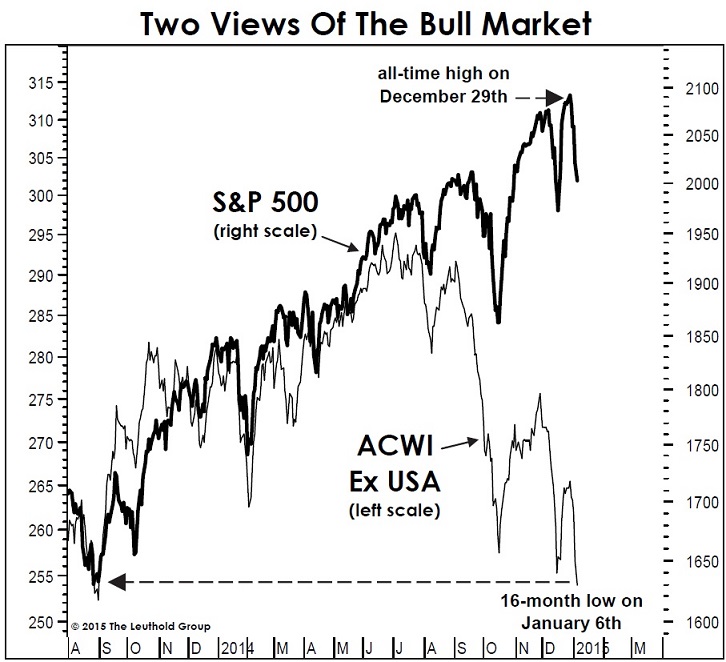

We expressed some concern about financial markets in last quarter's client letter and stated the theme of the letter was volatility. That characteristic carried over into the fourth quarter and caused our concern to heighten considerably. The S&P 500 finished with a flourish rising 4.9% in the quarter and 13.7% for the year. Unfortunately most other major stock indices were much weaker (see chart below), and we read the divergence as a warning signal. U.S. small capitalization stocks rallied almost 10% in the quarter to get into positive territory but finished the year up 5.8%. Developed international stocks fell in the quarter more than -3% and ended the year down over -4%. Emerging market stocks declined by about -4.5% in the quarter and about -2% for the year. A healthy market is much more broad-based and usually led by cyclicals and consumer discretionary shares. In 2014, defensive sectors, healthcare and utilities, led gains in the S&P 500 while many other sectors had modest returns.

Anyone who scans the investment landscape beyond the S&P 500 should be anxious. Weak gold prices, falling commodity prices, low government-bond yields and downward revisions to growth forecasts all point to a serious risk of deflation which is the last thing that countries with high debt burdens need. The extent and suddenness of the fall in bond yields and oil prices suggests the global economic outlook is very soft. Japan has been battling deflation for decades, prices in the eurozone are falling for the first time in more than five years, and even China is experiencing low inflation. The Economist reports that consumer prices in the Middle Kingdom are up just 1.6% over the last 12 months, while producer prices have been falling for 32 months. Data from Bloomberg and the Financial Times indicate investors think low inflation is here to stay. Market inflation expectations for the five years starting in five years’ time are at new lows in the eurozone and 2008 levels in the US.

Too much debt is a huge risk factor during deflationary times. While parts of the world economy, the U.S. consumer for instance, have reduced debt, the overall debt burden is at an all-time high due to central banks and sovereigns significantly increasing leverage.

It usually doesn't pay to fight the world's central banks when they are intent on propping up financial assets. The various forms of central bank largesse since the financial crisis were the main reason we've been positive on stocks. Every downturn in 2014 was halted by some news or action from one of the world's central banks, whether it was China cutting interest rates, Japan expanding their quantitative easing program, Mario Draghi hinting about buying eurozone sovereign debt, or Fed officials making dovish comments. From our perspective it appears monetary policy has done all it can. Its impact on the economy at this point is minimal. Central bank actions and musings do affect confidence in the short term, but we suspect the story for 2015 may be that investors lose faith in the ability of central banks to cure all the world's economic problems.

Despite all that we've said so far stocks should not be abandoned completely. U.S. stocks are not cheap but neither are they in bubble territory. Plus many companies sport attractive dividend yields and are seen as havens especially since the U.S. is by far the best developed world economy. Falling energy prices may not be the elixir many pundits hope it to be, but it will certainly be much needed relief to the beleaguered low- and middle-classes. Despite the economic challenges overseas, stocks abroad are cheap and in many cases have even higher dividend yields which are attractive in a low-yield world.

Short-term stock market movements are largely random and unpredictable. Longer term predictions are generally more accurate because they are based primarily on starting valuations, which suggests long-term returns will be modest compared to the recent past. While increased volatility may not herald a big decline we believe it is time to move from a more passive approach of generally being fully-invested to a more active approach with the goal of improving returns and reducing risk.

Let us know if you have any questions.

Jim Tillar, CFA, Steve Wenstrup

The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities listed herein will remain in an account's portfolio at the time you receive this report. It should not be assumed that any of the securities holdings listed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable. In addition we do necessarily agree with or endorse any outside commentary within this newsletter. If you have received this electronic transmission in error, please notify us by telephone (937) 428-9700 or by electronic mail [email protected]. Tillar-Wenstrup Advisors LLC does not necessarily agree with outside commentary. . Chart in the article is from the Leuthold Group.