Markets have begun 2015 on a volatile note, as plummeting commodity prices exacerbate fears of slowing global growth. We remain bullish on U.S. equities for 2015 and expect U.S. GDP growth of 2.5%–3.0%. Global GDP will likely be slower, expanding 2.0%–2.5% in 2015, reflecting euro zone weakness as well as more measured and bifurcated growth in the emerging markets.

Investors should be prepared for elevated volatility as markets work through the impact of slowing global growth and price declines in oil and other commodities. Political uncertainties will likely foment turmoil in the markets—including continued debate between the European Central Bank (ECB) and German finance ministers, renewed concerns about Greece, squabbles within OPEC, and economic deterioration in Russia. Given economic weakness outside the U.S., a strong dollar and weak oil prices, the Federal Reserve is likely to forestall interest rate increases until late in the year, which should keep the yield of the 10-year Treasury bond in the 1.50%–2.25% range for 2015.

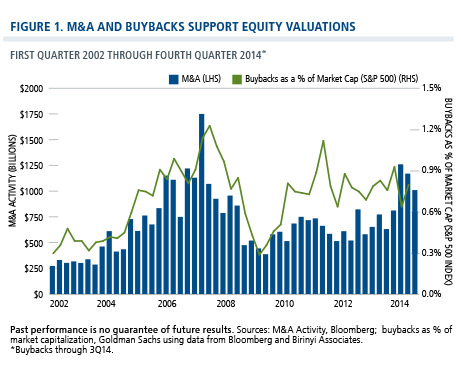

The good news? Deflationary pressures caused by plunging commodity prices will likely allow the Fed to “be patient” in pushing up short-term rates. This, combined with weak growth in Europe, has caused the 10-year Treasury to fall back below 2%, pushing spreads between equities and bonds close to historic high. As U.S. companies regain confidence that U.S. economic growth will strengthen, we believe M&A and share buyback activity will put a floor on valuations, allowing markets to move still higher (Figure 1). Our outlook is for the S&P 500 Index to hit 2,250 by year-end 2015, which would equate to a 14% return, including dividends.

Market Review

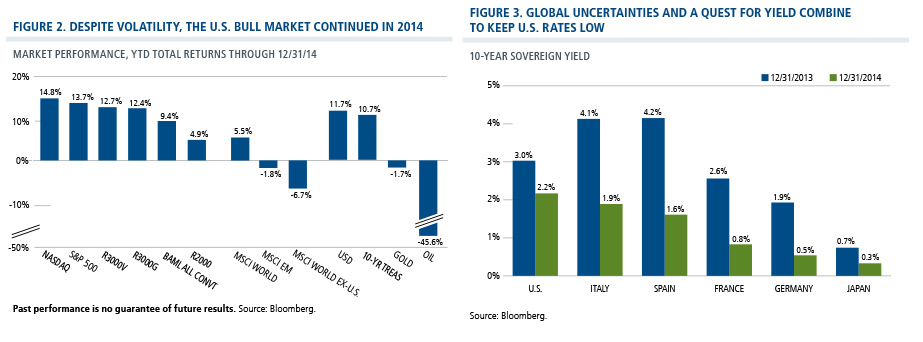

The U.S. markets led in 2014, with the S&P 500 Index returning 13.7% and the MSCI World ex-U.S. Index falling -6.7%. U.S. equities and convertibles benefited from still-accommodative policy and better economic fundamentals in the U.S., while a global quest for income and macro uncertainties supported the 10-year Treasury (Figures 2 and 3).

Still, the adage “every bull market climbs a wall of worry” certainly held true as U.S. stocks surmounted a range of concerns over the course of 2014, starting with Chair Yellen’s comments that interest rates might rise sooner than anticipated and fears that Europe would slip back into recession. As the year progressed, renewed concerns about the Fed’s timeline for raising rates created more headwinds, as did Russia’s bellicose stance toward Ukraine. The uncertainty around Russia and sanctions against the country took a particular toll on the euro zone as business and consumer confidence weakened. During the fourth quarter, markets were spooked by the potential for an Ebola pandemic and anxiety about declining oil prices as OPEC kept production high in the face of mounting global growth concerns.

Ultimately, optimism about global recovery, accommodative monetary policy—particularly in Europe—and solid corporate earnings growth won out in the U.S. market. Strong merger-and-acquisitions and buyback activity also provided key support to the market, as low corporate borrowing costs and high earnings yields made M&A and buybacks highly accretive to companies.

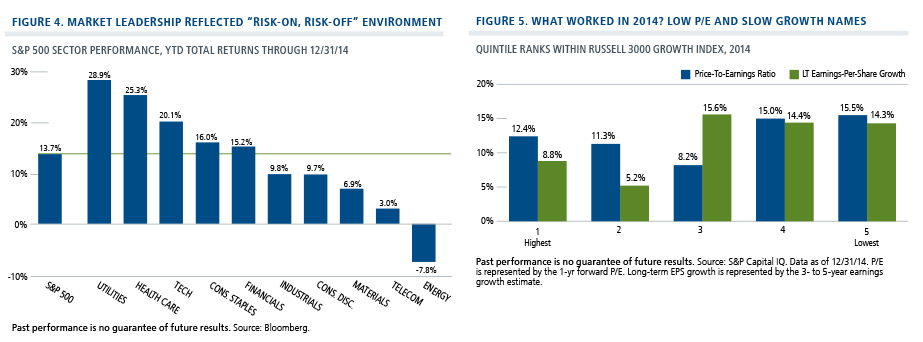

Against a backdrop of “risk-on, risk-off” vacillations, sector performance lacked a discernable pattern between traditional growth and defensive sectors. In a market with no clear direction, utilities led within the S&P 500 Index, followed by health care, technology and consumer staples (Figure 4). Within the growth stock universe, the markets rewarded names with low P/Es and the lowest expected earnings-per-share growth (Figure 5), as well as those with high dividend yields and large market caps.

Outlook

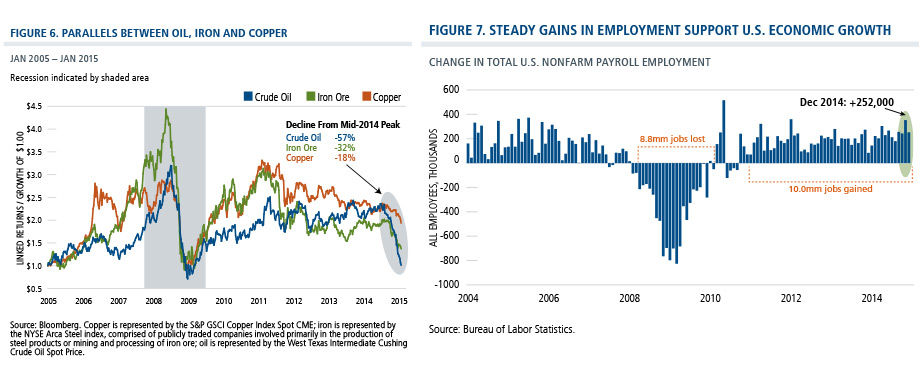

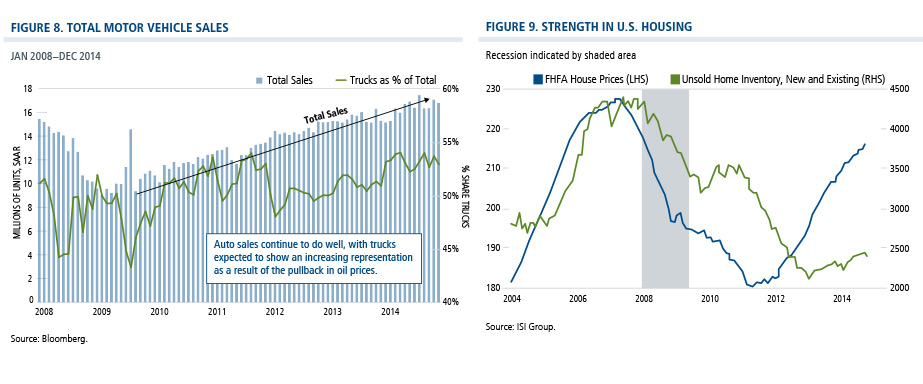

In addition to oil, other commodity prices have tumbled (Figure 6), suggesting that we’re seeing more than the impact of dissent within OPEC. Even so, we believe the global economy can continue to grow, albeit at a measured and uneven pace. Among major economies, conditions look healthiest in the United States. Plunging commodity prices may well be a harbinger of global economic weakness, but the recent strength in job growth, auto sales, and housing (Figures 7, 8 and 9) suggest that a U.S. recession is not imminent. Given the Fed’s willingness to take a “patient” approach in the face of falling energy prices and weakening global economic conditions, we expect continued accommodative monetary policy, with short-term interest rates staying put throughout most of 2015.

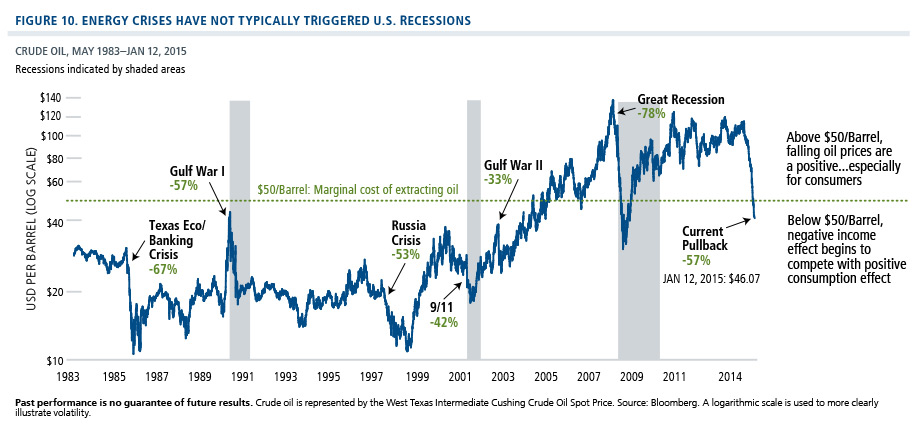

There has been much debate about the benefits and detriments of lower oil prices. During the holiday season, the “tax cut” of lower gas prices was heralded as a boon to consumers and retailers, although December retail sales were weak. However, with oil now below $50 a barrel (what many view as the marginal breakeven cost to extract oil), the consumption benefits of lower prices begin to be overshadowed by a deleterious income effect to businesses and industries with direct or indirect ties to the energy sector—hence the market’s recently amplified anxiety. Exploration-and-production (E&P) companies will have opportunities to reduce production over the next three to six months, the typical length of drilling leases. As current leases expire, E&P companies can moderate production to a less extreme supply-demand imbalance.

Based on past energy collapses, oil could fall another 10%–15% (to around $40 a barrel) before stabilization occurs, creating pockets of economic weakness in select industries and regions as well as spurring market volatility. However, we believe the negative economic impacts of plummeting oil prices can be contained, at least in the U.S. In the past, energy crises typically have not been catalysts for U.S. recessions. As Figure 10 shows, energy crises did not trigger broader economic collapses in 1984 and 1996, while the energy crisis of 2008-2009 was a byproduct of the housing market collapse. The diversification in the U.S. economy can provide a degree of resilience—notably, the energy sector represents less than 2% of GDP and energy companies represent 12% of earnings within the S&P 500. If the energy crisis were to infect other sectors of the economy, the Fed has considerable latitude to forestall rate increases, given the lack of inflationary pressures.

Moreover, we believe increased energy independence in the Americas should have a positive long-term economic impact for the U.S., due to reduced foreign policy spending, a benefit the markets do not appear to perceive—yet. There would also be benefits if Russia retreated from the provocative stance that characterized its foreign policy in 2014.

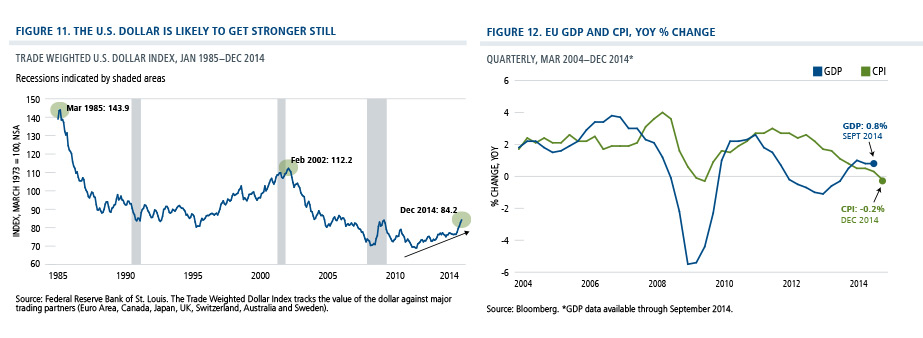

The dollar has staged a brisk rally as global growth concerns have grown (Figure 11). We expect the dollar to remain strong through 2015, reflecting the better economic fundamentals in the U.S. versus many other economies. At this point, we don’t view the strong dollar as a hurdle to U.S. economic growth, again due to the more balanced nature of the economy. That said, many companies have already guided lower for 2015 due to the strong dollar’s impact on their overall earnings and we need to be vigilant in our research about this impact going forward.

Europe is more of a wild card. When we view Europe relative to the other regions of the global economy, we see weaker growth fundamentals, as well as monetary accommodation and liquidity that has been inadequate but appears poised to loosen. While momentum has been weak, we expect it to stabilize and improve, and valuations are cheaper. The euro zone has officially crossed through the deflationary threshold (Figure 12), providing increased incentive for the ECB and German finance ministers to break through their stalemate. We believe the ECB will take more dramatic steps during the first quarter to increase the size of its balance sheet (i.e., quantitative easing) toward 2012 levels, although it is too soon to tell over what time period QE will take place.

Meanwhile, in Japan, domestic economic fundamentals remain weak, but corporate fundamentals are improving and the sales tax increase appears to have been put off. Monetary policy remains highly accommodative, and we’re encouraged by the recent uptick in corporate stock buybacks.

In the emerging markets, we expect continued divergence in economic fortunes as commodity prices fall and we enter the third year of what will likely be a multi-year cyclical strong-dollar environment. Against the backdrop of weak commodity prices, countries such as Russia, Brazil and Malaysia will likely face stiffer headwinds, versus India and China. We continue to view China’s recent stimulus efforts as being in-line with its longer-term strategy to move demand to the private sector with a focus on services and consumption. Although we have some shorter-term concerns about valuations and currency risk, we also believe the case for India is compelling over the medium- to longterm, supported by new leadership, reforms, infrastructure spending and better controlled inflationary pressures.

Positioning

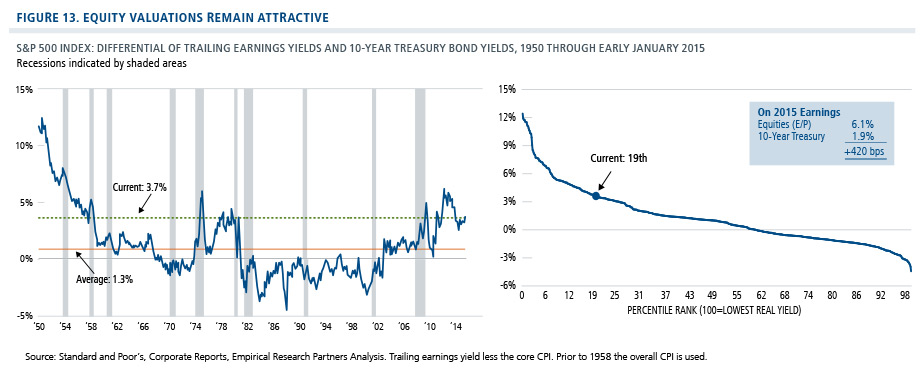

While these next months may not be comfortable for investors, we do see many opportunities. With oil prices likely to stabilize over the next several months and the ECB and Germany reaching a consensus on stimulus and structural reforms, we believe equity markets can resume their upward climb for 2015. In our view, steady U.S. GDP growth, quantitative easing in Europe, nearly non-existent inflationary pressures, and the widening spread between equity yields and 10-year Treasury yields (Figure 13) will stimulate renewed merger-and-acquisition and buyback activity, providing support to the equity market, as in 2014.

Although valuations in some sectors of the equity market may be stretched, valuations and fundamentals are attractive overall. The earnings yields of stocks remain extremely compelling relative to inflation, as well as Treasury yields. We continue to expect a longer-thantypical recovery cycle given the depth of the Great Recession, and believe the collapse in energy prices may elongate the recovery further as the Fed follows its patient approach. In our view, we are still in the middle innings of recovery, which supports the case for growth stocks. At 1.2x, the premium for U.S. large-cap growth over large-cap value is well below the 3.0x multiple of the technology bubble peak and less than the 1.4x average since 1990.

We remain overweight secular and cyclical growth opportunities in areas such as technology, health care, consumer discretionary and financials. We are underweight defensive names and also believe it is too soon to emphasize late-cycle industrials, materials, energy and other commodities. We are highly cautious regarding names with extreme multiples relative to underlying growth rates, given our expectation for near-term volatility and our anticipation of rising rates by late 2015.

Similarly, in non-U.S. markets, we continue to favor technology and consumer companies, viewing these areas as better positioned to navigate the crosscurrents coming from a strong dollar, weak commodity prices and slowing global growth. We continue to seek out opportunities tied to the consumer, as weaker commodity prices may provide the euro zone and countries such as China, India, Indonesia, and Japan with additional flexibility to pursue more accommodative monetary policies; these in turn could serve as a tailwind to consumption. We remain underweight the commodity complex as well as materials, although there may be opportunities to increase commodity exposure this year, as valuations and fundamentals warrant. We believe our focus on strong balance sheets, sustainable growth, valuations and comprehensive credit analysis will remain paramount, as we expect a few credit surprises to shake the markets.

In regard to regional positioning, we were generally underweight Europe for most of 2014 but believe opportunities will likely increase as 2015 progresses. While Mario Draghi hasn’t shown the ability to inspire shock-and-awe as Prime Minister Abe has in Japan, we believe additional quantitative easing from the ECB can provide a catalyst to improve economic fundamentals as well as a tailwind to the equity markets. In this environment, we are focusing on export-oriented companies benefiting from the weaker euro and asset reflation plays.

We began ramping up Japan exposure during the second half of 2014, and are currently equal-to-slightly overweight across most of our global and non-U.S. strategies. This upcoming earnings season may well provide opportunities to tilt further to Japanese equities. Despite the advance in the equity markets during the fourth quarter of 2014, valuations remain attractive—particularly versus the U.S. market—while many companies have improved capital and operating efficiencies that could translate into improved earnings.

In the emerging markets, we expect the bifurcation of returns we saw in 2014 to continue in 2015. Within our top-down framework, we favor countries positioned to benefit from secular tailwinds, such as China, Mexico, Indonesia, India and the Philippines. In regard to China, we continue to seek ways to capitalize on the country’s shift toward a greater emphasis on consumption and services. Reflecting a more cautious stance toward countries where economic reforms have less momentum, we expect to remain underweight Russia, Brazil, and Malaysia.

Convertibles

Because they have hybrid characteristics, convertibles can provide equity upside participation with potentially reduced volatility when stock markets decline. Historically, convertibles have performed well during volatile but generally upwardly moving equity markets—the environment we believe we will see in 2015—because convertibles benefit from their sensitivity to rising equities while the embedded option to convert into common stock becomes more valuable with the rise in volatility. Convertible issuers also tend to be more growth oriented, and therefore may be better positioned for the environment that we believe we are in.

However, we do not believe that all convertibles are equally well suited to this environment. During 2013 and the early portion of 2014, the market generally favored convertibles with high equity sensitivity, but since mid-2014, we’ve seen a more pronounced preference for convertibles that offer more balanced risk and reward attributes. We expect issuance for 2015 to stay in line with that of the past two years ($89 billion in 2014 and $93 billion in 2013), supported by economic expansion in the U.S., rising equity markets, and volatility (which can increase investor demand for the asset class).

Conclusion

While we expect near-term volatility associated with falling oil prices and weak economic growth in Europe to continue over the next few months, we remain bullish about the global economy and equity markets overall. Despite the impact of reduced capital spending on oil and oil-related sectors, we see U.S. GDP growth of 2.5%–3.0% in 2015 and corporate earnings growth in the 6%–7% range. We believe the start of QE in Europe will ease concerns about global growth. With share buybacks and M&A activity helping provide a floor, inexpensive valuations and an improving economy should allow the U.S. market to move 12% higher by year end, providing an equity return of around 14%.

The S&P 500 Index is considered generally representative of the U.S. equity market. The MSCI World Index is considered generally representative of the market for developed market equities. The MSCI World ex-U.S. Index is a market capitalization weighted index composed of companies representative of the market structure of developed market countries in North America (excluding the U.S.), Europe and Asia Pacific regions. The MSCI Emerging Markets Index is a free float adjusted market capitalization index cited as a measure of the performance of emerging market equities. The Nasdaq Index is an index composed of stocks that are listed on the Nasdaq stock exchange. The Russell 3000 Growth Index is considered generally representative of the U.S. growth stock market. The Russell 3000 Value Index is considered generally representative of the U.S. value stock market. The Russell 2000 Index is considered generally representative of the U.S. small-cap stock market. The BofA Merrill Lynch VXA0 Index is considered generally representative of the U.S. convertible market. The Consumer Price Index (CPI) measures the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care.

Price-to-earnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings.

Earnings-per-share (EPS) is the portion of a company’s profit allocated to each share of common stock.

Earnings yield is earnings divided by stock price. Quantitative easing refers to central bank bond buying activities.

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Outside the U.S., this presentation is directed only at professional/sophisticated investors and it is for their exclusive use and information. This document should not be shown to or given to retail investors.

Investments in overseas markets pose special risks, including currency fluctuation and political risks, and greater volatility than typically associated with U.S. investments. These risks are generally intensified for investments in emerging markets.

The price of equity securities may rise or fall because of changes in the broad market or changes in a company’s financial condition, sometimes rapidly or unpredictably. These price movements may result from factors affecting individual companies, sectors or industries.

Fixed-income securities are subject to interest rate risk. If rates increase, the value of fixed-income investments generally declines.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. Investors may not make direct investments into any index.Calamos Investments LLC

2020 Calamos Court | Naperville, IL 60563-2787

800.582.6959 | www.calamos.com | [email protected]

Calamos Investments LLP

No. 1 Cornhill | London, EC3V 3ND, UK

Tel: +44 (0) 20 3178 8838 | www.calamos.com/global

© 2014 Calamos Investments LLC. All Rights Reserved.

Calamos® and Calamos Investments® are registered trademarks of Calamos Investments LLC.

OUTLKCOM 18055 0115Q O C