Weighing the Week Ahead: A Message from the Bond Market?

Last week’s wild trading defied any simple explanation. That always sets the table for pundit pontification!

We are still a week away from earnings season. Bond, stock and commodity prices are moving in different directions. I expect this divergence to be a focus of attention, with many asking: Is the Bond Market Sending a Message about the Economy?

Prior Theme Recap

In last week’s WTWA I predicted that there would be a focus on alleged January effects. That was very accurate, especially after the first two days of the week included a major decline. As always, Doug Short’s weekly snapshot tells the story at a glance. If you snoozed through the week, you missed it!

Here were the competing theories:

- As goes January, so goes the year. Most of these stories included January as part of year, so the result was biased.

- As goes the first X days of January, so goes January. Once again the analysts often included these days in the month’s result, biasing the outcome. They also argued over whether January 2nd should count, since it was part of the holiday week. One top authority said that the theory worked for the first two days, but not the first five. Another expert, a regular on CNBC’s Fast Money, chained the days and the month together, calling the evidence irrefutable.

I hope that my readers will be skeptical about two days of trading predicting the next 250. There is certainly no reason to pick two days rather than five. These are the stories attracting big ratings, despite making little sense.

What you should do, of course, is look at the independent and dependent variable separately, using January to predict the next eleven months. You might also ask whether the same effect is seen in any other months. CXO Advisory reported this research last year. January explains only about 5% of the variance for the rest of the year, with the rest left to randomness or other factors. January is no better than other months. Etc. This kind of research deserves more publicity. This chart (one of many good ones in the article) shows that whatever the very modest effect, it ended over 30 years ago.

Will we hear the same story next year? Probably. These stories never seem to die.

Feel free to join in my exercise in thinking about the upcoming theme. We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead.

This Week’s Theme

While there is plenty of news on tap this week, we still have a week before the start of earnings season. It is a time that defies easy explanation, with wild gyrations in stocks and divergent moves in bonds and commodities.

I expect a focus on bonds, with the question:

Is the Bond Market Sending a Message about the Economy?

There are two basic viewpoints:

- Bonds are flashing a recession warning. Peter Eavis of the NYT’s DealB%k has a post on the perspective of the bond guys.

- Low bond yields reflect other unusual factors. Menzie Chinn at Econbrowser describes some of these.

- Bonds not cheap, but no bubble. (Prof. Shiller via Money).

As always, I have some ideas about last week’s trading as well as next week’s question. More on that in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was a normal news week, with a positive tilt.

- Auto sales remained strong at a 16.8 million annual rate. But growth might be slowing. (Reuters).

- Consumer confidence via the Conference Board hits a new high. The Gallup weekly poll also shows strength.

- Dividends rose 10% in Q4. (Eddy Elfenbein).

- Initial jobless claims hold below 300K. This was a slight miss on stated expectations, but the small deviation is not the key story. Calculated Risk puts it in perspective, including this chart:

-

Employment net gains beat expectations. As usual this complex report had a mixed story.

- Net job gains continue to grow at a strong pace. It was the strongest year of job growth in the last 15, but economists still give the news a “B.” WSJ covers and see the “Bad” news below.

- ADP private employment confirms the story

- It hits the Fed’s sweet spot for improvement. (Jon Hilsenrath).

- Unemployment falls

The WSJ (Nick Timiraos and Josh Zumbrun) has a great summary of the report in ten charts. Here is one that highlights some of the most controversial features, change in overall earnings:

Even better, you can see the labor market via Janet Yellen’s Dashboard, an interactive feature at MarketWatch.

The Bad

The bad news was pretty minor.

- ISM non-manufacturing missed expectations with a reading of 56.2 (Steven Hansen at GEI has a balanced look at the trend).

- Factory orders declined 0.7%, a little more than expected.

- Consumer companies lower earnings guidance despite falling oil prices (FactSet).

- Government returns as top concern. Economic matters are a close second. (Gallup)

-

Employment news disappointed in several respects

- Hourly earnings fell 0.2%. Stronger wage gains would be most welcome. New Deal Democrat explains further. Doug Short notes that it is the biggest decline in eight years, supplying analysis and charts.

- Labor force participation declined again to 62.7%. Changing demographics accounts for part of the story, but this is the lowest level in decades.

The Ugly

Extremist terrorism. Again. The market seemed to have little reaction to the news from France, but it increases worldwide concern.

Noteworthy

Google is moving into the auto insurance business. Isn’t the company also pushing a driverless car? Coincidence no doubt!

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week, but nominations are welcome.

Fans of the Silver Bullet can check out our annual review of award winners, just in case you missed one. Most investors have been bamboozled by one or more of these stories, so an annual review can be helpful.

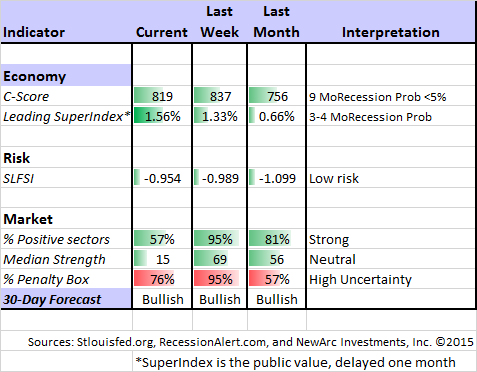

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting market indicators.

Doug Short: An update of the regular ECRI analysis with a good history, commentary, detailed analysis and charts. If you are still listening to the ECRI (three years after their recession call), you should be reading this carefully. Doug has the latest interviews as well as discussion. Also see Doug’s Big Four summary of key indicators.

Georg Vrba: has developed an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. Georg’s BCI index also shows no recession in sight. Georg continues to develop new tools for market analysis and timing. Some investors will be interested in his recommendations for dynamic asset allocation of Vanguard funds. Georg has a new method for TIAA-CREF asset allocation. He has added a method for Vanguard Dividend Growth Funds. I am following his results and methods with great interest. You should, too. This week Georg showed why the Fed might well pause before increasing interest rates.

Dow 20K in 2015? Just based on long-term data the odds are about 40%. Check out this analysis of the odds on the Jeremy Siegel forecast, and maybe also my own effort from years ago, when the Dow was at 10K — http://dashofinsight.com/dow-20k-and-the-wall-of-worry/

The Week Ahead

It is a week with a normal news flow and plenty of FedSpeak.

The “A List” includes the following:

- Retail sales (W). Special interest in the December data. Gas price effects?

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

- Michigan sentiment (F). Concurrent read on spending and employment.

- Crude oil inventories (W). Attracting a lot more attention these days.

The “B List” includes the following:

- JOLTS reports (T). Gaining attention for the right reason – an indicator of labor market slack. This affects the Fed decisions.

- Industrial production (F). Volatile series but important for GDP.

- Beige book (W). Anecdotal evidence to supplement the data at the next FOMC meeting.

- PPI (Th). Eventually this will matter.

- CPI (F). See PPI.

- Business inventories (W). Part of the GDP calculation. Only reason for interest in this November data.

I do not care about the regional Fed surveys, which seem to provide little help nor market impact. At least I am consistent. Some sources seem to disparage these volatile reports on some occasions and embrace them on others.

The calendar for Fed speechmaking is active, with at least four policy-related appearances.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix held a bullish stance throughout the week, despite the early turbulence. There is still plenty of uncertainty reflected by the extremely high percentage of sectors in the penalty box. There has also been some rapid changes in the top sectors, even in a relatively quiet market. Our current position is fully invested in three leading sectors. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com.

As I noted last week, Felix continues to feature selected energy holdings.

Also – Ten reasons traders lose money — -and some hints for a successful approach.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. We have recently updated our current ideas for investors.

We aim for a light-hearted approach in our “Hot and Not” review of the past year, but there is still a lot of investment truth. If you missed it, please take a look.

Other Advice

Here is our collection of great investor advice for this week:

Annual Reviews and Previews

I hope that readers will enjoy my annual Seeking Alpha preview interview. I have some ideas about market trends, the best sectors, and also some specific stocks. There is also a surprise ending. I recommend the entire Seeking Alpha “Positioning for 2015” series, which has many strong ideas and diverse viewpoints.

Roger Nussbaum highlighted the winning formula, and the warning for the future, in his interesting preview piece about Grandma.

Barry Ritholtz says to take them all with more than a grain of salt, doing a review of the highlights from 2014. Crash in bonds? Dow 5000?

Planning for the New Year

If readers were to follow one link this week, I recommend this collection of posts curated by Abnormal Returns. This is one-stop shopping for an individual investor doing planning for the year ahead. As I have frequently noted, I rely upon Abnormal Returns to keep up with great articles that I might not otherwise see. It is part of my research for WTWA. This particular article is attractive for a wide audience of investors.

Sectors and ETFs

The popular ETF might not be suitable for an individual investor. Barron’s notes that some “bespoke” ETFs are designed for big institutions. Despite large assets, the volume is light and the trading spreads are wide. I always watch for these factors. You should, too.

Ed Yardeni notes the positive impact of lower oil prices on earnings expectations for transportation stocks.

Stock Ideas

Goldman’s 40 cheapest stocks.

Market Prospects

Barron’s was probably not stealing the notes from my annual preview piece, but they certainly reached a similar conclusion: The Bulls Long Run is Not Over. Here is a good explanatory table:

But long-term investors should be prepared for a 20% correction. Josh Brown notes that this goes with the territory, occurring every three years or so, even in bull markets.

Wealth of Common Sense provides some long-term data on bonds, an interesting comparison to the stock table. Ben recommends looking at the current yield as the starting point.

Investor Psychology

Morgan Housel warns about thinking, I Knew it All Along. The entire article is well worth your time, but here is a key quote:

“Thank Fracking For Falling Gas Prices,” wrote The Daily Caller.

They’re probably right. It seems so obvious that the U.S. oil boom is pushing down gas prices that few feel much need to explain it any further.

But there’s something funny here.

We’ve known about the U.S. energy boom for years, long before oil prices started falling. And it wasn’t long ago that most people argued our oil boom would not lower gas prices.

“‘Drill, Baby, Drill’ Fails: Why Gasoline Prices Remain High Despite Oil Boom,” stated one article in 2013.

“Why More U.S. Oil May Not Mean Cheaper U.S. Gas,” argued another.

Before June, it was widely reasoned that since oil was traded on global markets, and demand from growing economies like China was ramping up, the U.S. oil boom wouldn’t lead to lower gas prices.

These arguments made sense, and were reasonable at the time.

But today we’re making the exact opposite argument. And just as confidently as before.

Kid Dynamite reminds us to take responsibility, not blaming the Kardashians (or the Fed) for our own mistakes. Great post and great list.

Buttonwood reminds us of easy it is to confuse skill and luck. Try your hand at this quiz (which 80% get wrong) as well as the key takeaway:

Jack is looking at Anne but Anne is looking at George. Jack is married, but George is not. Is a married person looking at an unmarried person? A) Yes, B) No or C) cannot be determined.

And this one…

Investors focus on the wrong measures. Studies find that earnings per share is the most popular measure of corporate performance and is often used for executive pay. They also find that “the majority of companies are willing to sacrifice long-run economic value to deliver short-run earnings” doubtless because of those executive incentives. But the correlation between eps growth in one three-year period and the next is actually negative; you can prop up the measure for a while but eventually growth reverts to the mean.

And how this all applies to the seduction of market timing – and why you cannot do it. (Brooklyn Investor).

Result: Many individual investors lost out – data via Stephen Gandel at Fortune. I trust that our readers did better!

Final Thought

Last week I wrote that I am not a big fan of seasonal effects unless there is a logical underlying reason. This week’s trading demonstrated why. For part of the week, daily trading was linked to oil prices and the simple heuristic followed by some computerized methods. This is a correlation analysis from months past, when a better economy lifted both oil prices and stocks, something that statisticians call a spurious correlation. It means that both factors are caused by something else.

By mid-week the executives at pension funds had returned from vacation and held their first investment committee meetings. Wednesday and Thursday reflected that. By Friday we were back to relatively normal daily news effects, including the mixed message from the jobs report.

My annual preview takes on the question of the bond market message. There are many reasons for some to own bonds, but the extremely low interest rates suggest something beyond that. I suggest a leveraged arbitrage with Europe and Japan. Please note: This is basically the opposite of the 1998 carry trade. Please read the entire article and feel free to comment!

I am comforted that the best real-time recession forecaster for the last 30+ years, Bob Dieli, is not alarmed by the bond market moves. He and I follow the key spreads carefully and these are also factors in my weekly updates for the SLFSI. These are long-term, objective indicator. No hype to sell page views. Sometimes the less dramatic story is the right one.

© New Arc Investments

http://dashofinsight.com