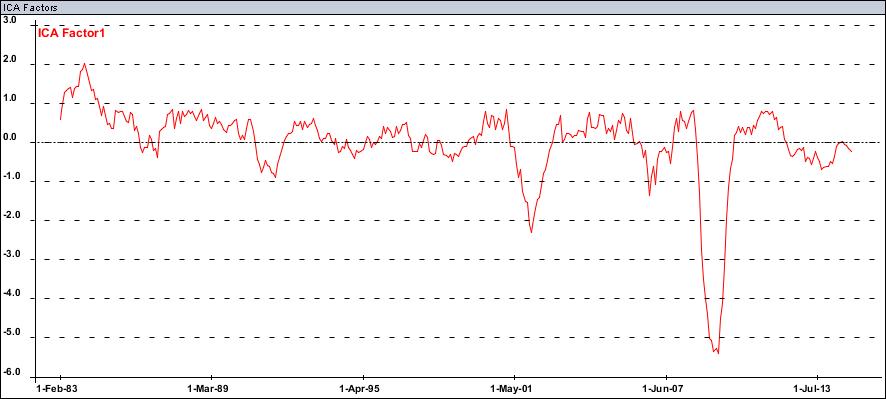

US growth and inflation based on Macro-Yield model, small and large datasets

Our Macro-Yield model growth factor is not particularly optimistic

Our growth and inflation factors based on the small US dataset

Growth:

Inflation (sorry, inverted):

Similar results in our growth and inflation factors based on the large US dataset

Growth:

Inflation:

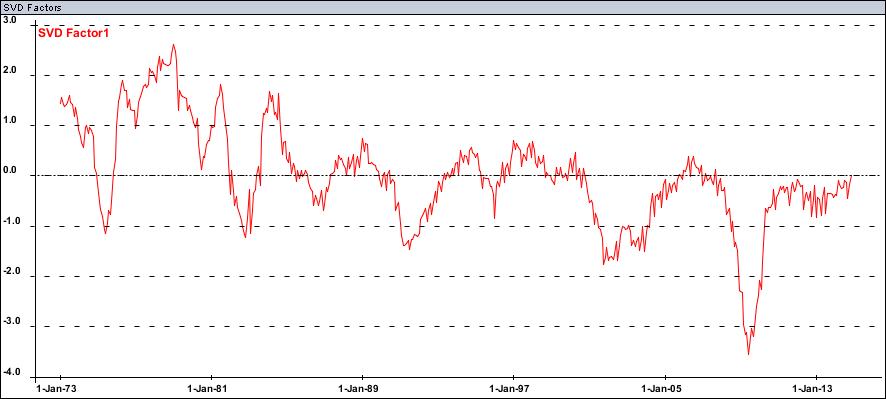

US GDP-based leading indicator

Finally GDP-based growth leading indicator[9] is not too optimistic

Happy Holidays and Happy New Year!

[1] Dynamika Commentary, “Lifted by Germany and China”, 16 August 2014

[2] Dynamika Commentary, “Monitoring the late cycle symptoms”, 1 June 2014

[3] Dynamika Commentary, “Watch out for the late cycle symptoms”, 30 March 2014

[4] BIS, “A shadow policy rate to calibrate US monetary policy at the zero lower bound”, June 2014

[5] Dynamika Commentary, “Where do the leading indicators lead?”, 28 February 2014

[6] Dynamika Commentary, “Watch out for the late cycle symptoms”, 30 March 2014

[7] Dynamika Commentary, “The global interplay of business cycles”, 31 May 2014

[8] Dynamika Commentary, “Lifted by Germany and China”, 16 August 2014

[9] Dynamika Commentary, “Watch out for the late cycle symptoms”, 30 March 2014