Markets May Be Choppy, but Equities Should Advance in 2015

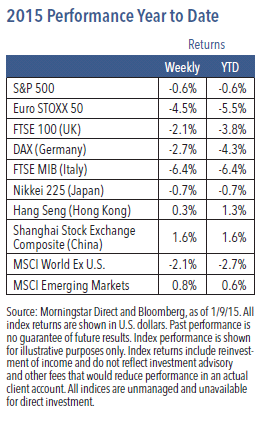

The year started off with equity markets experiencing volatile trading. Stock prices dropped sharply in the first few trading days before recovering, while oil prices plummeted and bond yields fell. Last week, U.S. equities lost ground and the S&P 500 Index declined 0.6%.1

The Slide in Oil: Some Risks, but Probably More Benefits

Oil prices have now declined more than 50% since the middle of last year, with Brent crude dropping below $50 last week.1 Falling oil prices hurt oil producers but benefit oil users, and since there are far more users of oil than there are producers, the net effect of lower prices on the global economy should be positive. Falling oil prices also put downward pressure on inflation. This combination of a boost to growth and lower inflation is one reason stock prices have been rising while bond yields have been falling over the past several months.

Weekly Top Themes

1. Jobs growth remains solid. December’s employment report showed that 252,000 new jobs were created in the final month of 2014. This brings the total number for the year to over 3 million, the best annual rate since 1999.2 The data contained no evidence that lower oil prices have depressed employment growth.

2. Falling oil prices are hurting corporate earnings expectations. The consensus for 2015 earnings per share for the energy sector has fallen by about one-third over the past three months.3 This has caused overall corporate earnings estimates to decline, and 2015 consensus expectations are currently for an 8% growth rate.3

3. The sharp rise in the value of the U.S. dollar could present some growth risks. Since the middle of last year, the value of the dollar has risen by close to 10%, the largest six-month move since the 2008 financial crisis.1 The magnitude and pace of the increase could translate into a modest drag on U.S. economic growth, chiefly through lower U.S. exports.

4. The Federal Reserve appears to be on track to raise rates this year. Last week’s release of the minutes from the Fed’s December meeting show that most members believe deflationary pressure and weaker growth outside of the United States should not significantly affect U.S. growth. We expect to see the first rate hike around the middle of 2015.

5. Divergent growth levels and central bank policies could result in uncertainty and volatility. While the U.S. and U.K. central banks are set to begin tightening,other areas are still in the midst of easing. Chinese growth appears to be slowing significantly, Russia and Brazil may be sliding into recession, Japanese growth is stagnating and Europe continues to struggle with the threat of deflation.

6. Political discord makes the prospects for legislation uncertain. With Republicans now in control of Congress, we expect they will pass more legislation, but President Obama has made it clear he will not hesitate to veto bills with which he disagrees. There is a long list of important issues to be addressed (including energy policy, trade, health care, immigration and tax reform), but none of the issues have clear sailing ahead.

7. Historical trends suggest this month and year may be positive for equities. Despite declines in the first three trading days of 2015, stocks rallied the next two days, meaning the S&P 500 gained 0.2% over the first five days of the year (before experiencing a subsequent downturn).1 Since 1958, when the first five days were positive for equities, markets in January advanced 74% of the time with an average return of 2.2%, and full year returns were up 74% of the time with an average return of 10.4%.4

The Main Themes from 2014 Should Persist

Over the past six months, accelerating U.S. growth and diverging monetary policies have been pushing the value of the U.S. dollar higher while falling oil pries have kept inflation in check. The global economy remains troubled, but we expect it will slowly recover thanks to solid U.S. growth and aggressive policy support. We anticipate that oil prices will eventually experience a moderate rebound from oversold levels, which should provide some support for risk assets. Investment markets are likely to be more volatile in 2015 than they were last year, but we expect global equity prices and bond yields to rise over the next 12 months as the recovery gains traction.

1 Source: Morningstar Direct, Bloomberg and FactSet, as of 1/9/15 2 Source: Bureau of Labor Statistics 3 Source: Goldman Sachs Global Investment Research 4 Source: Merrill Lynch Bank of America Global Research

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

©2015 Nuveen Investments, Inc. All rights reserved.

GPE-BDCOMM2-0115P 5224-INV-W01/16