The economy

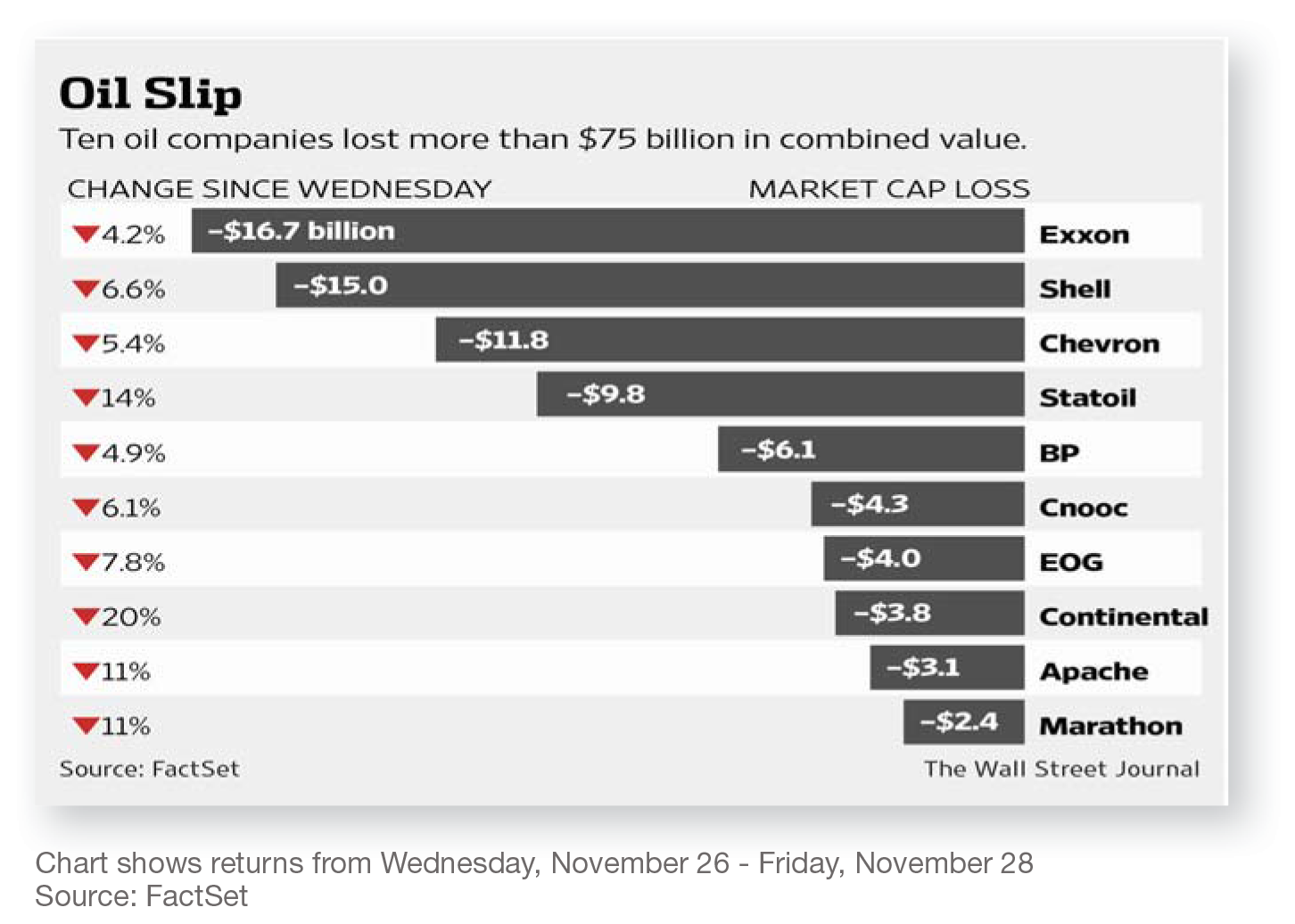

Drop in energy prices dominates global headlines

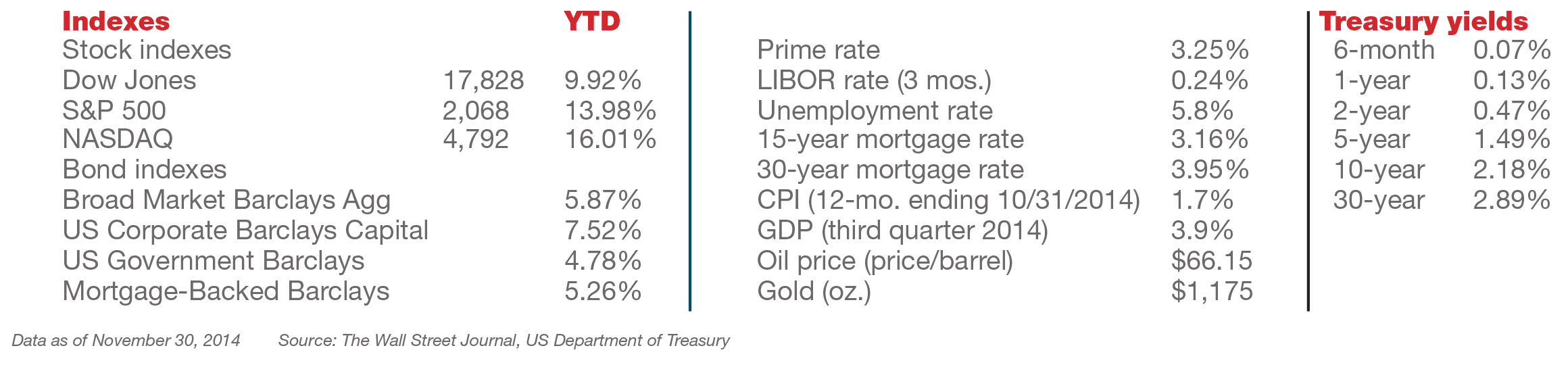

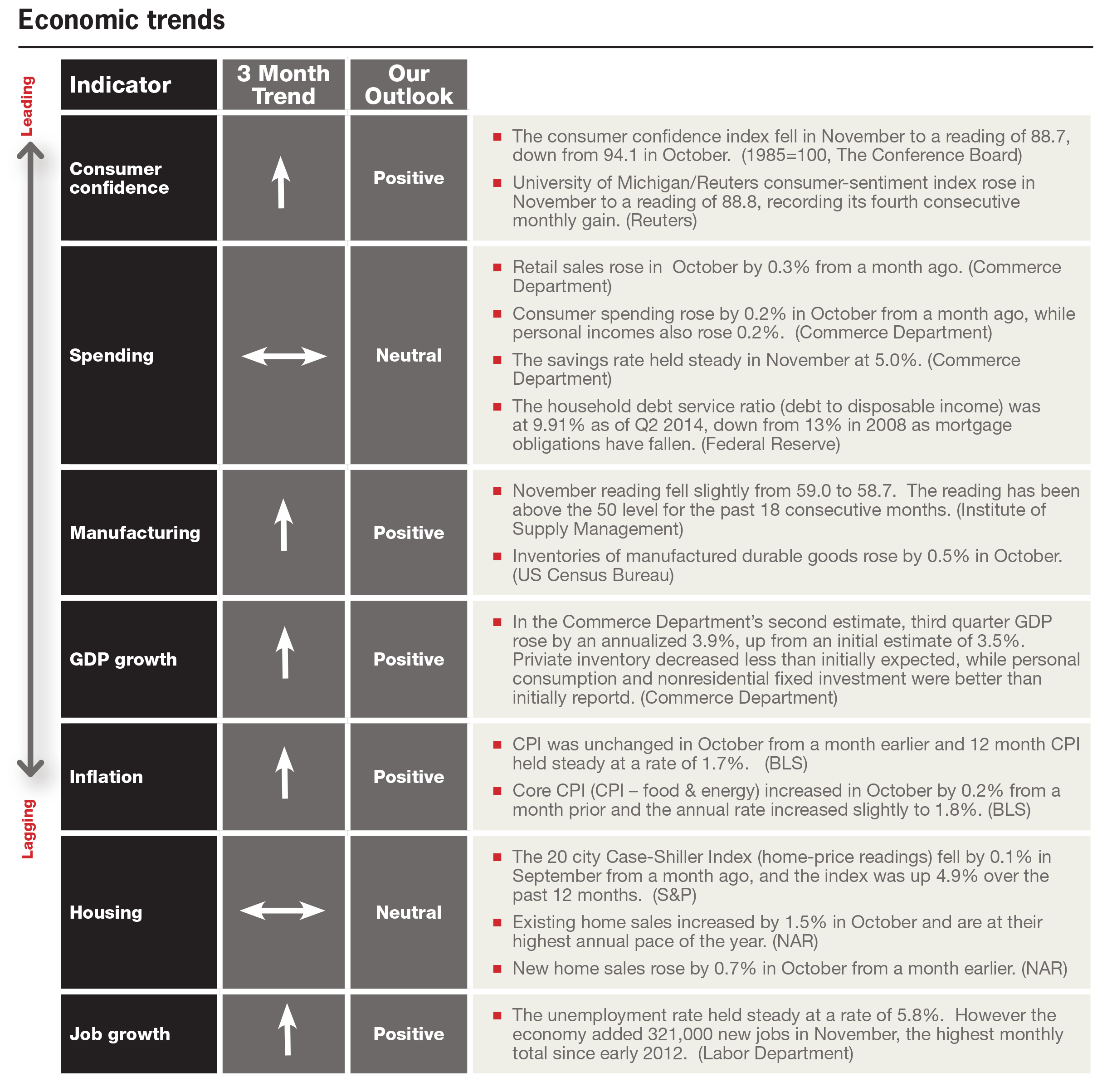

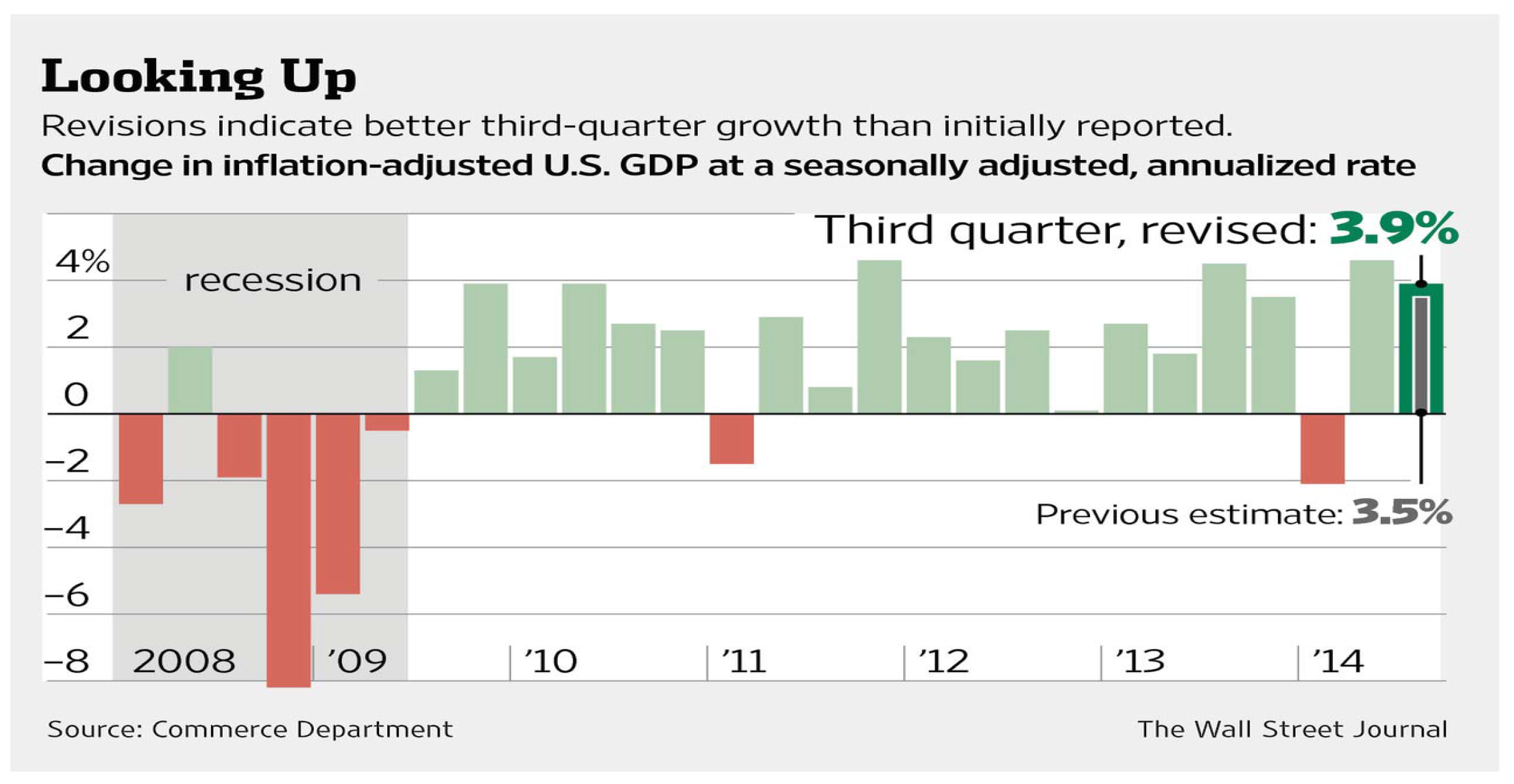

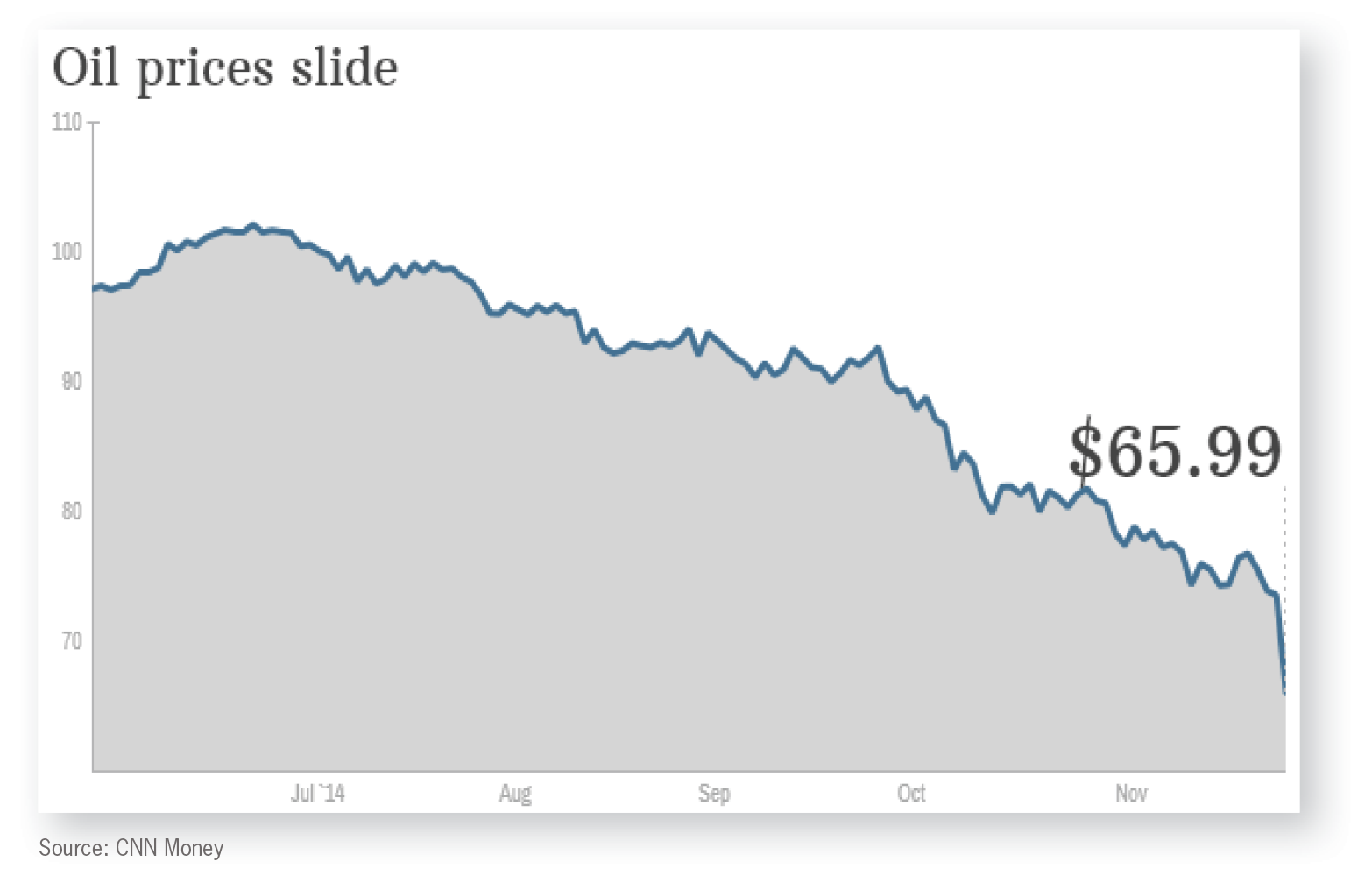

As we enter the holiday season and consumers look for a little extra cash to spend, they shouldn’t have to look too far. The price of oil has fallen nearly 40% since its annual peak in mid- June. This has helped drive down the national price of gasoline to an average of roughly $2.75 per gallon. The economic implications on a global scale are somewhat mixed, with major oil importers benefiting the most. The U.S. continues to consume more oil than it produces, but advances in technology and domestic production have been increasing at a rapid pace. Beyond energy, the backdrop for the U.S. economy continues to be strong, with a third quarter GDP estimate of 3.9% and a labor market that continues to plod along; although improvements are still needed. The strong close to 2014 is providing a robust tailwind for the domestic economy entering the New Year, whereas many countries overseas continue to cope with slower growth and potential deflation.

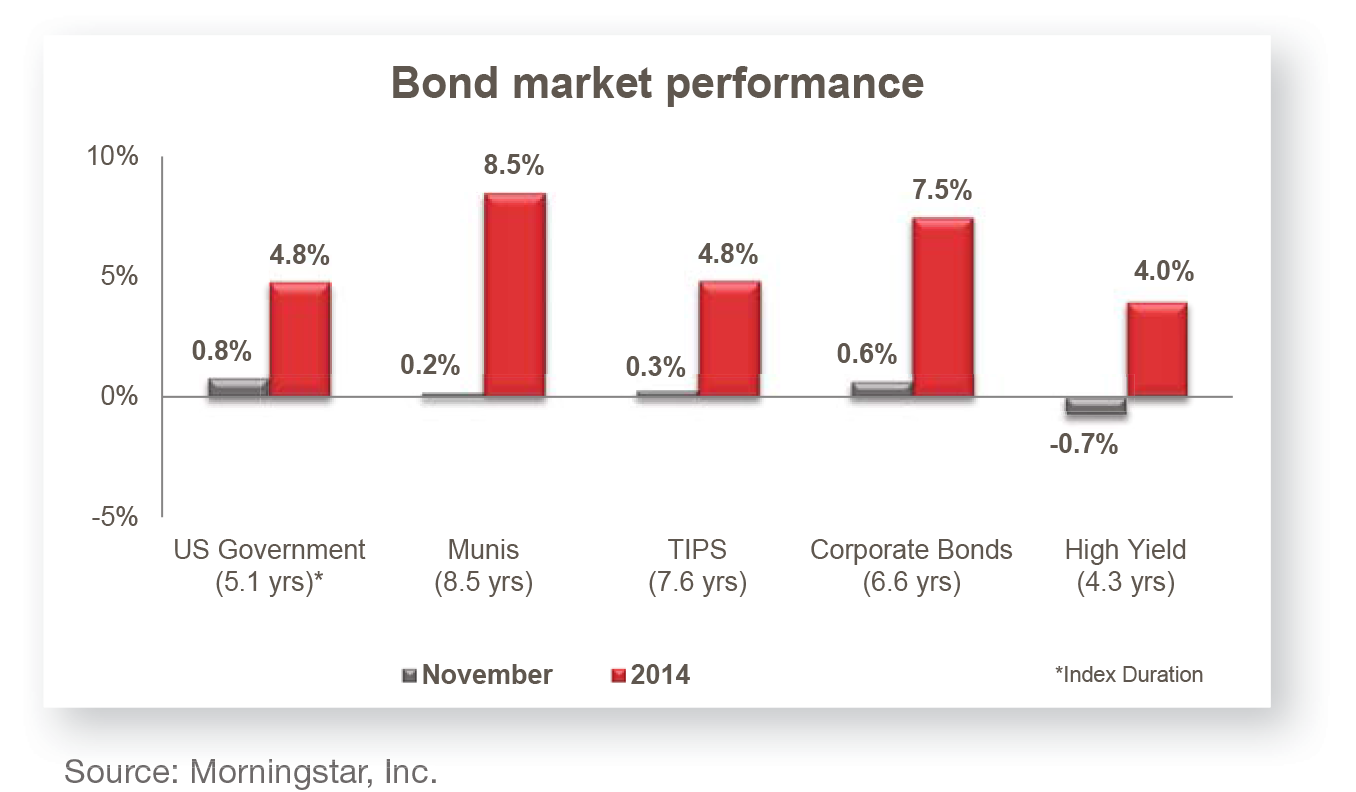

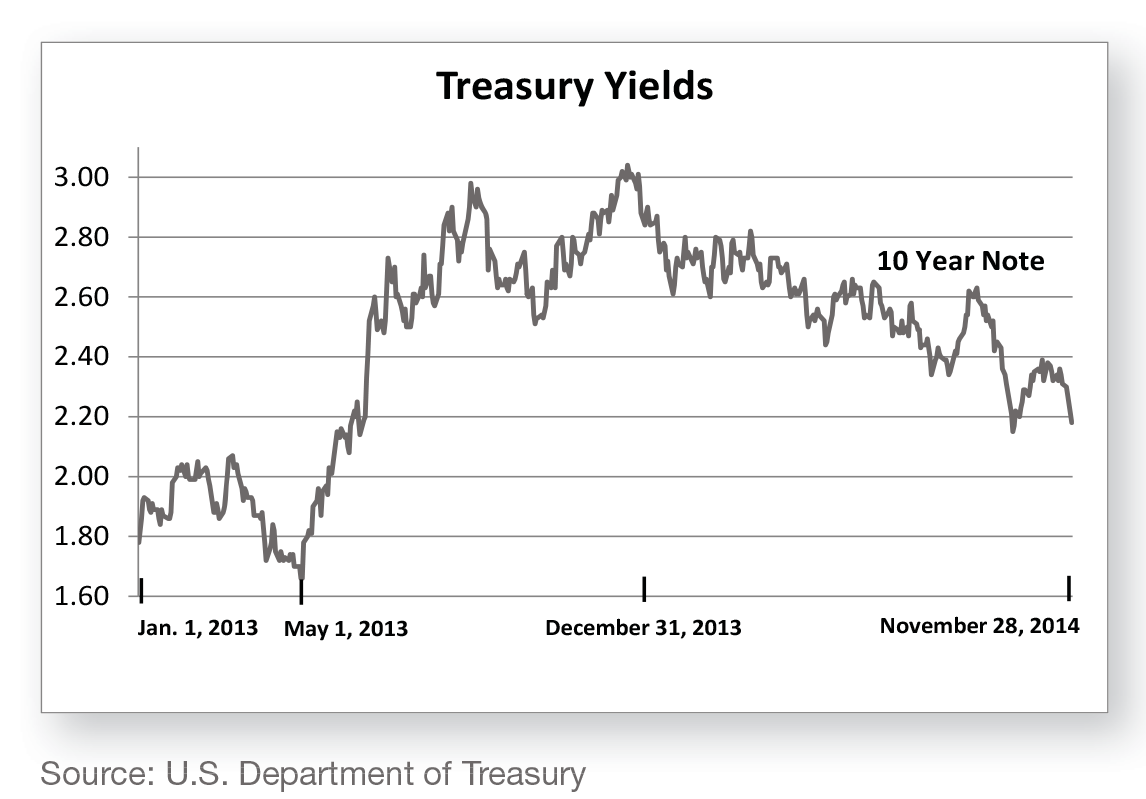

The bond market

Treasury rates drop across all maturities

Contrary to the trend for much of this year, interest rates dropped across the yield curve in November, providing a positive boost for bond prices. The flattening of the U.S. Treasury yield curve has been a point of interest in 2014, with rates on shorter-term bonds rising and longer-term bonds continuing to fall. A flattening and potentially inverted yield curve can be a signal of slow growth on the horizon. However, with the Federal Reserve manipulating rates to a greater extent than seen historically, this is not necessarily a foregone conclusion. Their bond purchase program, although now completed, has had the biggest impact on the long end of the curve, while the prospect of a higher federal funds rate in 2015 is placing upward pressure on short-term rates. With this scenario in play, it remains prudent to be well-diversified along the short and intermediate portion of the yield curve.

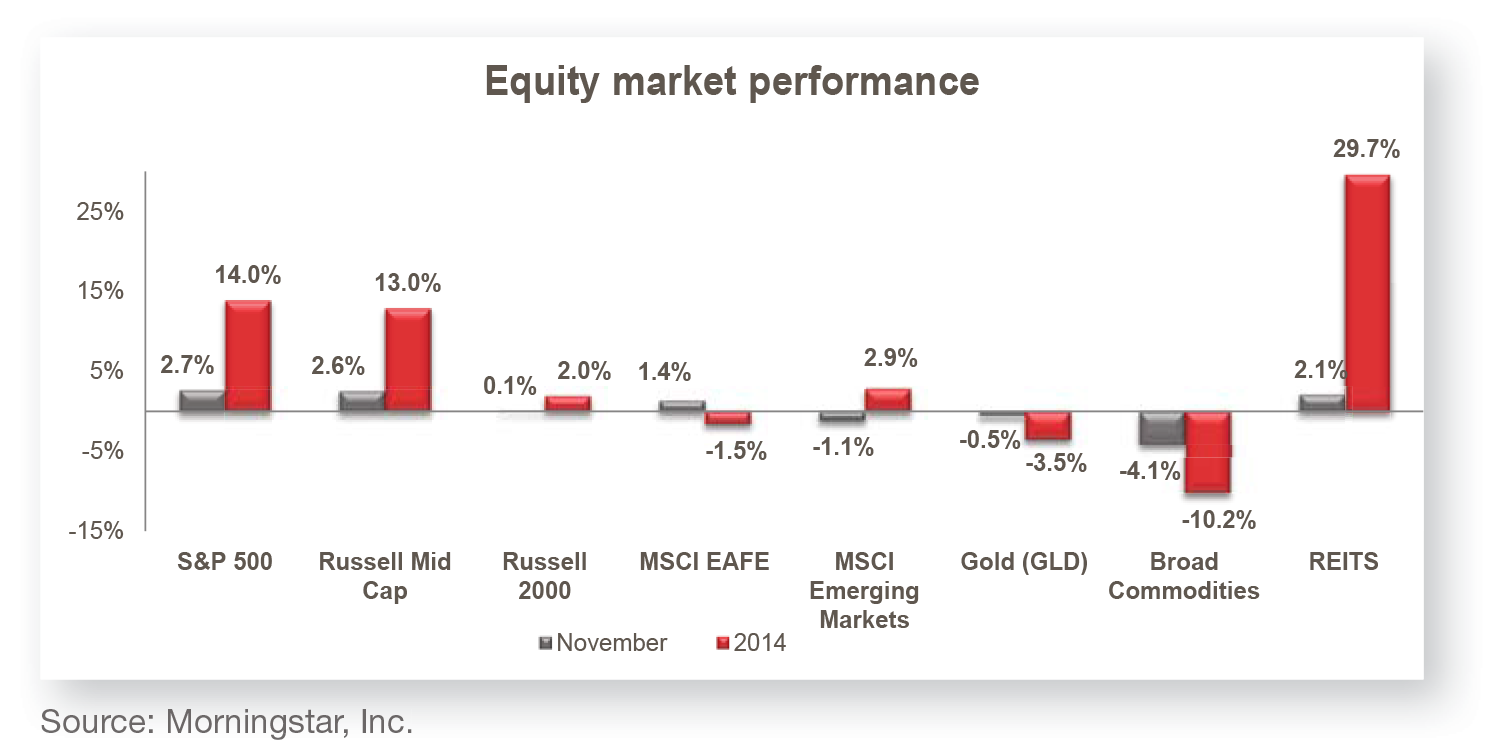

The stock market

Stocks push higher in November

The Dow Jones Industrial Average reached record highs yet again in November after fully working its way back from a sell-off in September / October. Large and mid-cap domestic stocks continue to lead the way, with small caps and foreign equities trailing well behind. Central banks around the world continue to look for new ways to stimulate economic growth, but these measures have not necessarily translated into strong stock returns. The European Central Bank is delaying until early 2015 for additional stimulus measures, causing markets in Germany and France to drop more than 5% year to date. On a positive note, a recent surprise interest rate cut in China did have a constructive impact on their stock returns, and U.S. markets are capitalizing on strong corporate earnings and a stable economy. While numerous record highs are a cause for worry amongst some investors, we still believe fundamentals justify the current trend.

Economic Trends

Headlines

U.S. grows continues to be strong, while energy market sells off.

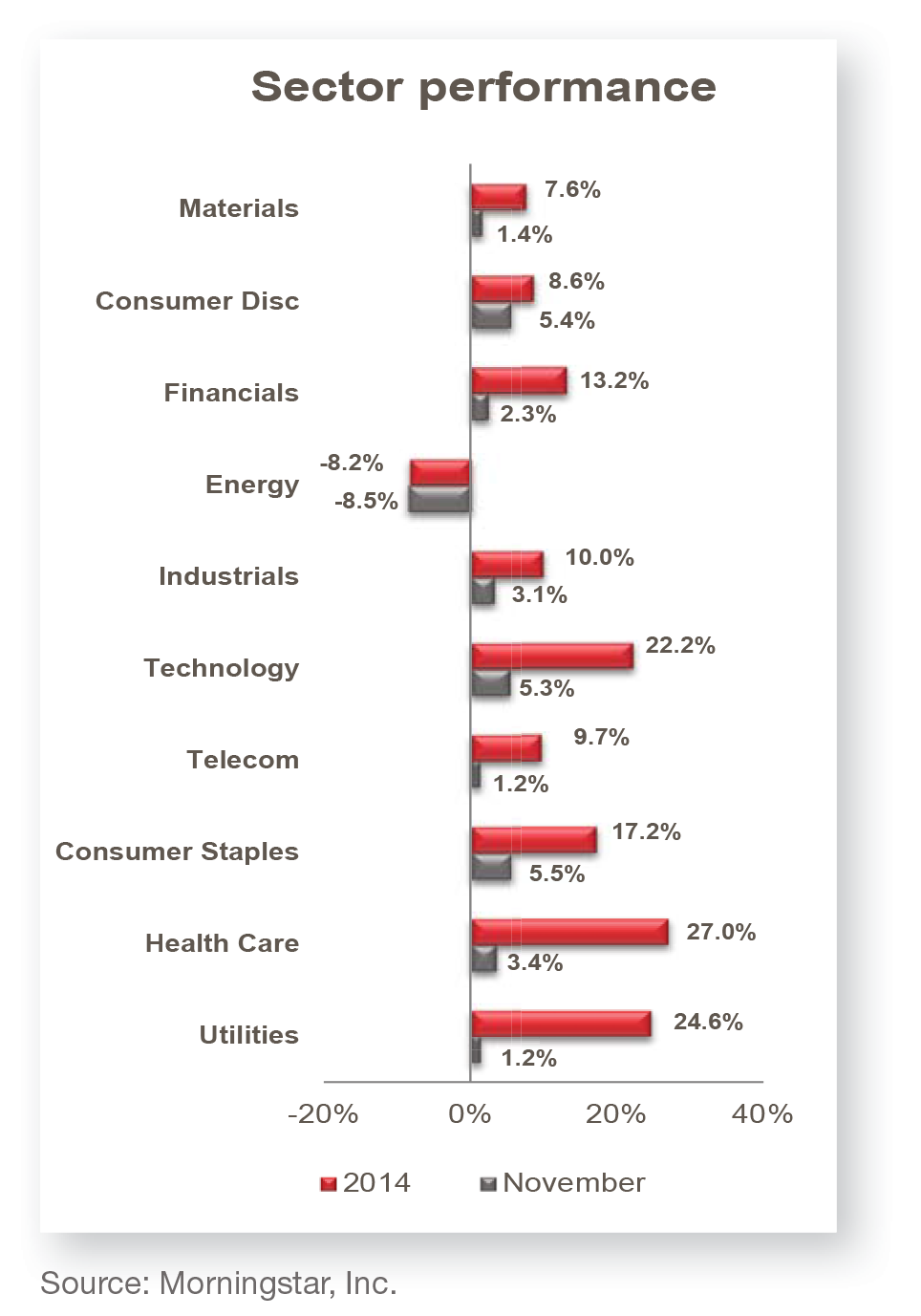

Large cap stocks once again lead markets higher in November.

Emerging markets lag, but see new measures put in place to help growth.

Energy stocks take major hit in November as oil prices approach the $60 / barrel level.

Fixed income markets

China steps into easing measures with a surprise rate cut.

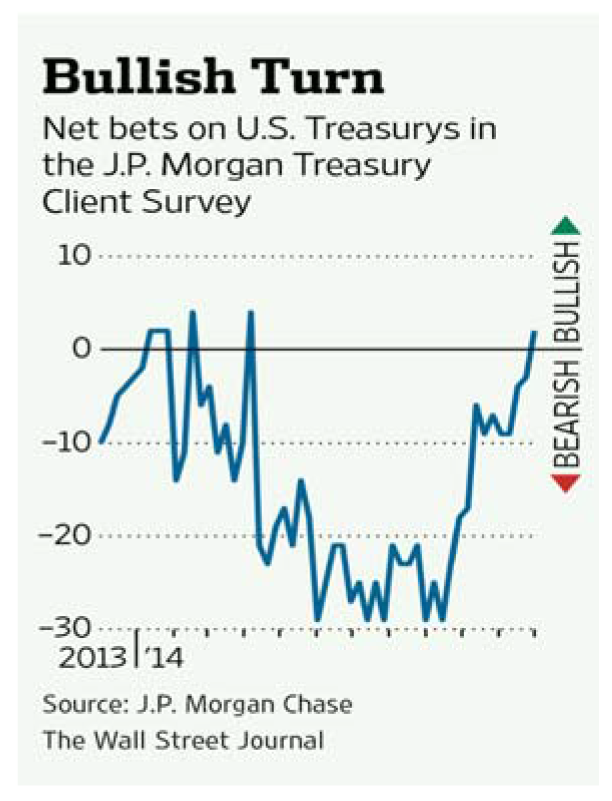

Survey shows investors now betting on run for Treasuries (meaning interest rates will fall).

Bronfman E.L. Rothschild, LP is a registered investment advisor. Securities, when offered, are offered through Baker Tilly Capital, LLC, member of FINRA and SIPC; Office of

Supervisory Jurisdiction located at 10 Terrace Court, Madison, WI 53718, phone 800.362.7301. Bronfman E.L. Rothschild, LP and Baker Tilly Capital, LLC are not affiliated.

This publication should not be viewed as a recommendation, an offer to sell, or a solicitation of an offer to buy a particular security or service. The commentary provided is for informational purposes only and should not be relied on for accounting, legal, tax, or investment advice. Financial information is from third-party sources. While such information is believed to be reliable, it is not verified or guaranteed. Performance of any indexes is provided for reference and competitive purposes only without factoring any fees, commissions, and other charges. Individual results achieved by investors will be different from those of the indexes. Indexes are unmanaged; one cannot invest directly into an index. The views and opinions expressed are those of Bronfman E.L. Rothschild, LP, and they are subject to change at any time. Past performance does not imply or guarantee future results. Investing in securities involves risks, including possible loss of principal. Diversification cannot assure a profit or guarantee against a loss. Investing involves other forms of risk that are not described here. For that reason, you should contact an investment professional before acting on any information in this publication.