As the economic and market cycles progress, increased volatility[1] should be expected; however, none of our Five Forecasters show elevated reason for concern, indicating a recession is unlikely in 2015.

Pullbacks Do Not Mean the End of a Bull Market

The relatively stable and upward-sloping stock market trajectory of recent years has caused investors to become unaccustomed to pullbacks, making them more likely to overreact during any spike in market volatility. An important element to remember is that an increase in volatility, especially in the latter stages of an economic expansion, is quite common. In addition, pullbacks in equity prices are frequent occurrences and showcase a healthy relationship in the tug-of-war between buyers and sellers, bulls and bears. In fact, during this current bull market that started on March 9, 2009, in which the S&P 500 has delivered a 236% cumulative return,[2] there have been 20 modest market pullbacks of 5% or more. During the 1990s bull market, there were 13; in 2002–2007, there were 12. Considering the average of 3–4 pullbacks per year, the last couple of years have been uncharacteristically quiet, but that is likely to change in 2015 [Figure 1].

Pullbacks do not mean the end of the bull market is near. In fact, most bull markets since WWII included only one correction of 10% or more, and the current expansion has had two already (2010 and 2011), though 2012 and 2014 brought close calls. Bull markets do not end because of a rise in volatility, an increased frequency of market downdrafts, or even the lengthening duration of the economic expansion. The labor markets are improving but are not strong enough yet to generate anything more than modest upward pressure on wages to drive inflation, and U.S. factories have excess capacity. As a result, the Fed is unlikely to start hiking interest rates until the latter part of 2015 at the earliest.

What to Do When the Market Delivers a Pullback

Given the likely increase in volatility and the more frequent occurrences of market downdrafts, what is the right way to navigate a pullback or even a correction in stock prices? The simple answer is to follow your investment plan and not let emotions dictate a detour. Fear and subsequent overreaction are almost always the best ways to ruin a great plan. As investors, we must understand that volatility is a part of the market. Pullbacks provide a balance that helps to cull excesses before they become larger problems; they can even help to set the stage for investment opportunities.

We advocate two steps to best approximate the severity of a market downdraft (i.e., pullback, correction, or bear market) and consequently, determine when a market decline becomes an attractive opportunity. First, understanding the distributions of declines helps to frame stock market pullbacks. In short, since the start of the bull market in 1982, 47% of the 8,282 days for the S&P 500 Index have been negative but only 62 have turned into pullbacks, 6 into corrections, and only 5 have turned into bear markets (losses of 20% or greater).[3] When declines happen, the bumps feel terrible. We then extrapolate the worst case scenario and feel worse. But the reality is, in investing (and in life itself), the worst case scenario rarely happens—and the outcomes are far less drastic than we emotionally feel when living through it.

Second, using LPL Research’s three-question approach can help you evaluate the likely severity of a market decline. When stocks decline, take this step-by-step approach and ask yourself the following questions:

1) Is a recession likely around the corner?

2) What caused the stock market decline?

3) What are the catalysts for reversal?

Asking and understanding these three questions can help estimate the potential severity of a decline, targeting the most likely scenario as either a pullback (0–9% decline), correction (10–19% decline), or bear market (20% or more decline), which can then set the stage for making rational decisions and even transforming a challenging period into a potentially profitable opportunity. It is important to note that nothing is completely predictive of the market’s future direction, especially during periods of increased volatility and market downdrafts, as investor panic is a powerful force. But staying patient, following a financial plan, and understanding this three-question framework can help in weathering short-term spikes in market volatility.

Question 1: Is a recession likely around the corner?

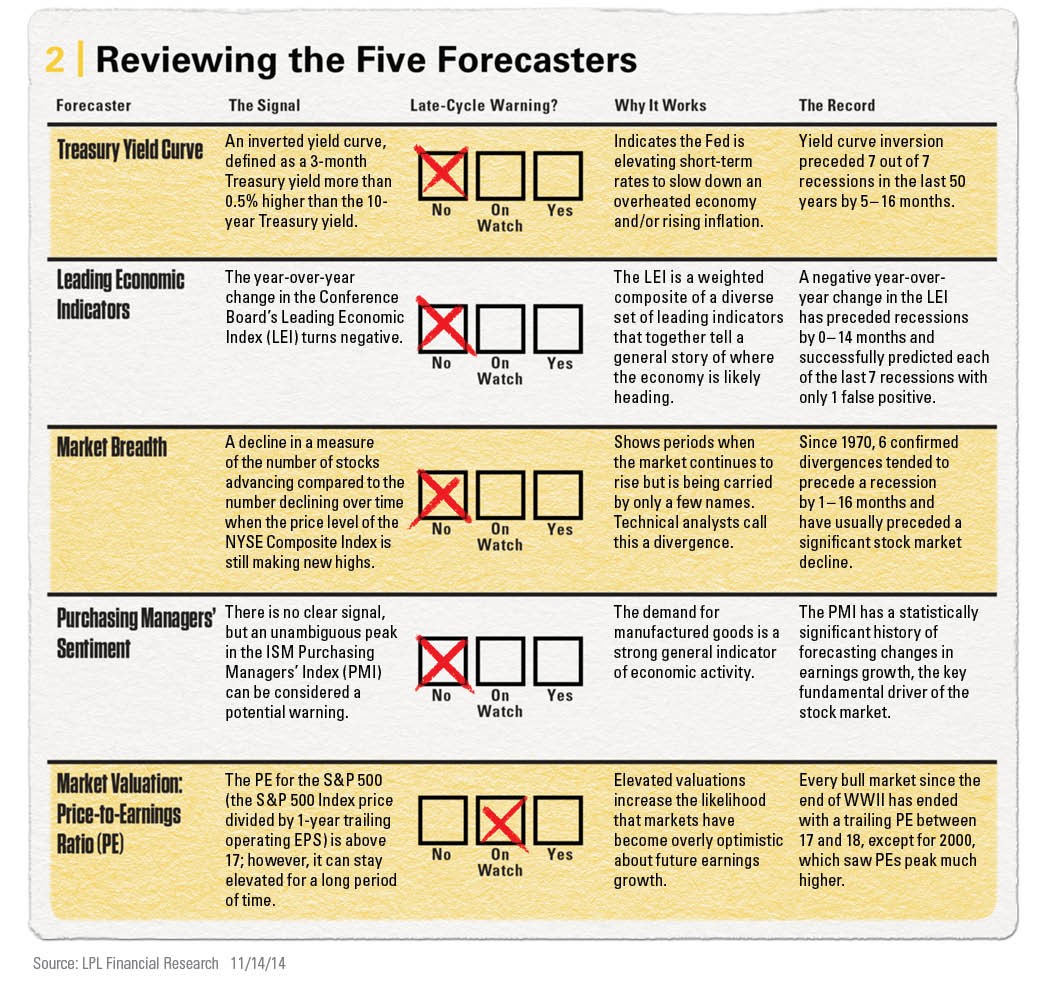

The goal of this question is to determine the likelihood that the market backdrop can create the conditions for a full-blown bear market. The bottom line is that bear markets rarely occur outside of recessions. In fact, since 1980, there have been five bear markets and all but one happened around or during a recession, which leads to the question: How do you know if a recession is on the doorstep? We look for excesses in the market and economy by examining the Five Forecasters—data series that have had a statistically significant historical track record of providing warning signs that we are transitioning to the fragile, late stage of the economic cycle [Figure 2].Once we receive these signals, on average, we can expect a recession within the next 6 to 12 months. It is important to note that none of the Five Forecasters currently show cause for concern, which indicates a recession (and the subsequent bear market) is unlikely in 2015.

Question 2: What caused the stock market decline?

Once the likelihood of a recession and bear market has been assessed, the next two steps help to hone in on the subtle, but significant, differences between whether a market drawdown is a run-of-the-mill pullback or of the more significant correction variety. In other words, is the market’s wound a deep cut or a scratch? The first step is to determine the cause of the decline. Usually, corrections of 10% or more happen if the cause is a single significant event (a geopolitical event, a natural catastrophe, etc.), rather than the culmination of many smaller events. For example, the uncertainty surrounding the run-up to the Iraq War in 2003 saw a 14% correction. Corrections often need a “deep cut” to instigate a major decline rather than a series of market “scratches.” For example, in the fall of 2014, stock prices fell sharply but did not quite reach correction territory. Numerous reasons—including the rise of Islamic State militants, the Ebola outbreak, the prospect of Europe headed to a recession, China’s slowdown, extended valuations, and the Fed taper—drove the sell-off. As a result, this “scratches” scenario signaled to investors that the market decline was likely limited to a pullback and not a correction.

Question 3: What are the catalysts for reversal?Last, are there compelling reasons for potentially turning the market’s “frown” upside down? Naturally, if there are several strong catalysts to lure bulls back into a market in decline, the likelihood is a less severe experience. We forecast that the continuing recovery of the labor market, attractive corporate fundamentals, and strong earnings growth can serve as the sparks that could keep most of 2015’s increased volatility in the pullback category, suggesting investors may be better served viewing these declines as opportunities rather than challenges.

In summary, to navigate a pullback effectively, first evaluate the change in the context of history; and second, evaluate the specific drivers in the current scenario.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Tracking # 1-339037 (Exp. 12/15)

[1] Greater volatility involves the potential for greater loss.

[2] Measured by the S&P 500 Index from the market’s close on March 9, 2009 to October 31, 2014. Past performance is not indicative of future results. One cannot invest directly into an index.

[3] According to Bloomberg data and LPL Financial Research analysis as of 11/14/14.