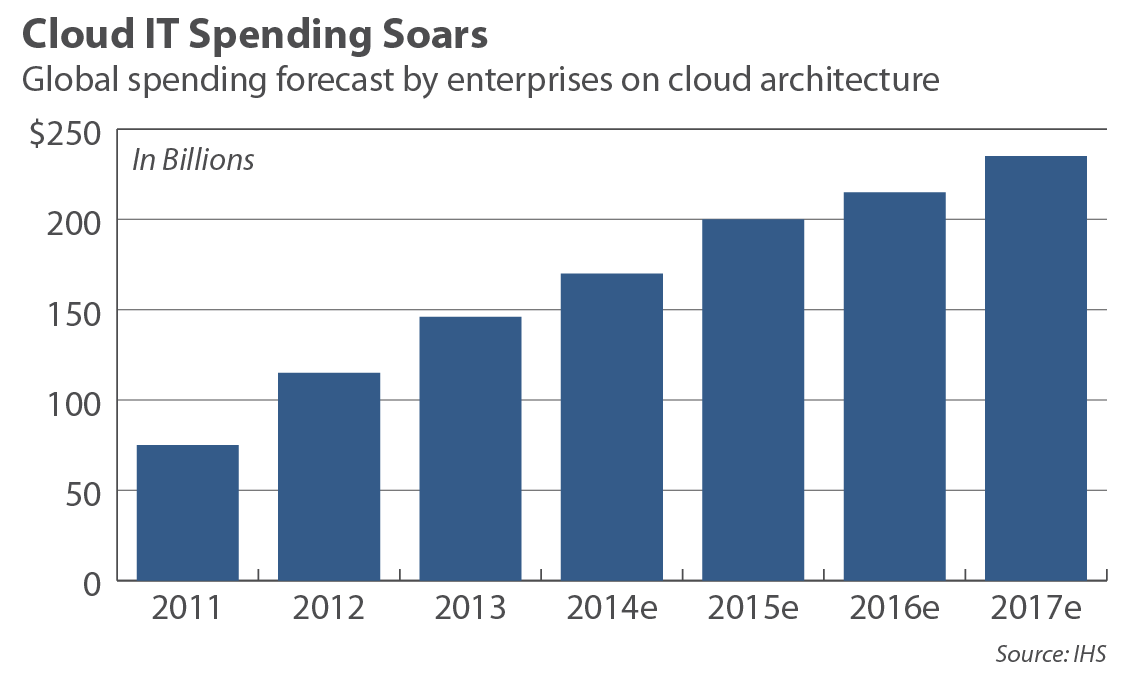

Cloud computing may be the most compelling and, thus, perhaps the most lucrative technology theme over the rest of this decade. Global enterprise spending on cloud computing, which excludes consumer purchases, is expected to be $235 billion in 2017 — triple the $78 billion spent in 2011.¹ In this context, what is cloud computing and what factors are important to investors?

Although its definition varies, we define cloud computing as any subscription-based or pay-per-use service that — in real time, over the Internet — extends your technology infrastructure and capabilities. It includes Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS).

IaaS firms provide virtualized hardware, primarily storage and servers. Gartner, a leading information technology research company, reports that worldwide IaaS revenues were $9 billion last year and projects them to be $24 billion in 2016. Amazon.com epitomizes this market with its Amazon Web Services (AWS) unit producing $1.3 billion in sales last quarter, up 40% versus the same period a year ago.

With PaaS, a similar service delivery model, customers rent virtualized servers and services in order to run their applications or to develop and test new ones. Software developers most often use this service. Gartner predicts that the global PaaS market will be $2 billion this year and $3 billion in 2016. Google competes in this space with its Google App Engine.

Global enterprise spending on cloud computing is expected to rise to $235 billion.

SaaS offers customers access to software applications over the Internet. Customers rent the software, typically on a monthly basis, rather than buy it up front. The service provider hosts applications, whereas in the prior delivery model they had been installed on customers' computers. Gartner pegs this worldwide market at $24 billion in 2014 and sees it growing to $33 billion in 2016. Analysts expect leading SaaS firm Salesforce.com to increase sales more than 30% this fiscal year to over $5 billion.

To capture this investment theme, investors must determine which of the incumbent technology companies will be made obsolete by the cloud and which ones will survive the transition and perhaps even thrive as a result. One of the best examples of the latter is Adobe Systems, which Saturna held at the end of November in the Amana Growth (4.14%) and Sextant Growth Funds (2.18%).

Founded in 1982, Adobe is a dinosaur, at least from a technologist's perspective. It has offered its Creative Suite of products, including Photoshop, InDesign, Dreamweaver, and Premiere, since 2003 as software to be purchased and installed on customers' premises. However, in May 2013 the firm moved these products to the Creative Cloud. Now a Photoshop customer can only update that software in the cloud.

Adobe's CEO Shantanu Narayen forced this drastic business model change. In Silicon Valley if you do not quickly cannibalize yourself, a competitor — sometimes another incumbent, but more likely a start-up company — will do it for you. Narayen showed courage in embracing the cloud because the financial implications for any firm, particularly in the first year of this transition, are scary. Why? Because analysts often gauge a firm's sales and profits on a quarterly basis versus the same period a year ago, and they generally want to see an increase. Nothing chills analysts — technology investors in particular — more than significant year-over-year declines in reported revenues and earnings per share.

Unfortunately, that often appears to be the case when a firm such as Adobe switches its product delivery model from one where revenue is recognized up front (when the software is sold) to an SaaS model where the revenue stream is divided into smaller monthly payments (when the software is rented). Adobe made it through the perilous first year of its transition to SaaS while most of its peers still cling to the old paradigm or have just begun the switch. Gladly, Adobe's shares returned 27% over the twelve months ended November 18, versus 15% for the S&P 500. In technology, it is almost always good to be first.

For better or worse, sometimes there's no scarier roller coaster than the technology sector. Products go in and out of favor at a rapid pace while making or breaking companies and enriching or busting their investors. It's not practical to avoid the ride altogether, especially when growth is among your investment objectives. Identifying and acting upon the longer-term trends can help alleviate the white-knuckle effect.

Saturna's analysts continue to scrutinize incumbent technology companies to determine which will become meaningful cloud computing beneficiaries. We also keep a watchful eye on emerging firms that establish promising track records as potential cloud investments.

|

Ownership of Securities Mentioned |

Amana Growth |

Sextant Growth |

|

Adobe Systems |

4.14% |

2.18% |

|

Amazon.com |

|

0.83% |

|

Gartner |

1.02% |

|

|

Google, Class A |

2.22% |

1.11% |

|

Google, Class C |

|

0.69% |

|

IHS |

|

|

|

Salesforce.com |

|

|

Security weightings are shown as a percentage of a Fund's total net assets. Amana Income, Amana Developing World, Idaho Tax-Exempt, Sextant Bond Income, Sextant Core, Sextant Global High Income, Sextant International, and Sextant Short-Term Bond Funds did not own any securities of the companies mentioned.

Footnote

¹ Enterprise Cloud Spending to Soar to New Heights in Quest to Drive Greater Business Success. IHS Press Release, April 3, 2014. http://press.ihs.com/press-release/design-supply-chain/enterprise-cloud-spending-soar-new-heights-quest-drive-greater-bus

Copyright 2014 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 8 · No. 10

Important Disclaimers and Disclosures

This report is intended only for the information of the reader and is not to be used for or considered as an offer or the solicitation of an offer to sell or buy any securities or other financial instruments of any kind, including without limitation, any mutual fund or other product offered, sponsored, created, or managed by Saturna Capital Corporation or its subsidiaries or affiliates ("Saturna"). This report is not intended for distribution to, or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country, or other jurisdiction in which such distribution, publication, availability, or use would be contrary to law or regulation or which would subject Saturna to any registration or licensing requirement within such jurisdiction.

This document should not be considered as providing investment advice or services, or any other service offered by Saturna. Saturna may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the report.

Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor's circumstances or otherwise constitutes a personal recommendation to any investor. Saturna does not offer advice on the tax consequences of any investment.

All material presented in this report, unless specifically indicated otherwise, is under copyright to Saturna. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied, or distributed to any other party without the prior express written permission of Saturna. Unless otherwise indicated, all trademarks, service marks, and logos used in this report are trademarks or service marks of Saturna.

The information in this report was obtained from sources Saturna believes to be reliable, and Saturna believes the information and opinions in the material are accurate and complete as of the date of this material. However, information and opinions contained herein will change over time and without notice. Saturna has no obligation to update or amend any information or opinions at any time. Saturna makes no representations as to the accuracy or completeness of this material, nor does it have any responsibility to ensure that any other materials, including any containing materially different information, are brought to the attention of any recipient of this report.

Under no circumstances shall Saturna, its employees, or any affiliate be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to making any investment based on this report or for any necessary explanation of its contents.

Saturna does not provide tax, legal, or accounting advice. Investors should consult their own tax, legal, and accounting advisers before engaging in any transaction. In compliance with IRS requirements, recipients are notified that any discussion of US federal tax issues contained or referred to herein is not intended or written to be used for the purpose of (A) avoiding penalties that may be imposed under the Internal Revenue Code; nor (B) promoting, marketing, or recommending to another party any transaction or matter discussed herein.

The Dow Jones Industrial Average is a price-weighted index of 30 of the largest, most widely held US stocks. The S&P 500 is an index comprised of 500 widely held common stocks considered to be representative of the US stock market in general. The Russell 1000 Growth index is a widely recognized index of large-cap growth stocks. The Russell 2000 Index is comprised of US small cap stocks and measures the performance of the 2,000 smallest US companies in the Russell 3000 Index. The NASDAQ Composite index measures the performance of more than 5,000 US and non-US companies traded "over the counter" through the National Association of Securities Dealers Automated Quotation system. The MSCI EAFE Index, produced by Morgan Stanley Capital International, measures the equity market performance of developed markets in Europe, Australasia, and the Far East. The MSCI Emerging Markets Index, produced by Morgan Stanley Capital International, measures equity market performance in over 20 emerging market countries. Barclay's Capital US Aggregate Bond Index measures the performance of the US bond market.

All indices shown are widely recognized unmanaged indices of common stock and bond prices that reflect no deductions for fees, expenses, or taxes. Investors cannot invest directly in the indices.

Past performance does not imply or guarantee future performance, and no representation or warranty, express or implied, is made regarding future performance. The price for, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of foreign securities and financial instruments is subject to exchange rate fluctuations that may have a positive or negative effect on the price or income of such securities or financial instruments. Investors in securities such as American Depositary Receipts — the values of which are influenced by currency volatility — effectively assume this risk.